A study by the Reserve Bank of New Zealand (RBNZ) claims that people taking out mortgages to buy a home have become less vulnerable to the effects of a housing market downturn, higher interest rates and/or a loss of income since the introduction of Loan to Valuation Ratio (LVR) lending restrictions were introduced in October 2013. From Interest.co.nz:

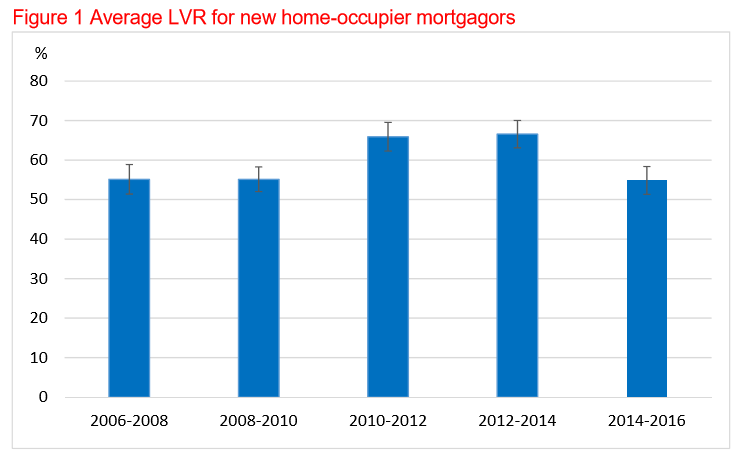

The report found that prior to the introduction of LVRs in October 2013, the average new mortgage was for 67% of a property’s value.

But by mid-2016 the average LVR had fallen to 55%.

That excludes lending to investors but includes lending to first home buyers and those moving up the property ladder.

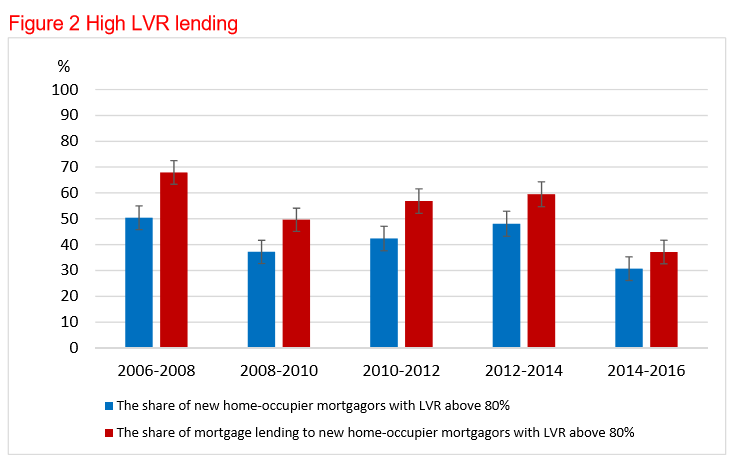

Over the same period, the amount of money provided to home buyers where the amount borrowed was above 80% of a property’s s value declined from more than 80% of new mortgage lending to 35%.

“This suggests a substantial increase in average equity buffers, driven by a widening gap between median mortgage debt and median house prices,” the report said.

This had benefits for both borrowers and the banks that were lending them the money, it said…

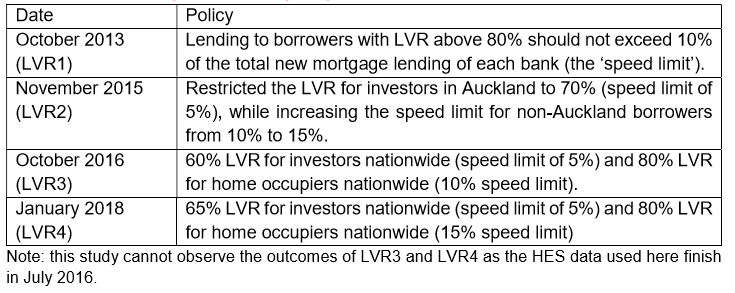

The actual report includes the below table listing the LVR changes by implementation date:

The decline in average LVR is shown below:

And here’s the decline in high LVR lending:

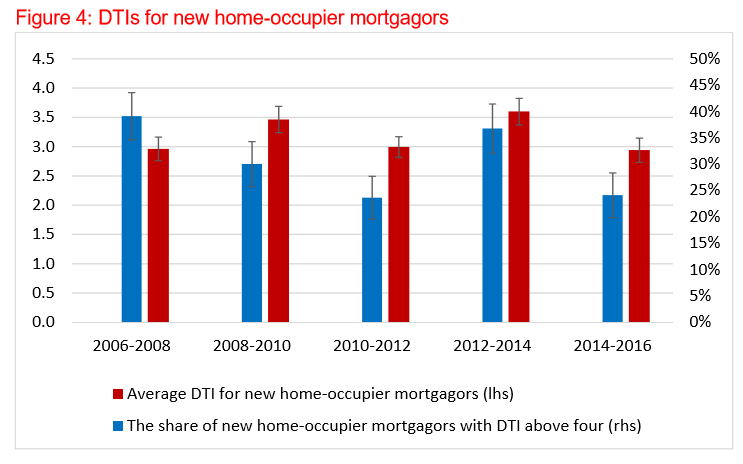

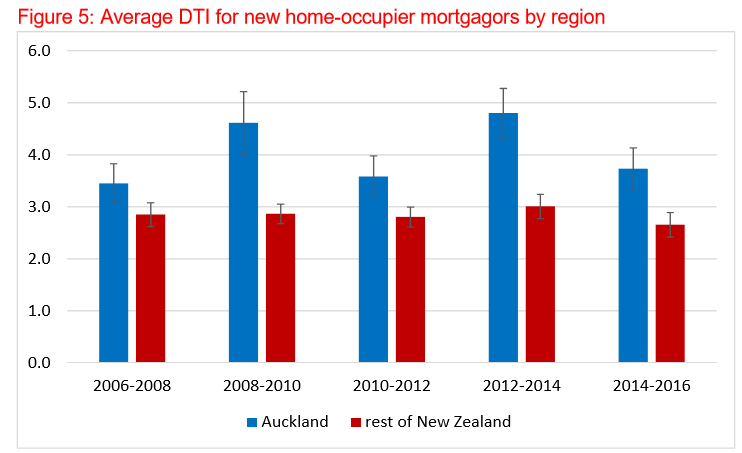

The average debt-to-income (DTI) for new borrowers also declined from 3.6 to 2.9 in the last time cohort and the share of borrowers with a DTI above four declining from 37% to 24%:

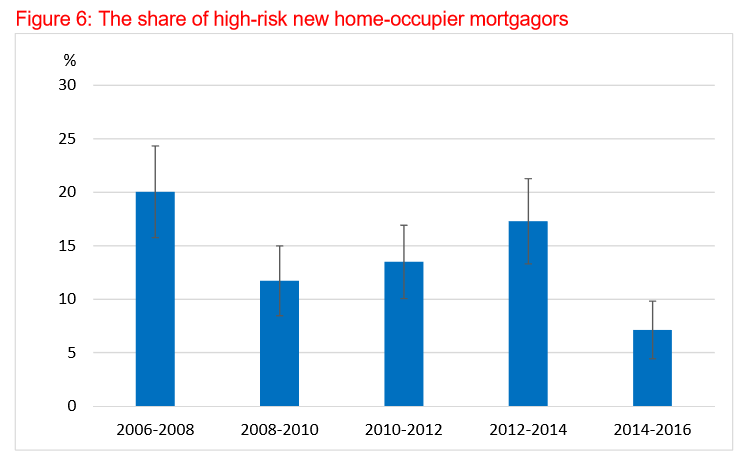

The share of high-risk borrowers who have a DTI above four and an LVR above 80% declined significantly after the policy, from 17% to 7%:

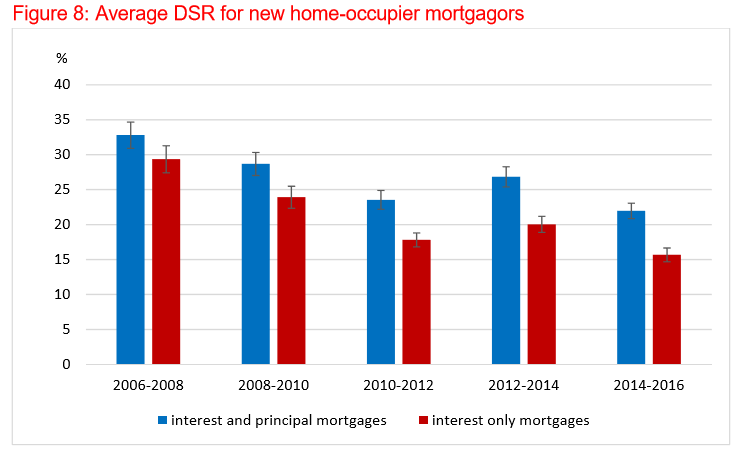

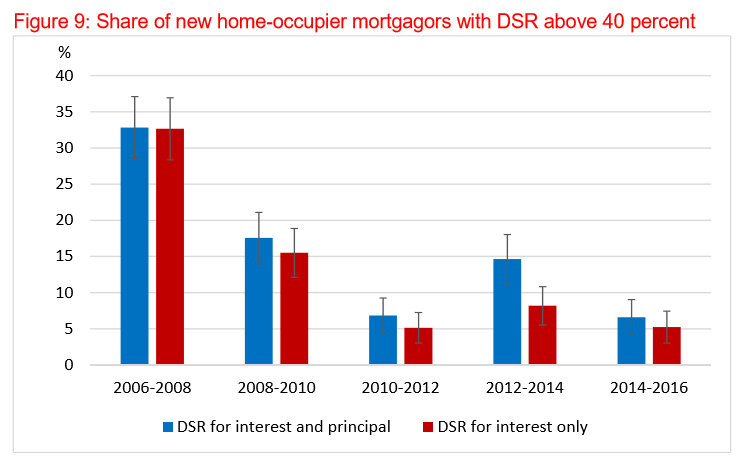

Whereas the average debt-servicing ratio (DSR) has also declined since mid-2014 (figure 8) for both owner-occupiers and investors:

In light of the above, it’s hard to believe the RBA opposed macroprudential measures for so long.

Good job RBNZ.