Citigroup forecasts that the rising cost of funding will prompt Australia’s four major banks to increase their mortgage interest rates independently of the Reserve Bank of Australia (RBA), with the banks tipped to begin lifting their mortgage rates by an average of eight basis points by September. Citigroup adds that the rise in banks’ short-term funding costs since early 2018 is likely to be sustained. From The AFR

The big four are expected to start raising rates before the end of their financial years at the beginning of September.

For a $1 million borrower on a 30-year term with a 20 per cent deposit, an 8 basis point rise will mean an extra $45 a month for a principal and interest loan, says Canstar. That rises to $67 for an interest-only investor.

This will increase financial stress on many household budgets already struggling with record levels of debt as the average debt-to-income ratio tops 200 per cent.

For example, four in 10 loan applicants – including borrowers attempting to refinance existing property loans – are being rejected because lenders are toughening scrutiny of their capacity to service a loan for the full term, according to analysis by Digital Finance Analytics.

…the “unusual and sustained” spike is “seemingly here to stay”, having remained elevated since February with few signs of reversing, according to Citi analysis.

There are strong reasons to believe that this housing correction could end up being a doozy.

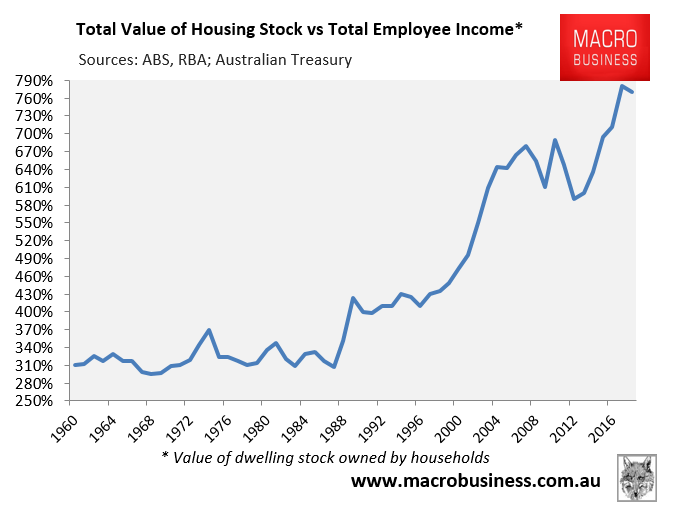

First, dwelling values are more expensive than ever when compared against incomes:

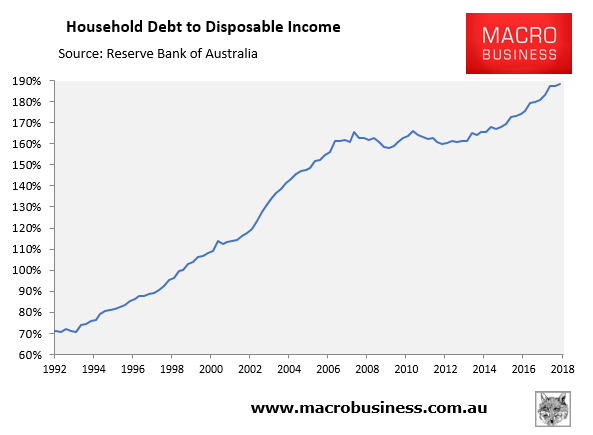

As are households’ debt-loads:

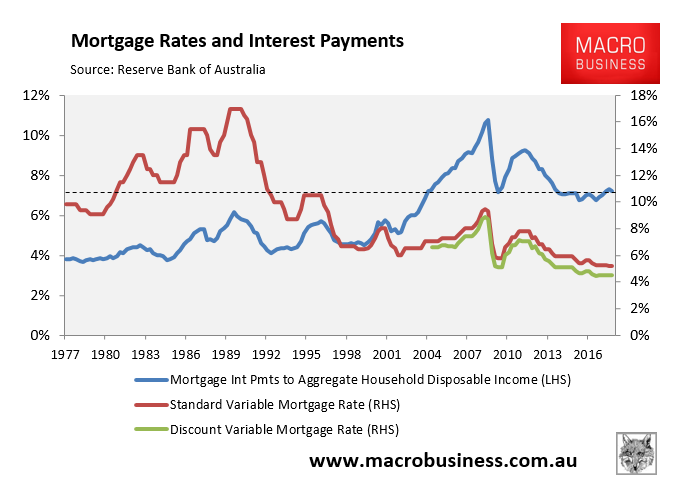

Second, past housing corrections were arrested by big reductions in mortgage rates and, in the case of the 2008 correction, huge fiscal stimulus as well:

However, with the cash rate already at just 1.5%, there is limited scope to cut mortgage rates further. Moreover, as noted by Citi, Australia’s banks are likely to raise mortgage rates out-of-cycle to the RBA due to higher wholesale funding costs, not to mention regulatory pressures arising from the banking Royal Commission.

The fiscal pressures facing the federal budget also limits the government’s ability to undertake fiscal stimulus to support households and the housing market.

And then there’s Labor’s negative gearing and capital gains tax reforms in the event that it wins the next election.

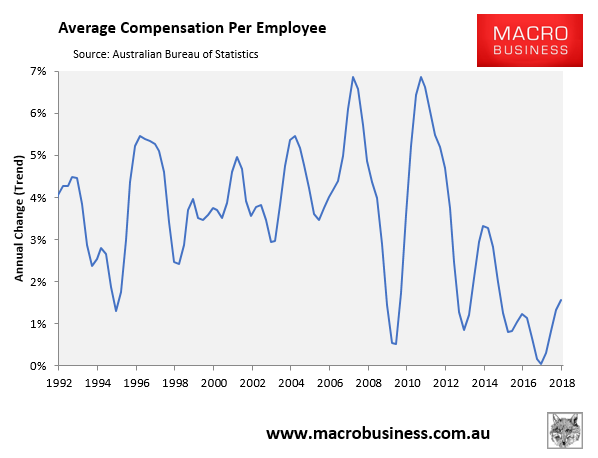

Finally, with both inflation and wages growth running at such low levels (see next chart), any correction in house prices is likely to occur nominally through price falls, rather than in real terms via inflation.

These factors alone mean this housing correction is likely to be deeper and more protracted than prior episodes.

unconventionaleconomist@hotmail.com