A very mixed session here in Asia as stock markets put in scratch sessions and mild losses in reaction to the BOJ monetary policy and Chinese PMI prints. Bonds gained while the USD pushed higher against Yen but lost ground against the Australian dollar.

The Shanghai Composite finished exactly 1 point down to 2860 after a listless session, remaining below recent resistance at 2900 points, unable to gain traction. The Hang Seng Index was more definitive, losing another 0.5% to finish at 28593, now having pulled back last week’s swing play move as it looks set to return to support at 28000 points proper:

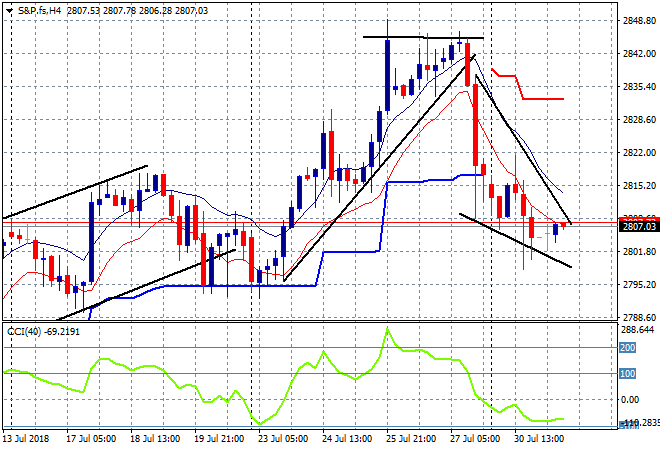

S&P futures are up slightly as we go into the European open, where it could well be a volatile session given the crowded economic calendar. The four hourly chart is kind of making an attempt at a bullish falling wedge pattern here as price gravitates around 2800 points, where support must hold going into the latter half of this week:

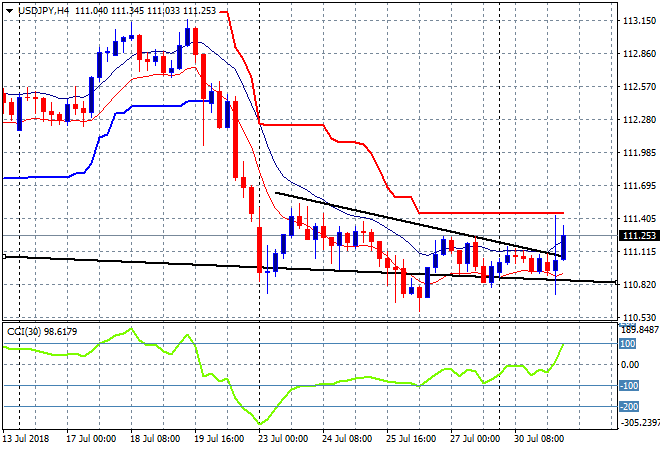

Japanese stocks were all over the place with the broader TOPIX falling while the Nikkei 225 put in a scratch session in response to the (late) BOJ policy shift. The latter finished at 22543 points, remaining stuck between the low and high moving average band on the daily chart. The USDJPY pair however shot above the 111 handle and the series of lower highs on the four hourly chart after some intrasession volatility. It remains to be seen if this is a true breakout yet as considerable resistance overhead at 111.40 must be cleared:

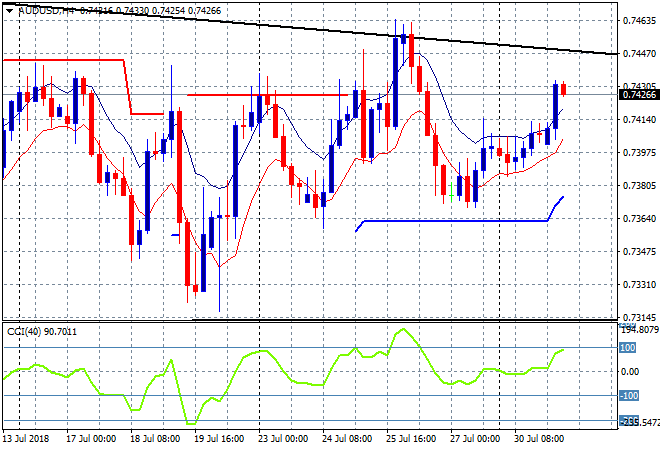

The ASX200 also put in a scratch session, unable to make any gains as the Aussie dollar climbed, finishing at 6280 points. The Aussie dollar finally moved, this time higher on the back of the BOJ move as it absorbed the Chinese PMI prints with aplomb. This breakout will likely have legs up to the high 74s at last week’s high before likely reverting back to the mean:

The data calendar is crowded tonight with a trifecta of extermeley sensitive European releases, namely German unemployment, EZ wide CPI and 2Q GDP estimates. In the US it’s May house prices and consumer confidence figures for July.