As Trump trounces Europe and supports Russian hegemony, markets continue to run the concern thread over trade tensions, while pushing the hope barrow on stellar US corporate earnings to keep the whole risk edifice afloat. The Aussie and Kiwi dollar advanced against the USD on RBA optimism and higher inflation levels in New Zealand.

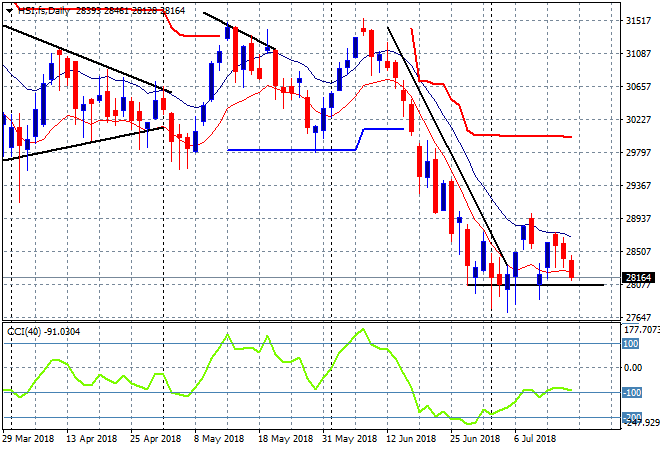

The Shanghai Composite has fallen back below the previous level of support at 2800, down 0.7% to 2793 points as it flounders about. The Hang Seng Index was worse off, down 1.2% to close at 28196 points, returning to the bottom here on the daily chart at 28000 after the false breakout above 28900 previously:

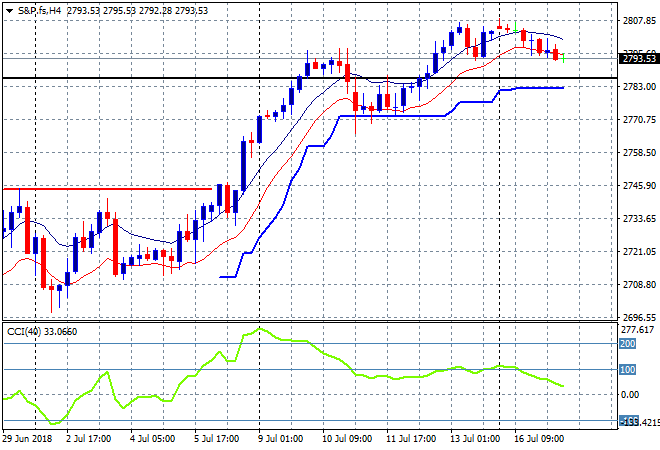

S&P futures have pulled back alongside Eurostoxx, with the latter indicating a slip of 0.1% or so on the open. The S&P500 four hourly chart suggests a retracement back to trailing ATR support before another attempt at the 2800 level:

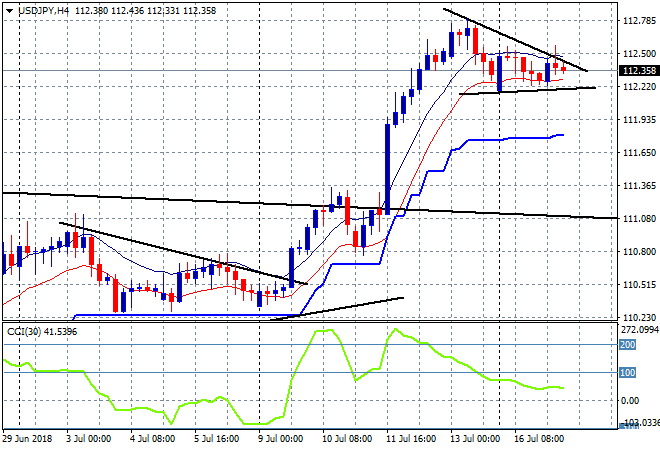

Japanese stocks were the best performers in the region, even as Yen moderated against USD, with the Nikkei 225 up 0.4%, closing at 22697 points, looking quite firm on the daily chart. The USDJPY pair has remained above the 112 handle, with a pennant pattern forming here on the four hourly chart as it unwinds last weeks extremely overdone momentum:

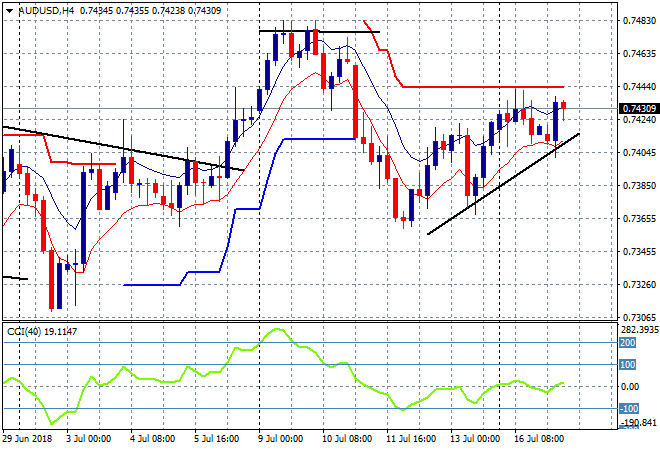

The ASX200 has pulled back to psychological support at the 6200 level, closing 0.6% lower at 6203 . The Aussie dollar has pushed through the 74 handle matching yesterdays highs with the tentative uptrend still intact, but overhead resistance at 74.40 still weighing:

The data calendar only has a few central bank speeches to keep an eye on overnight, plus US industrial production for June.