Via HSBC:

- USD rally to continue as the Fed tightens;

- Other central banks have delayed hiking creating asymmetric risk for the USD;

- Tumbling emerging markets are adding more upwards pressure the USD, and

- Neither USD valuations nor positioning is yet stretched.

I would add a slowing China, falling commodity prices (especially bulks which are weakest in the August-November period) and the trade war.

HSBC cut its Australian dollar forecast to 70 cents by year end from a previous 72 cents. It’s now matched the MB outlook.

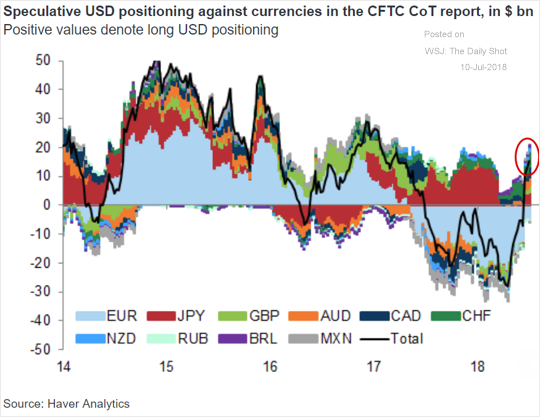

A chart from Goldman makes the point that the USD rally has plenty of room yet to run:

We’ll need to see at least one of four things before the AUD bottoms:

- European growth must accelerate and the ECB tighten faster, dropping the USD;

- US growth will need to fail such that the Fed stops tightening, dropping the USD;

- China will need to stimulate enough to turn its incipient slowdown, boosting Australian prospects;

- Australian domestic demand will need to accelerate enough to trigger RBA tightening.

Not one of those preconditions has yet been met, let alone plural. HSBC is right.

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar. Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.