China has released its June QTR national accounts and it’s some whack numbers. Growth is steady at 6.7%:

But the monthly numbers for June is where the action is as internals keep slowing with industrial production at 6%, fixed asset investment at 6% and retail sales at 9%:

Advertisement

Infrastructure investment is slowing fast with some offset in private sectors:

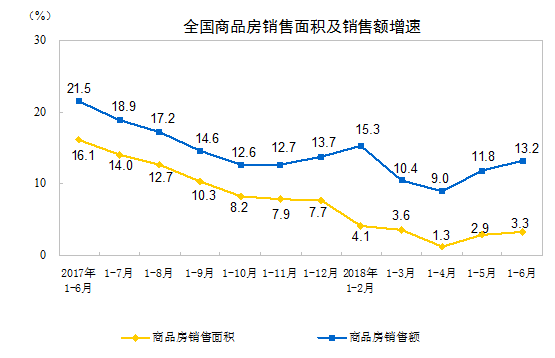

But the big support to growth is real estate which remains in an outright boom, contrary to any hopes of “rebalancing”. Sales are accelerating year to date though less so year on year:

Advertisement

1-6 months, real estate sales area of 77143 square meters, an increase of 3.3% , higher than the 1-5 increase in March 0.4 percentage points. Among them, the sales area of residential buildings increased by 3.2% , the sales area of office buildings decreased by 6.1% , and the sales area of commercial business buildings increased by 2.4% . Commercial housing sales were 669.45 billion yuan, an increase of 13.2% , and the growth rate was increased by 1.4 percentage points. Among them, residential sales increased by 14.8% , office sales decreased by 3.2% , and commercial business sales increased by 5.7% .

And construction starts are bonkers with a second month in a row posting all time highs for floor area commenced:

Advertisement

Year to date floor area starts are now up 11.8%:

That has been enough to re-accelerate total floor pace under construction to year to date growth of 2.5%:

Advertisement

That’s the major driver behind still insane steel output which fell back 80.2mt:

Advertisement

Though cement production fell hard as infrastructure comes off, nor can it be exported like steel so it has no OBOR uplift:

Crazy numbers. Some stimulus components are cooling fast but others are heating up even more.

Advertisement

I find it hard to believe that this level is real estate investment is sustainable for any period of time. China has been tightening not loosening around it. And the yuan outflows also hit realty especially hard. That said, property prices have been rising again in sub-tier one cities and response in supply has been immediate. So unless we see those prices cool we may see yet more empty apartments built into the heavens.

The base case remains growth slowing as mortgage credit saps both prices and starts:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.