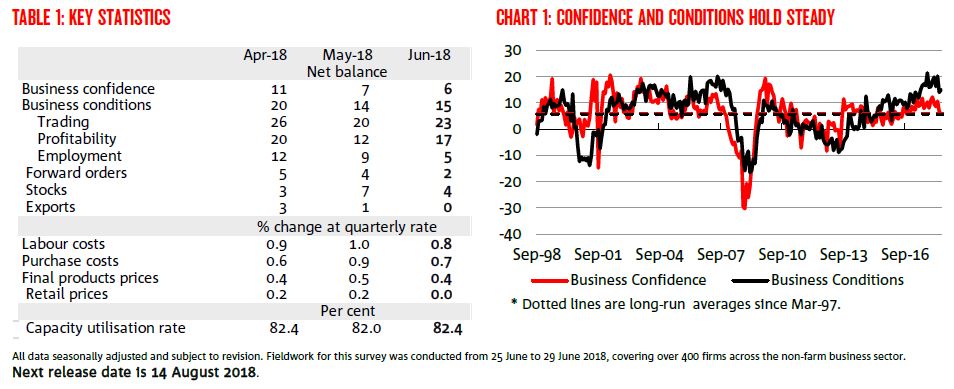

• How confident are businesses? The business confidence index edged down 1pt to +6 index points in June, continuing an around-average trend after easing back in recent months.

• How did business conditions fare? The business conditions index ticked up by 1pt to +15 index points after the pull-back in the previous month. Overall, conditions remain highly favourable with the index around 9 index points above the long-run average.

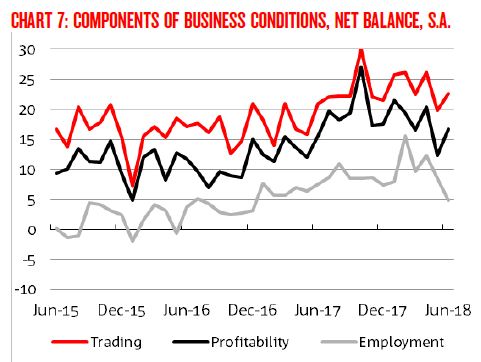

• What components contributed to the result? The trading and profitability indices rose in the month (by 3 and 5pts respectively), while the employment index declined for a second month in a row to +5 index points.

• What is the survey signalling for jobs growth? Despite two consecutive months of falls, the employment index – based on historical patterns – is consistent with jobs growth around 20k per month, slightly above the rate required to keep the unemployment rate constant.

• Which industries are driving conditions? Conditions improved in manufacturing, construction, wholesale and financial, property & business services in June. These gains were offset by a sharp decline in the mining industry, while transport & utilities and recreational & personal services also fell. Despite the sharp decrease in the month, in trend terms conditions remain strongest in the mining industry. Conditions in the retail industry continue to lag at +1pt in trend terms.

• Which industries are most confident? Confidence remains highest in trend terms in the mining and construction industries. Confidence, in trend terms, is lowest in recreation & personal services; the remaining industries remain at or around the national average in trend terms.

• Where are we seeing the best conditions by state? Conditions (in trend terms) remain most favourable in South Australia and Tasmania, though all states remain well above average. Conditions in Western Australia continue to lag the other states.

• What is confidence like across the states? Confidence is highest in trend terms in Queensland and Western Australia (both +12 index points) followed by South Australia (+10). Confidence in New South Wales and Victoria continues to lag the other states (+5 and +4).

• What does the Survey suggest about inflation and wages? Surveyed prices, costs and wages variables continue to suggest weak price pressures in the economy. Labour cost, purchase cost and final products prices growth all edged lower in June. Retail prices tracked sideways in the month, with no growth after increasing at a relatively low pace recently.

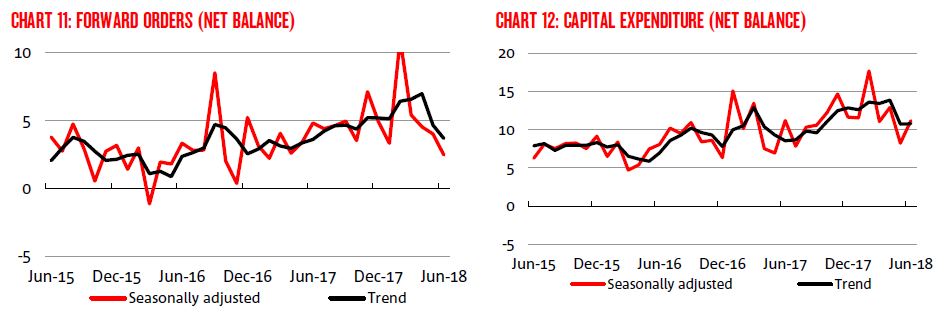

• Are leading indicators suggesting further improvement? Key leading indicators were mixed in the month. Capacity utilisation edged slightly higher in June, reversing the small decline in May and is at a relatively high level. Forward orders fell 2pts in June. In trend terms, both continue to point to a positive outlook for the non-mining economy.

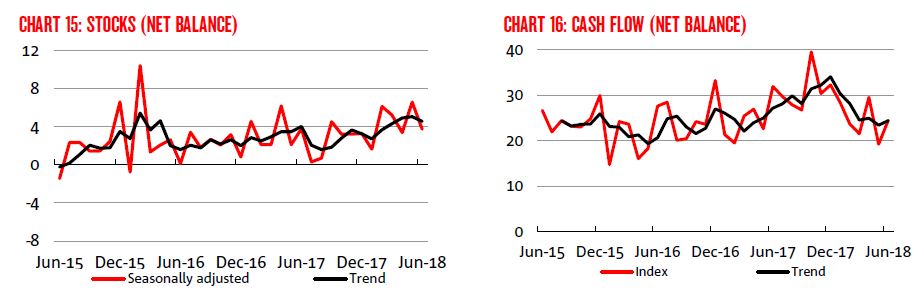

They should read their own survey. Headline numbers were unchanged but the underbelly is weakening fast with forward orders, stocks, employment, cash flow and capex all softening:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.