Australian house prices are gently falling. They are likely to fall further as credit conditions tighten. The big unknown, however, is how the fall in house prices will affect consumer saving. Recession is a risk, but not yet the investment base case.

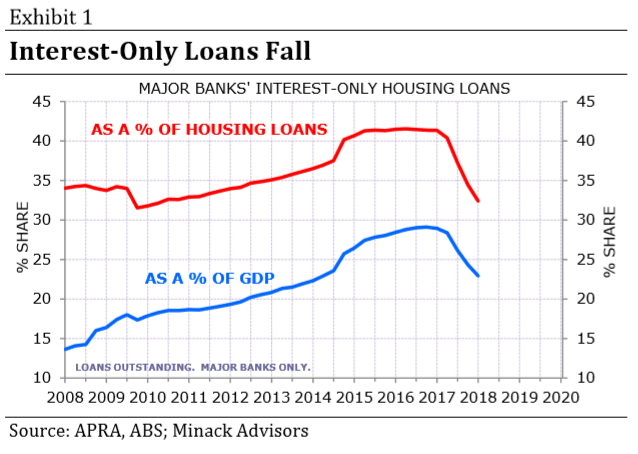

Several factors are now tightening credit conditions in the Australian housing market. First, regulators had asked banks to restrict lending to investors and interest-only loans. Second, some interest-only loans are now converting to principal & interest loans – leading to a substantial increase in debt service costs for those affected. Interest-only loans had peaked at 40% of all housing loans (Exhibit 1).

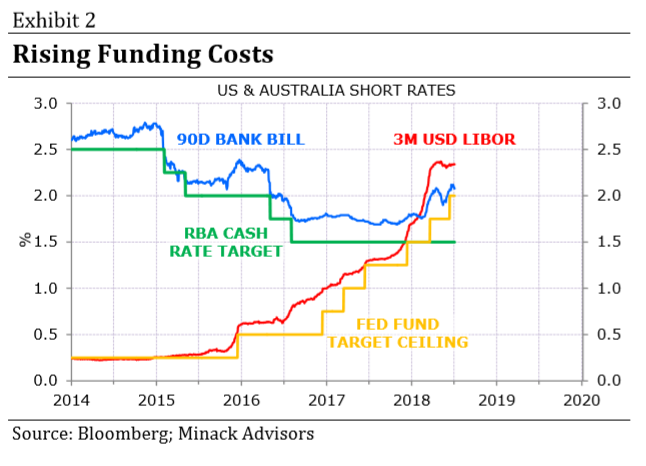

Third, funding costs are rising, both for US$-based funds – which are priced off LIBOR – and domestic wholesale funds as bank bill rates rise relative to the RBA cash rate (Exhibit 2). The result is that some second-tier lenders have increased mortgage rates, despite no change to the RBA policy rate.

Fourth, the Banking Royal Commission seems to have triggered a tightening in lending standards. This is the most difficult component to calibrate. More importantly, this process is driven by legal concerns, not by regulators, and therefore there’s greater risk of unintended consequences.

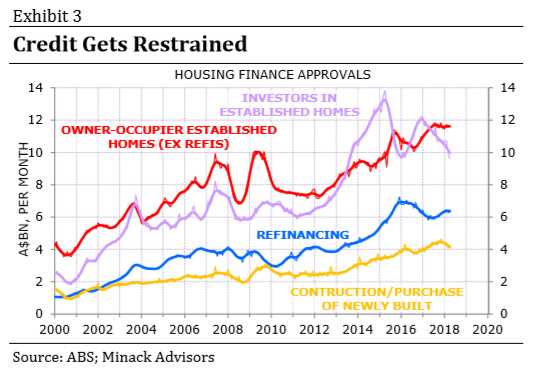

As a result housing finance approvals are now falling, particularly for investors (Exhibit 3 – note the data are up until April, and anecdotes suggest that credit conditions have tightened since.)

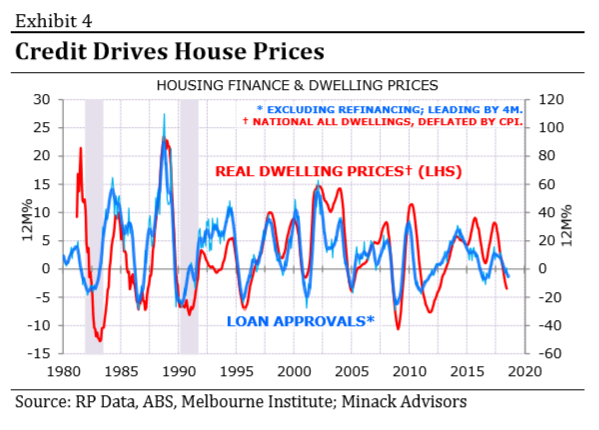

Most houses are bought on credit, so the demand for housing is a function of the supply of credit. Consequently, housing loan approvals have historically led house prices (Exhibit 4). New loan approvals have fallen by around 20% year-over-year several times over the past 25 years. If the current credit contraction is more severe – say, a decline of up to 30% – then nationwide house prices could fall high single digits over the coming year.

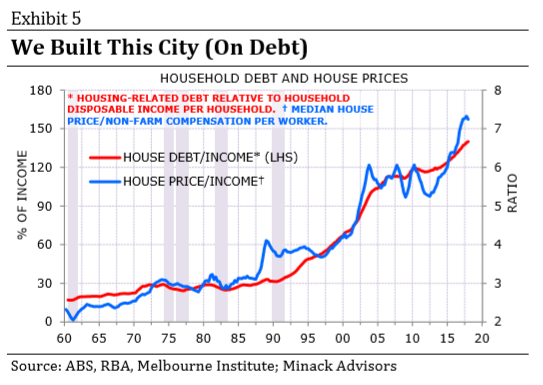

It may be that a slowdown in credit growth now could have an out-sized impact, for two reasons. First, house prices are now at record highs relative to income as is – not coincidentally – household debt relative to income (Exhibit 5). It may be that credit supply is more influential at higher prices.

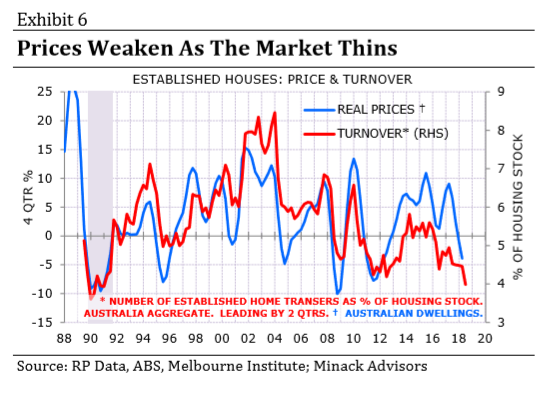

Second, the housing market looks ‘thin’, hinting that prices may be unusually sensitive to a change in demand. Historically housing market turnover tracked price growth. However, turnover has been soft relative to price gains over the past 3-4 years, and in the March 2018 quarter turnover fell to the lowest level since the 1990 recession (Exhibit 6).

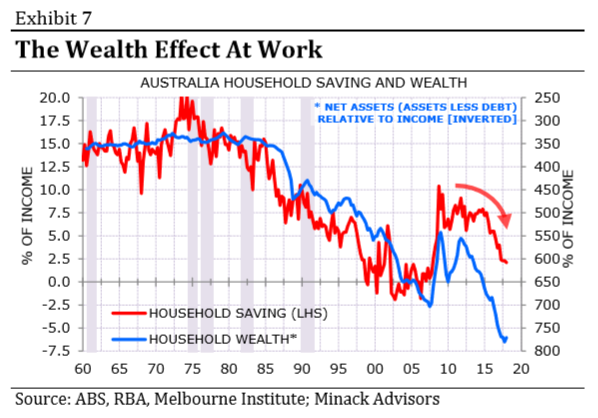

So there’s uncertainty about the extent of the credit tightening; and there’s also uncertainty about how any credit tightening will affect house prices. But the most important uncertainty is how any change in house prices – and household wealth generally – affects consumer saving behaviour. There is clearly a correlation between household wealth and saving (Exhibit 7). But the correlation is not so tight that it’s clear how the saving rate would change in response to, say, a 10% fall in house prices.

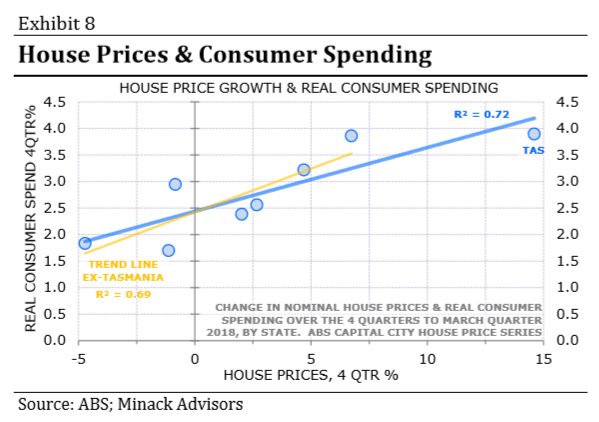

But let me have a stab at it: Exhibit 8, for example, shows a snapshot of real consumer spending by state and capital city house price growth over the past year. The best fit line implies that a 10% rise or fall in house prices lifts or damps real consumer spending by around 1¼%. The housing stock is now worth just over 7 times household income. So the response of consumer spending to a 10% change in housing wealth (~70% of income) implies the marginal propensity to consume from a change in housing wealth is around 1¾% – a fairly plausible (possibly conservative) estimate.

All this suggests that a high single-digit decline in house prices would put a material dent in domestic demand. If prices were to fall by, say, 15%, and if consumer income growth was as tepid as it now is, there would be a good chance of recession.