Treasuries were flogged as inflation expectations build with tariffs:

Advertisement

Bunds too:

Stocks firmed:

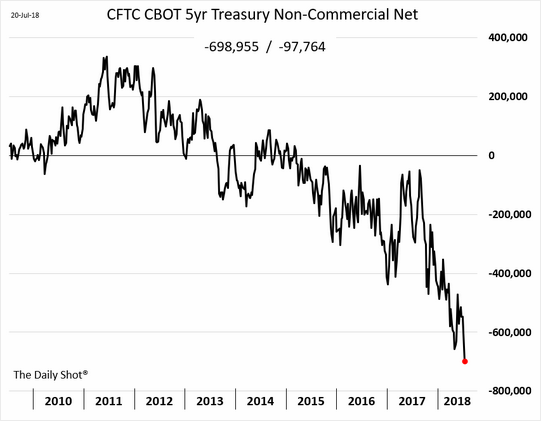

It’s US inflation versus Chinese deflation front and centre now. Treasury shorts are lifting as tariffs drive inflation expectations higher:

Advertisement

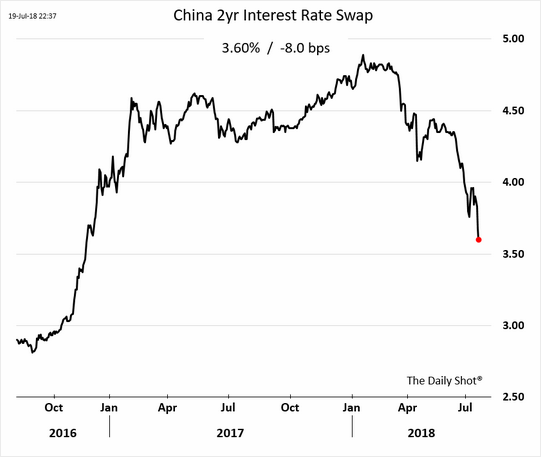

At the same time in China, it’s all deflation and bond buying:

Advertisement

Who will win? At the moment it looks like China, eventually. Trump is too confused in his tactics. But not yet.

So while we wait for global deflation to roar back, the CNY crashes with abandon, via FTAlphaville:

A weaker currency, the argument goes, makes China’s exports cheaper than global manufacturers’ and its imports pricier. This not only gives Chinese tariffs on US products more bite, but it could also blunt the impact of those piled on by the Trump administration. A 10-per-cent depreciation in the real effective exchange rate raises net exports by an average 1.5 per cent of GDP, according to the IMF.

But at the moment, China does not appear to be doing this.

The recent depreciation, says Marc Chandler of Brown Brothers Harriman, is more about the dollar than the renminbi. The greenback has strengthened against emerging markets and most major currencies like the euro, British pound, Japanese yen and both Aussie and Canadian dollars. Federal Reserve Chairman Jerome Powell’s upbeat assessment of the US economy and his nod to continued (if gradual) rate hikes this year and next has supercharged this dynamic.

And because the renminbi has strengthened relative to virtually every other emerging markets currency since January, a correction was due, points out Robin Brooks of the Institute of International Finance.

Other market forces played a part, adds Chandler.

Advertisement

“China’s economy has weakened, debt worries are growing, and they have eased monetary policy while forcing some deleveraging. Add to that tightening from the Fed, and for any country, the currency is probably going to fall.”

The only issue with that argument is that China manages the value of its currency, of course. Officials have had the ability to intervene at any point during the renminbi’s recent drop, which means they essentially chose to let it touch 12-month lows. But Calvin Tse of Citigroup writes that he does not expect Beijing to adopt a policy of using the renminbi to offset trade tensions.

“Authorities have deep scars from the 2015/2016 experience, where a rapid pace of currency depreciation drove excessive capital outflows, which net resulted in a large tightening of financial conditions.”

Advertisement

Weaponising the renminbi through a managed depreciation could resume this flight. Brooks believes it could lead to a repeat of the panic in 2015 and 2016. Worse, it could foil Beijing’s plans to put its financial system on firmer footing.

But if China chooses to escalate a trade war using its currency, it has the ammunition to do so, says Brad Setser of the Council on Foreign Relations. Using China’s balance-of-payments data from the first quarter of 2018 (the most recent available), Setser finds that the Middle Kingdom added about $100bn to its foreign assets, the fastest growth of official assets since 2014.

Reserves increased by about $25bn, while state banks extended their overseas lending some $55bn. Chinese financial institutions snapped up about $30bn of foreign bonds and equity, too.

Portfolio inflows also surged, topping $150bn—two-thirds of which came from foreign investors purchasing Chinese bonds. What flows in can also flow out, so the volume of capital flight could be higher if things take a turn for the worse this time around. That being said, China can also impose capital controls whenever it sees fit.

Just because China can initiate a currency war does not mean that it will. And it almost certainly will not make such a move lightly, given the very real risk that depreciation could run away from authorities and lead to a broader loss of confidence in domestic assets.

Still, some concern may be warranted if the currency makes further declines against the dollar, says Setser, because “it’s quite possible that the tariffs have changed China’s calculus.”

First quarter flows might as well be 19th century now. They were amid a crashing USD and the “global synchronised growth trade”. That’s ancient history.

In today slowing circumstances, the falling yuan is normal but the Chinese are still allowing it amid the trade war, saving their forex reserves for later if it comes to that.

Advertisement

For China to be forced to cough more of them up, the US will need to keep growing strongly and the Fed to keep hiking plus driving up the USD. This is where Trump is confused. He needs a higher USD to break China’s currency peg and force a reckoning on its domestic credit monster. It’s actually the opposite of a more limited trade war.

He’ll need to return to more stimulus soon if he is to achieve that end before the US fiscal tailwind exhausts itself in a year from now. We haven’t heard anything of the infrastructure push since February. Counter-intuitively, that’s what the US needs now to win its economic (as opposed to trade) war.

If not the CNY will just keep falling until deflation wins and the Fed buckles, letting China off the hook for risk-free domestic easing.

Advertisement

But we’re not there yet and while CNY falls so will AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.