DXY ran riot last night then crashed on Trump jawboning before rallying again. CNY is crashing. EUR falling:

AUD got sucked down as expected:

Though emerging markets fell even harder:

Advertisement

Gold was the same story:

Oil bucked the trend as Saudi jawboned prices higher:

Base metals were smashed:

Advertisement

And big miners:

Plus EM stocks:

Oddly, junk did better:

Advertisement

Treasuries were bought:

And bunds:

Stocks eased back:

Advertisement

Some are calling it panic stations for China already, via Nomura:

Stocks, Commods and EM on overnight lows with the Yuan decline accelerating (CNH to the lowest level in a year) as signs of accelerated easing / outright stimulus confirm the Chinese economic slowdown and credit crunch reality

Our Chinese Economics team highlights said “outright stimulus” shift-indications this week alone (note from last night attached):

Sharp decline in the Treasury deposit rate

A call from the chairman of the China Banking and Insurance Regulatory Commission to increase credit supply and significantly cut financing costs of small- and micro-sized enterprises

A possible new window guidance from the PBoC on using the MLF to encourage banks to increase loan supply and buy high-yield bonds, averting bond defaults

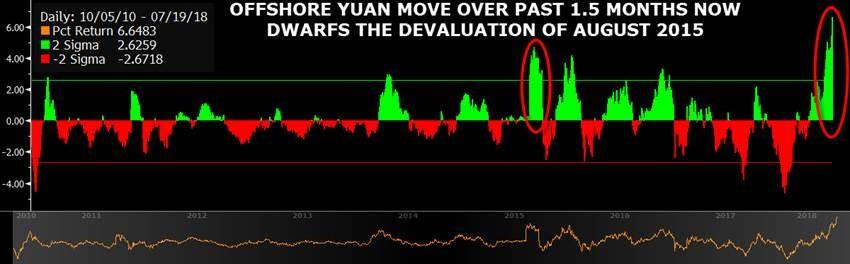

The cumulative move in offshore deliverable CNY (USDCNH) over the past 30 sessions is 6.6%, a 5 standard-deviation event across all returns over the past 10 years and now significantly larger than the devaluation of August ’15.

The implications of this Chinese “confirmed slowdown”—alongside the ambiguous / “edge-less” “trade war” noise—have driven the recent escalation of “global growth scare” which I have been discussing in my “Downshift” thesis since mid-June.

As experienced in the period following August ’15, the Yuan devaluation has the potential to trigger a global “disinflationary impulse” with stronger US Dollar NEGATIVELY impacting Commodities, and with it, global Fixed-Income, Equities and EM assets.

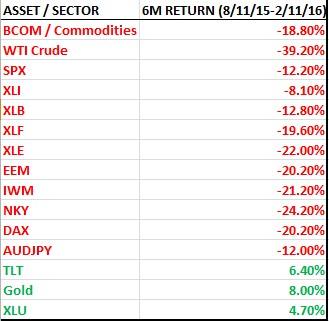

The cross-asset impacts in the 6 months following the August 11th 2015 devaluation were “beyond profound”—see table below.

All 15 major cross-asset markets studied by Quant-Insight which are “in regime” (“explainable by their macro factors”) have either “Metals & Agri”, “Inflation Expectations” or “Global Growth” as one of their top 3 price-drivers.

Cross-asset sentiment and performance trends have become increasingly “acute” both regionally and globally:

Asian currencies have continued to decline, with the ADXY -4.2% over the past month alone

MSCI Asia ex-Japan is -9.0% over the last month

Bloomberg Industrial Metals Index -17.1% over the past month

Shanghai Property Index -18.2% over the past month

Chinese 10Y government bond yields collapsing 60bps since late 4Q17 (4.04 to 3.44 last)

Significant trend reversal in U.S. Equities “Cyclicals over Defensives” positioning over the past two months, with “Cyc/Def” proxies -7.5%

But therein lies the rub as it pertains to the near-term risks to my “Downshift” call (where I have stated that “now is the time” to begin positioning portfolios more defensively / “up in quality” for late-cycle realities of “QE to QT”): as Chinese financial conditions further deteriorate and market stress worsens, we actually / perversely push CLOSER to the “RISK-ASSET POSITIVE” outcome of escalated PBoC stimulus- and easing- measures

Essentially, we are nearing the pain-point of the “PBoC Put”

The potential here is that “heavy-handed” measures from the PBoC in H2 could near-term stabilize or squeeze the Commodities / Materials space, in-turn boosting “global growth” positioning once again (positive for Commods / Inflation / Cyclicals, negative for USTs and global “Defensive” / “Flight to Safety” assets)

An additional “right tail” scenario is that the “worse” things get in China in the near-term, the more-likely it is that we too could see Chinese concessions in the “trade war” with the U.S., which could destroy market tension / volatility and drive a “gap higher” in risk sentiment

The actual longer-term impact of said POTENTIAL measures will remain to be seen, if deployed at all—the particulars, from Ting Lu et al:

“However, some of these measures could lead to even bigger problems in the medium- to long-term, although in the short term they might be able to stabilise both financial markets and economic growth. The actual impact remains to be seen. Banks may still be reluctant to invest in risky high-yield bonds even if the PBoC provides the funds via MLF, and markets could soon realise that forcing banks to buy high-yield bonds may not be positive for the banks’ health and market valuations. The monetary transmission channel could still be clogged if banks refuse to abandon their cautious stance. We expect more easing and stimulus measures, especially more pro-active fiscal policies, in H2 to mitigate strong headwinds on growth.”

YUAN’S “SLOW-BLEED” DEVALUATION = GLOBAL “DISINFLATIONARY IMPULSE

Source: Bloomberg / Nomura

30d CNH MOVE NOW DWARFING THE 2015 EVENT:

6m RETURNS ACROSS ASSETS / SECTORS FOLLOWING THE AUGUST 11, 2015 DEVALUATION:

Source: Bloomberg / Nomura

WHY THIS POTENTIAL “DISINFLATIONARY IMPULSE” FROM THE ONGOING YUAN DEVALUATION MATTERS TO MARKETS:

There’s no way that we’re at the panic stage yet for the PBOC. It is still in the “targeted easing” phase and growth is fine which is why the bulk commodities are still sitting this out. Moreover, it is still letting the yuan plunge so it’s clearly not yet concerned enough by capital outflow.

Advertisement

As well, the pain in broader emerging market debt and equity is still minor versus 2015. We’ll need at least a rerun of those depths to stall Fed hikes which is what China really needs if it to survive the trade war.

It’s onwards and downwards for the EM/commodity complex for now, including the Australian dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.