DXY rebounded strongly last night as CNY and EUR dumped:

AUD was wiped against developed markets (DMs):

And worse than some emerging markets (EMs):

Gold was hit:

Oil was firm:

Base metals were mixed:

Big miners were weak:

Along with EM stocks:

And junk:

And junk:

Treasuries were dumped:

Bunds too:

And stocks mixed:

First, the news. The ECB was dovish:

At today’s meeting the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.00%, 0.25% and -0.40% respectively. The Governing Council expects the key ECB interest rates to remain at their present levels at least through the summer of 2019, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to levels that are below, but close to, 2% over the medium term.

Regarding non-standard monetary policy measures, the Governing Council will continue to make net purchases under the asset purchase programme (APP) at the current monthly pace of €30 billion until the end of September 2018. The Governing Council anticipates that, after September 2018, subject to incoming data confirming the Governing Council’s medium-term inflation outlook, the monthly pace of the net asset purchases will be reduced to €15 billion until the end of December 2018 and that net purchases will then end. The Governing Council intends to reinvest the principal payments from maturing securities purchased under the APP for an extended period of time after the end of the net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

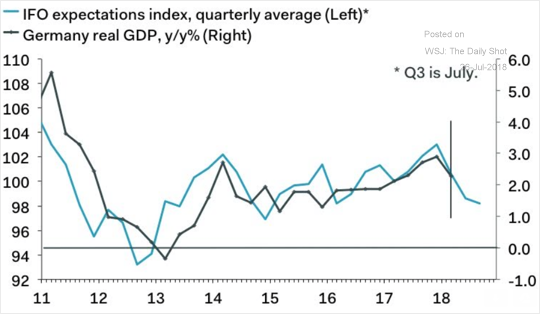

No surprises there given how fast the German IFO is falling:

Back to stagnation with a bullet!

But the big news is all about trade. A NAFTA deal is looming, via CNBC:

Treasury Secretary Steven Mnuchin told CNBC on Thursday a deal on NAFTA is coming in the near future.

“We hope to have an agreement in principle, clearly, very soon. That’s the first priority,” Mnuchin said on “Squawk Box.” “I think we’re making a lot of progress.”

The U.S., Mexico and Canada have been in talks to renegotiate the trade deal after President Donald Trump repeatedly bashed it by calling it the worst trade agreement ever.

Following the EU deal, we can see the shape of things to come. Goldman sums it up:

The announcement did not mention EU auto tariffs specifically, even though reducing the differential between the EU’s 10% tariff on auto imports and the US 2.5% tariff on cars has been a frequently cited White House goal. This could reflect internal EU disagreement over the issue or it could represent a strategy to save auto tariff reductions until later in the negotiation.

While the announcement is a clearly positive development, and was interpreted as such by financial markets, it is in some respects reminiscent of the state of US-China negotiations earlier this year after tariffs had initially been proposed. In that case, after initial negotiations regarding increased exports of agricultural and energy products, among other issues, Treasury Secretary Mnuchin declared that the trade war with China was “on hold”. That situation did not hold for long, however, and the proposed tariffs were eventually implemented earlier this month. The US-EU announcement is somewhat more specific and somewhat more likely to result in a formal agreement, but follow-through remains a clear risk.

.. these programs seem likely to give the Trump Administration more political flexibility to impose additional tariffs on imports from China, in our view. Rural voters voted disproportionately for President Trump in 2016 and most rural areas have Republican representatives in Congress. Retaliatory tariffs recently implemented by China are particularly focused on agricultural exports that would impose disproportionate economic losses in rural areas and could weaken support for the President’s trade agenda among these constituencies. Additional subsidies are likely to reduce this effect, though they will probably not reverse it entirely.

Overall, developments over the last few days suggest that risks from trade policy are becoming more concentrated on the US-China trade relationship. The preliminary US-EU agreement could lead the White House to believe that imposing tariffs on imports from China could increase the probability of a US-China agreement. With subsidies in place to guard against some of the domestic economic fallout from retaliatory tariffs, the White House is likely to have additional political flexibility to pursue that strategy.

Exactly. China has played this horribly. It overplayed its hand by reacting nationalistically. It overplayed its hand by reaching out to the EU and got slapped down. It overplayed its hand in jeopardising a fantastic deal on North Korean demilitarisation.

It’s now painted itself into a corner where to save face it has no choice but to do the very thing it was aiming to avoid, stimulate again. Martin Wolf looks at what that means:

The salient characteristics of a system liable to a crisis are high leverage, maturity mismatches, credit risk and opacity. China’s financial system has all these features. Among other things, China has a shadow banking sector, though a study by the Bank for International Settlements argues that “securitisation and market-based instruments still play only a limited role”. It is, in all, less complex and more directly connected to the banks than the US system was.

So why might the outcome in China be different than elsewhere?

…The strongest reply is that the government is powerful and has a well-run central bank, effective control over the banking system, ownership of vast domestic and foreign assets, untapped fiscal capacity and tight controls over transactions with, and by, foreigners. If it were determined to protect the financial system from collapse it could do so. But if gross debt were to rise above 400 per cent of GDP over the next decade, even that would be less certain.

Imagine, however, that there is a financial crisis. Would it be followed by lower growth? The answer is: yes, in both the short and long term.

…A crisis, then, would probably mean a recession in the short term. In the longer term, growth would also slow from current reported levels. That would be largely because a significant part of the credit-fuelled investment spending had been wasted, partly in building unneeded dwellings and excessive industrial capacity.

What about a more palatable world with no crisis? This would represent a soft landing. The longer the authorities take to control debt trends the more difficult it will be to achieve such an outcome. But this is clearly the animating principle behind current policy, which is aimed at strengthening the financial system and halting the trend towards higher debt. Just how difficult it will be to stick to those principles is shown by this week’s announcement of another round of infrastructure spending, in order to stimulate demand. That implies more investment and debt. But the trade war with the US may make such backsliding inevitable.

There is no way out. It’s take you medicine and shake out the misallocated capital or its extend and pretend and watch growth choke on more misalloacted capital.

So, Trump has China on the run. It is my view that he remains willing to do a deal. That’s his thing. But like all deal makers, the longer his prey waits and the weaker it gets the more Trump will demand. That’s been China’s most fatal mistake. It should have gone in hard and early, offering a big easy win to Trump so that it could keep cheating on everything else for years to come. Now it’s been outed and as the world falls in behind Trump, it is shaping up as bare-knuckled fight between him and China.

How can the AUD do anything but fall amid that fight?

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book (or PMICO is!). Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.