Treasuries were bashed at the short end. The curve crashed:

Advertisement

Bunds were sold:

Stocks took off with NASDAQ leading at new record highs:

Advertisement

So, is this an inflexion point? There are reasons to think so. China is stimulating again, via a breathless Bloomie:

The Beijing “put” is back.

China’s bid to boost policy stimulus to barricade its domestic economy from the brewing trade war is breathing life into risk assets battered by liquidity and geopolitical angst.

Among the winners: Asian junk bonds, the besieged industrial-metals complex and emerging-market stocks.

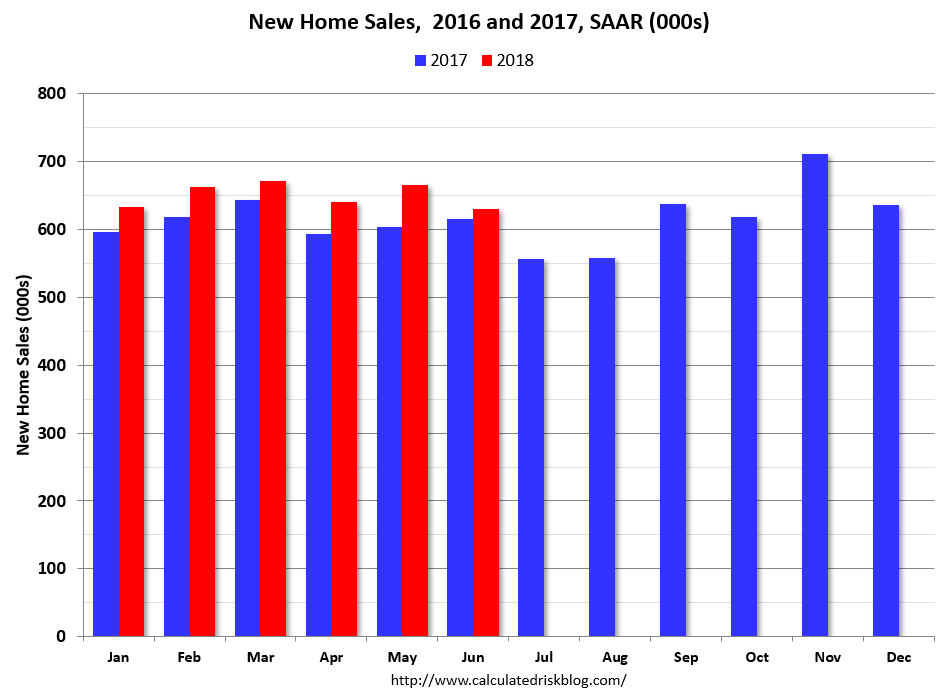

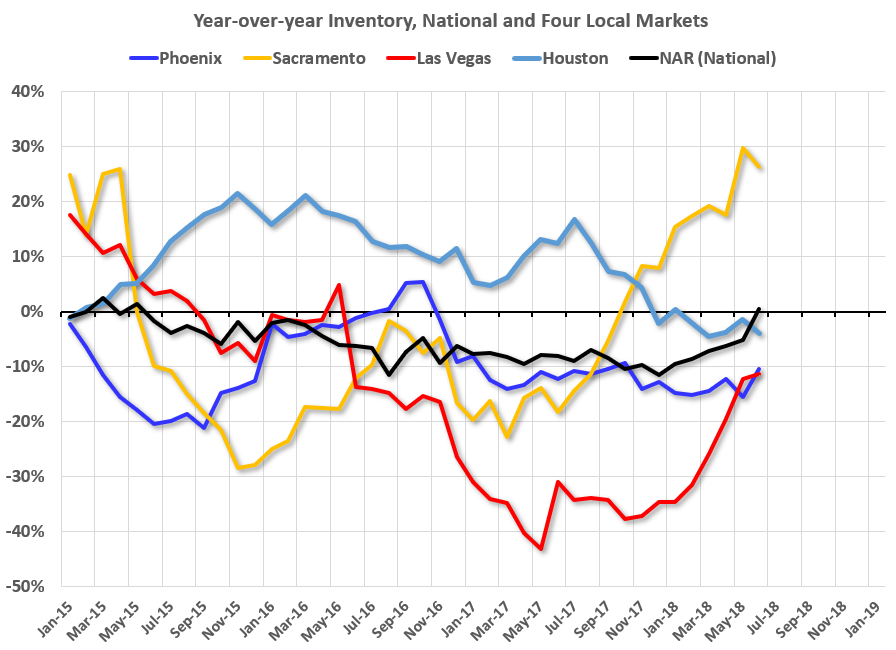

Also, with Trump’s new anti-dollar rhetoric aimed at the Federal Reserve, the USD is struggling. As well, tightening is starting to impact the economy with housing markets off the boil as existing home sales slow though still up year-on-year:

Advertisement

Inventory has begun to rise and prices may slow:

We have Q2’s big GDP print looming but every economist and his dog now expects the US to slow from here. Added to that are many reports that are calling slower growth arising from tariffs. Though that rather hangs on the notion that the USD keeps rising to match the tariffs.

Advertisement

That is probably the key. Will markets respond to tariffs by shifting production onshore into the US? Or will they respond by moving offshore thanks to rising costs and higher USD? Not to mention possible side deals in NAFTA and the EU. And moves today by the US senate to block auto-tariffs.

Is any of this enough to repeat the early 2016 experience of the pivot from liquidity withdrawing from the EM periphery to flowing outwards to it? Not yet, in my view.

The Chinese stimulus, such as it is, is big enough only to slow the slowing. Nor is the Fed is done yet. If anything, tariffs are giving it more to think about regarding the durability of rising inflation. I don’t think that we can assume Trump rhetoric will impact its reaction function.

Advertisement

Despite the flattening yield curve, US recession fears are overblown for now:

As well, wages are still steadily accelerating.

Advertisement

We may see a short term rally for risk assets, possibly even tradable for a bit. But if the USD falls much it will again fire up its overheating manufacturing sector and multi-national profits that are already booming. Thus any shift towards risk assets will benefit US shares anyway and any forex updraft be more than offset in equity gains.

So, for now, I don’t see any reason for a lasting turn up for the Australian dollar nor any need to shift positioning from the MB Fund’s overweight US position.

David Llewellyn-Smith is chief strategist at the MB Fund which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book. Below is the performance of the MB Fund since inception:

If the ideas above interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.