Over the long weekend, DXY and EUR were roughly stable:

The market is now a little less hilariously long EUR:

AUD was soft against DMs:

EMs are still struggling vs AUD:

The market pulled its AUD short in a little last week:

Gold is flat:

Oil bottoming:

Base metals soft:

And big miners:

EM stocks still look bad:

And EM junk:

Treasuries are poised for a flogging:

Bunds are eating dust:

Italian debt got short squeezed as the Finance Minister said it’s all the way with EUR and Interior Minister cut immigration:

US stocks are on the march, European caught a break:

It’s all about the Fed this week. Another rate hike is all but certain and we’re building towards two more in H2, via Calculated Risk:

The consensus is that the Fed will increase the Fed Funds Rate 25bps at the meeting this week, and the tone will remain upbeat.

Assuming the expected happens, the focus will be on the wording of the statement, the projections, and Fed Chair Jerome Powell’s press conference to try to determine how many rate hikes to expect in 2018 and in 2019.

Here are the March FOMC projections.

Current projections for Q2 GDP range from 3.1% to 4.5%. GDP increased at a 2.2% real annual rate in Q1. This puts first half GDP close to the top of the expected range, and GDP projections might be revised up.

GDP projections of Federal Reserve Governors and Reserve Bank presidents Change in

Real GDP12018 2019 2020 Mar 2018 2.6 to 3.0 2.2 to 2.6 1.8 to 2.1 Dec 2017 2.2 to 2.6 1.9 to 2.3 1.7 to 2.0 1 Projections of change in real GDP and inflation are from the fourth quarter of the previous year to the fourth quarter of the year indicated.

The unemployment rate was at 3.8% in May. So the unemployment rate projection for 2018 will probably be lowered.

Unemployment projections of Federal Reserve Governors and Reserve Bank presidents Unemployment

Rate22018 2019 2020 Mar 2018 3.6 to 3.8 3.4 to 3.7 3.5 to 3.8 Dec 2017 3.7 to 4.0 3.6 to 4.0 3.6 to 4.2 2 Projections for the unemployment rate are for the average civilian unemployment rate in the fourth quarter of the year indicated.

As of April, PCE inflation was up 2.0% from April 2017. Based on recent PCE readings, PCE inflation will likely be revised up for 2018.

Inflation projections of Federal Reserve Governors and Reserve Bank presidents PCE

Inflation12018 2019 2020 Mar 2018 1.8 to 2.0 2.0 to 2.2 2.1 to 2.2 Dec 2017 1.7 to 1.9 2.0 2.0 to 2.1 PCE core inflation was up 1.8% in April year-over-year. Core PCE inflation might also be revised up for 2018.

Core Inflation projections of Federal Reserve Governors and Reserve Bank presidents Core

Inflation12018 2019 2020 Mar 2018 1.8 to 2.0 2.0 to 2.2 2.1 to 2.2 Dec 2017 1.7 to 1.9 2.0 2.0 to 2.1 In general the data has been somewhat firmer than the FOMC’s March projections, so it seems likely the FOMC will be on track for four rate hikes in 2018.

Whether the Fed will squash the AUD this week will depend upon the dot plot above. If it indicates two more hikes this year then yes. If it remains at three then no.

It’s a by-the-by anyway. Nothing has changed in three days. The US is booming. Europe fading. China slowing. It is a formula for more monetary tightening in the US than anywhere else, more trouble for EMs and more US dollar strength plus AUD weakness.

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

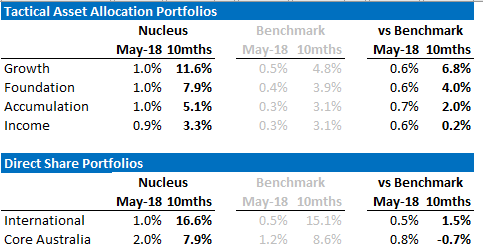

The recent performance of both is below:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.