I can’t believe I’m still addressing this question but here we go again, via the AFR:

The Australian dollar is perceived to be a fair-weather currency, tending towards strength when investor risk appetite is high and the global economic outlook is benign.

On the other hand, the $A tends towards weakness when investor risk appetite is down. In fact, data suggests that the association between a weaker $A and risk-off environment is deeper than the firm $A/risk-on relationship.

The $A’s fair-weather character has been constructive for Australian investors with overseas assets during global market sell-offs, as the weaker Australian dollar has helped to protect the value of overseas holdings.

…Some wonder whether such free-kicks may now be in danger as the $A stays put despite current market ructions stemming from Italy sliding into deep political uncertainty…Through it all, the $A has been relatively stable, falling just 0.75¢, barely a blip given the move in safe haven bonds. This is not supposed to happen. The $A should be weaker.

But before anyone concludes that the $A has joined the safe-haven club, there are a few things to consider.

The Australian dollar may not yet be under pressure because markets have decided for now, at least, that Italy is a European problem, and the issue will be confined to Europe.

That is the most important point. The Italian crisis has so far lasted for one week. It’s been chaotic rather than growth threatening (though I think it will become the latter).

If we look at the history of the AUD and real growth-damaging crises then pattern is clear:

- during the 1990s recession it fell -29%;

- during the LTCM/Asian crisis then dot com busts it fell -42%;

- during the GFC it fell -39%;

- during the first European debt crisis it fell -16% despite being in the midst of 150 year mining boom.

If Italy leaves the Eurozone it will be as bad if not worse than the GFC given it will instantly render large parts of the French and German banking systems insolvent. That will, in turn, trigger a global banking freeze as global counter-parties shut off the liquidity tap.

Australia will be impacted more than most given our banks our very dependent upon global and European financing.

You can be quite sure that the Australian dollar will crater along with risk assets everywhere, remaining “constructive for Australian investors with overseas assets during global market sell-offs, as the weaker Australian dollar has helped to protect the value of overseas holdings”.

———————————————

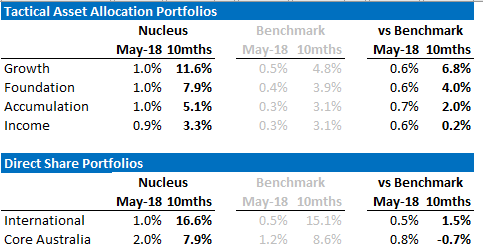

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.