EUR cratered last night and DXY took off:

AUD was slammed against developed markets (DMs):

And weaker than emerging markets (EMs):

Gold held on:

Oil was flat:

Base metals mixed:

Big miners fell:

EM stocks look ominously poised for lower:

As EM junk leads the way down. Even worse for EM, US junk is recovering!

US yields rose but the curve flattened:

Bunds were bid bigly:

So was Italian debt:

Stocks roared in Europe and lifted in the US:

It’s all about the dovish ECB. God knows why anybody expected anything else given the cratering data but the market got whip-lashed:

Since the start of our asset purchase programme (APP) in January 2015, the Governing Council has made net asset purchases under the APP conditional on the extent of progress towards a sustained adjustment in the path of inflation to levels below, but close to, 2% in the medium term. Today, the Governing Council undertook a careful review of the progress made, also taking into account the latest Eurosystem staff macroeconomic projections, measures of price and wage pressures, and uncertainties surrounding the inflation outlook.

As a result of this assessment, the Governing Council concluded that progress towards a sustained adjustment in inflation has been substantial so far. With longer-term inflation expectations well anchored, the underlying strength of the euro area economy and the continuing ample degree of monetary accommodation provide grounds to be confident that the sustained convergence of inflation towards our aim will continue in the period ahead, and will be maintained even after a gradual winding-down of our net asset purchases.

Accordingly, the Governing Council today made the following decisions:

First, as regards non-standard monetary policy measures, we will continue to make net purchases under the APP at the current monthly pace of €30 billion until the end of September 2018. We anticipate that, after September 2018, subject to incoming data confirming our medium-term inflation outlook, we will reduce the monthly pace of the net asset purchases to €15 billion until the end of December 2018 and then end net purchases.

Second, we intend to maintain our policy of reinvesting the principal payments from maturing securities purchased under the APP for an extended period of time after the end of our net asset purchases, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

Third, we decided to keep the key ECB interest rates unchanged and we expect them to remain at their present levels at least through the summer of 2019 and in any case for as long as necessary to ensure that the evolution of inflation remains aligned with our current expectations of a sustained adjustment path.

Today’s monetary policy decisions maintain the current ample degree of monetary accommodation that will ensure the continued sustained convergence of inflation towards levels that are below, but close to, 2% over the medium term. Significant monetary policy stimulus is still needed to support the further build-up of domestic price pressures and headline inflation developments over the medium term. This support will continue to be provided by the net asset purchases until the end of the year, by the sizeable stock of acquired assets and the associated reinvestments, and by our enhanced forward guidance on the key ECB interest rates. In any event, the Governing Council stands ready to adjust all of its instruments as appropriate to ensure that inflation continues to move towards the Governing Council’s inflation aim in a sustained manner.

Let me now explain our assessment in greater detail, starting with the economic analysis. Quarterly real GDP growth moderated to 0.4% in the first quarter of 2018, following growth of 0.7% in the previous quarters. This moderation reflects a pull-back from the very high levels of growth in 2017, compounded by an increase in uncertainty and some temporary and supply-side factors at both the domestic and the global level, as well as weaker impetus from external trade. The latest economic indicators and survey results are weaker, but remain consistent with ongoing solid and broad-based economic growth. Our monetary policy measures, which have facilitated the deleveraging process, continue to underpin domestic demand. Private consumption is supported by ongoing employment gains, which, in turn, partly reflect past labour market reforms, and by growing household wealth. Business investment is fostered by the favourable financing conditions, rising corporate profitability and solid demand. Housing investment remains robust. In addition, the broad-based expansion in global demand is expected to continue, thus providing impetus to euro area exports.

This assessment is broadly reflected in the June 2018 Eurosystem staff macroeconomic projections for the euro area. These projections foresee annual real GDP increasing by 2.1% in 2018, 1.9% in 2019 and 1.7% in 2020. Compared with the March 2018 ECB staff macroeconomic projections, the outlook for real GDP growth has been revised down for 2018 and remains unchanged for 2019 and 2020.

The risks surrounding the euro area growth outlook remain broadly balanced. Nevertheless, uncertainties related to global factors, including the threat of increased protectionism, have become more prominent. Moreover, the risk of persistent heightened financial market volatility warrants monitoring.

According to Eurostat’s flash estimate, euro area annual HICP inflation increased to 1.9% in May 2018, from 1.2% in April. This reflected higher contributions from energy, food and services price inflation. On the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around the current level for the remainder of the year. While measures of underlying inflation remain generally muted, they have been increasing from earlier lows. Domestic cost pressures are strengthening amid high levels of capacity utilisation, tightening labour markets and rising wages. Uncertainty around the inflation outlook is receding. Looking ahead, underlying inflation is expected to pick up towards the end of the year and thereafter to increase gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

This assessment is also broadly reflected in the June 2018 Eurosystem staff macroeconomic projections for the euro area, which foresee annual HICP inflation at 1.7% in 2018, 2019 and 2020. Compared with the March 2018 ECB staff macroeconomic projections, the outlook for headline HICP inflation has been revised up notably for 2018 and 2019, mainly reflecting higher oil prices.

Taper but no rate hikes forever. The market is positioned for much more hawkish.

So, we now have a hawkish QT Fed and dovish QT ECB, just as expected. This was underlined again last night as US retail sales boomed while Europe wrestles with weak growth and political meltdown.

Ambrose Evans-Pritchard sums up the implications nicely:

(i) The US Federal Reserve has given an unequivocal warning today that it will not be deflected by currency mayhem in emerging markets. Chairman Jay Powell might as well have told half the world to drop dead. The combined policy of the Fed, the European Central Bank, the Bank of Japan, and the Bank of England (G4 bloc) will be contractionary within months, perhaps dangerously so if the monetarists are right. China is shifting briskly in the other direction to avert an investment bust and a corporate default scare. But monetary easing by Beijing stores up a different kind of problem down the road. It may weaken the yuan and set off capital outflows, akin to the currency drama of early 2016. Not even China can escape the Impossible Trinity.

(ii) …as the Fed raises rates a seventh time to 2pc, and the ECB prepares – perhaps this week – to signal the end of its vast bond market adventure. The unwinding of quantitative easing implies a loss of $2 trillion (£1.5 trillion) in annual net stimulus by December, compared to peak QE in early 2017. Nobody knows what the consequences will be as the Fed reverses the process at an accelerating pace, lifting bond sales to $50bn a month by early autumn.

(iii) Nor does anybody know what rising borrowing costs will do to a global system habituated to a decade of zero rates and emergency liquidity… The world has never been so leveraged, and therefore so sensitive to a monetary squeeze. The Institute of International Finance says world debt reached 318pc of GDP at the end of 2017, 48 percentage points higher than the bubble-peak just before the Lehman crisis… Emerging market debt has jumped from 145pc to 210pc. That is where the trouble is brewing. It is a near mathematical certainty that the currency crisis in Argentina and Turkey – already nibbling at Brazil, South Africa, and Indonesia – will spread to the rest of the emerging market nexus and detonate a systemic crisis…

(iv) The ECB is turning down the spigot in tandem, but largely for political reasons that it cannot admit. The economic rationale is weak. Core inflation remains pinned to the floor at 1.1pc. The real M1 and M3 monetary aggregates are flashing amber. The eurozone economy has slowed to stall speed. It will reduce bond purchases to zero by the end of the year. It is doing so under ideological pressure from the northern “German” bloc… rips away the ECB shield for Italy. Mario Draghi’s “do whatever it takes” no longer holds. There is no sovereign backstop except on political conditions that Rome will not lightly accept. Bond markets are certain to test this. It is not hard to imagine a self-fulfilling crisis.

The ECB has just locked in the next EM crisis. As EUR falls and DXY rises, EM debt and equity will evaporate, monetary and fiscal tightening will accelerate and growth falter. The next shoe to drop is a slowing China and commodity prices.

This will initially reward DM markets with lower yields and higher equity before the contagion eventually wends its way back to the centre as US fiscal stimulus fades.

The Australian dollar only has one way to go in these settings, exacerbated by its own slowdown as fiscal stimulus plateaus and housing falls.

Down, down.

David Llewellyn-Smith is the chief strategist at the MB Fund which is overweight US equities. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

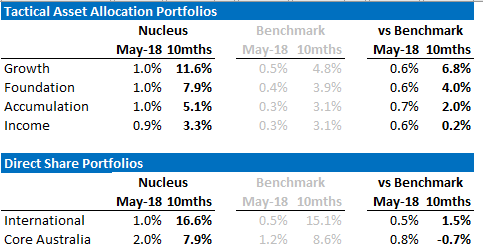

The recent performance of both is below:

If these themes interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.