It’s a seductive thought for immigration extremists like Greg Jericho:

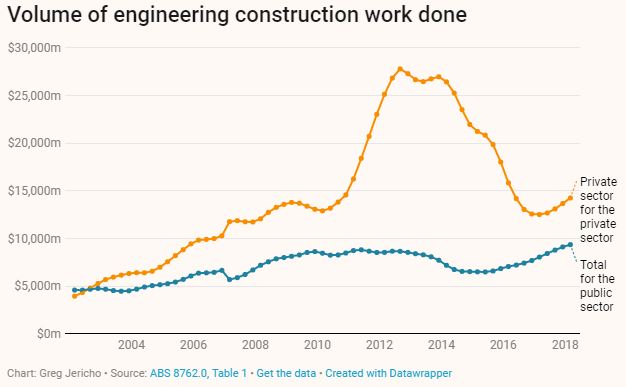

In the September quarter of 2012, the volume of engineering construction work done reached a record level of $36.5bn. And then it fell off a cliff. Within four years the value had almost halved as mining companies ended their construction of mines and shifted to the production and export phase.

The winding down of this investment was a serious drag on the economy, but it now appears to be over.

For over a year now engineering construction has been rising, and while public infrastructure spending has been a big reason, the good news is that spending by the private sector is also improving:

But even with this growth it is quite astonishing to see how much engineering construction has fallen. Over the past 12 months there was $53bn less engineering construction work done than occurred during the peak 12 months period to March 2013:

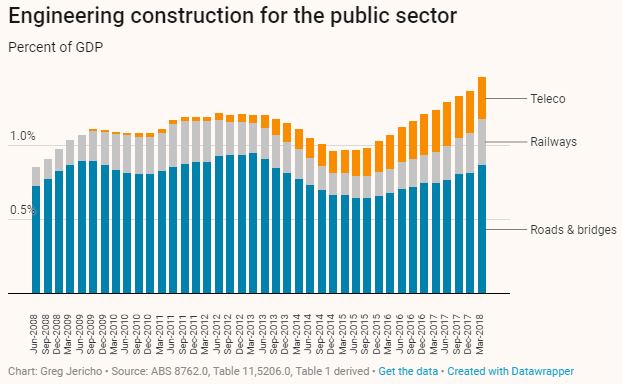

The great change that has occurred over the past five years however is highlighted when you note that the drop in engineering construction in the mining states of Western Australia, Queensland and the Northern Territory has been so great that for the first time since 2005 the value of construction in the non-mining states is larger:

Rather than be led by the mining states, the big driver of infrastructure is now coming from New South Wales and Victoria.

Over the past year engineering construction spending in New South Wales rose by 25% and in Victoria a rather stunning 38%.

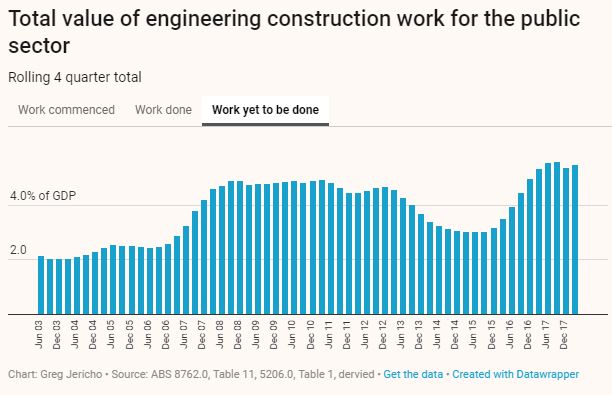

When we look ahead we also see that this is set to continue as a massive pipeline of public infrastructure work comes on line. The level of public sector infrastructure work to be done over the next few years well surpasses that of the GFC stimulus spending:

As I noted recently, the private sector in Australia remains less than ebullient, and while this data highlights the sharp falls of private sector investment from the end of the mining boom are now over, the public sector infrastructure projects remain absolutely crucial for keeping the economy growing, and look set to remain so for a number of years to come.

Wrong. Here’s the chart:

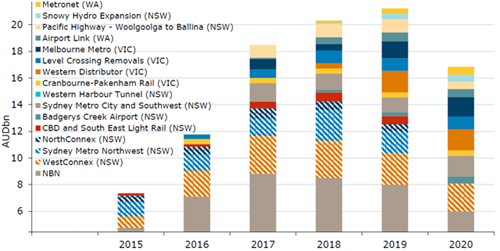

All of the growth in these projects is derived from the rate of change in spending not the aggregate. It doesn’t matter how big it is if it is not bigger than last year.

Advertisement

Thus, most of the growth is behind us already. There’s a little more next year but then projects begin run-off and a cliff forms much like the mining version before it that withdraws from growth.

No doubt more projects will be concocted to keep the plateau high but there’s no way we’ll be able to keep growing the rate of change to add GDP and jobs.

This is yesterday’s Botox Boom. It’s peaking now and is, for all intents and purposes, over.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.