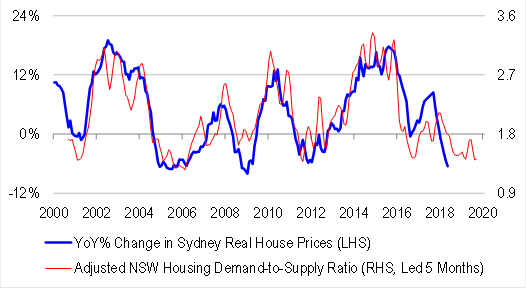

Twice before Australia has managed to backfill its housing bubble. From 2003-2009 we did it thanks to the mining boom driving huge income and rental gains, despite falling prices in Sydney. Again in 2010-13 we backfilled it with mining boom redux plus fiscal stimulus. Today we are trying the same with an immigration and fiscal boom. Can it succeed? Via Damien Boey at Credit Suisse:

Surprisingly solid retail sales growth in April

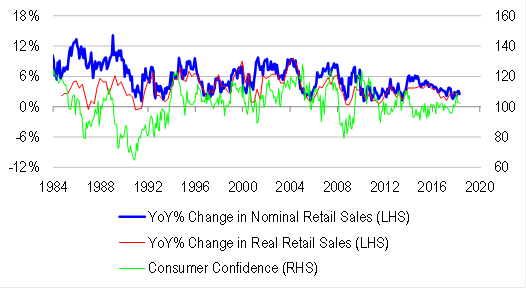

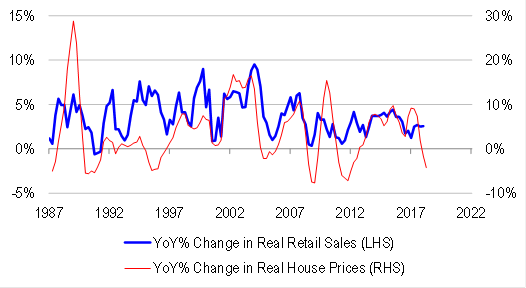

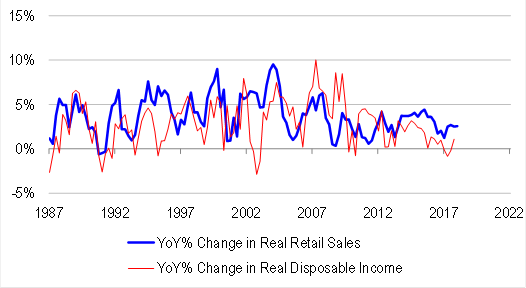

Retail sales came in above expectations, rising by 0.4% in April, compared with the Consensus forecast for 0.3% growth. For context, some higher frequency partial indicators, such as the NAB cashless retail index, had been pointing to contraction in spending over the month. As such, the actual April reading came as a very pleasant surprise. However, looking through the monthly volatility, the numbers do not look very positive in trend terms, with year-ended growth slowing to 2.5% from 3.2%.

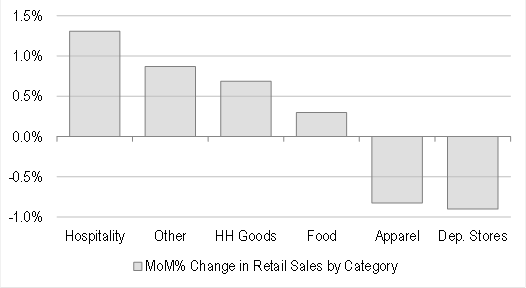

Compositionally, the report was quite mixed. Food spending rose moderately. Among the discretionary components, hospitality, household goods and other categories rose strongly. But department store and apparel sales were weak.

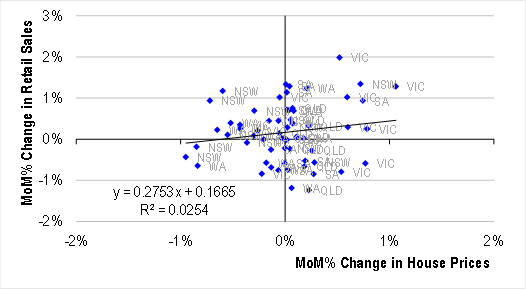

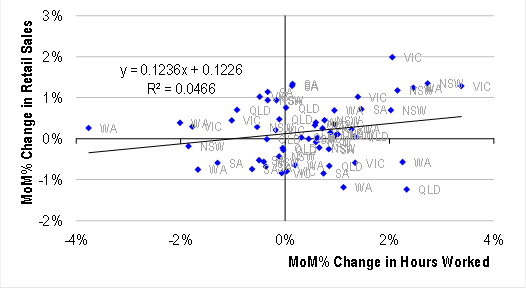

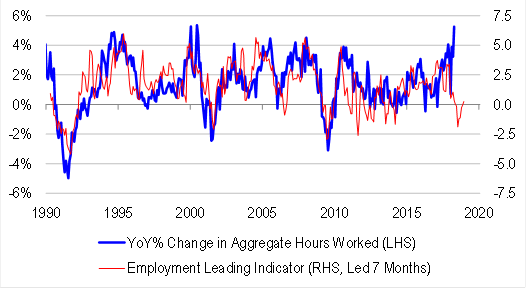

Looking at the regional picture over the past year, the states that experienced the strongest (weakest) spending gains tended to be the ones experiencing the strongest (weakest) jobs growth and the fastest (slowest) house price inflation. Interestingly, the correlation with labour market conditions has strengthened over the correlation with housing market conditions. Arguably, this temporarily vindicates the RBA’s position that housing market weakness need not have calamitous consequences for consumer spending if jobs growth is solid.

Outlook is still concerning

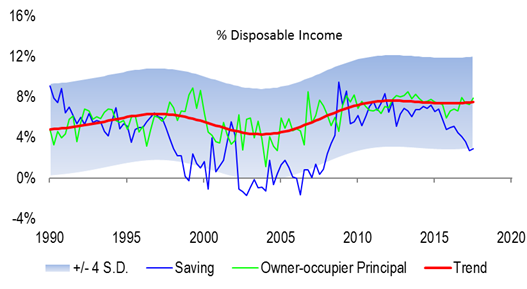

The trouble with the April data is that probably has not yet encompassed recent tightening of credit conditions and collateral damage on housing markets. But it will have fully accounted for the strength of labour market conditions. Taking these considerations on board, the April bounce in retail spending could prove to be quite short-lived. After all, the leading indicators point to more weakness in house prices, and slower labour income growth … And the household saving rate is woefully inadequate to cover required principal payments on amortizing debt.

Policy and investment implications

Consumption bounced in April, but the consumer is not yet out of the woods. Many of the downside risks recognized by policy makers are still in play. The good news is that for once, the strength of labour market conditions has provided a buffer against de-leveraging pressures. But the bad news is that the labour income impulse could very easily fade from historically high levels, while downward pressure on asset prices could get materially worse.

For now, the RBA remains comfortably on hold, and the partials help to vindicate the Bank’s stance. But there are a host of new risks that the Bank will need to consider that are likely to reshape the outlook going forward. We are most concerned about incremental credit market tightening coming through, and impairment of the monetary transmission mechanism.

I don’t think we can do it. The immigration rat wheel economy intrinsically saps wages and income. More rate cuts and a lower dollar will aid the backfilling but then we’ll be out of ammunition and completely exposed to the next global shock.

Looks to me like our housing bubble luck has run out.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.