Gold is breaking down, suggesting more DXY strength ahead:

Oil took off:

Base metals sank:

Advertisement

EM stocks sank:

EM junk sank:

Treasuries were bid:

Advertisement

Not bunds:

Or BOTS:

Stocks firmed modestly:

Advertisement

US data was still good with consumer confidence strong, Richmond and Philly Fed strong and house prices marching on.

Trump backed away from some escalation on China, via WSJ:

If Mr. Trump’s decision holds through June 30, when the new policies are scheduled to be announced, it would represent a significant backing away from threats the president has made against China and a possible olive branch to Beijing before the July 6 impositon of tariffs on $34 billion of Chinese goods.

…It would also mark the end, for now, of the ascendancy of the so-called nationalist wing represented by White House trade adviser Peter Navarro and U.S. Trade Representative Robert Lighthizer. The two camps have jockeyed for power for months over the China issue and the battle is sure to continue.

…Industry lobbyists and China experts who follow the issue closely attribute the shift to recent declines in the stock market and to U.S. companies getting battered by tariffs in U.S. trade battles with the European Union, Canada, Mexico and China.

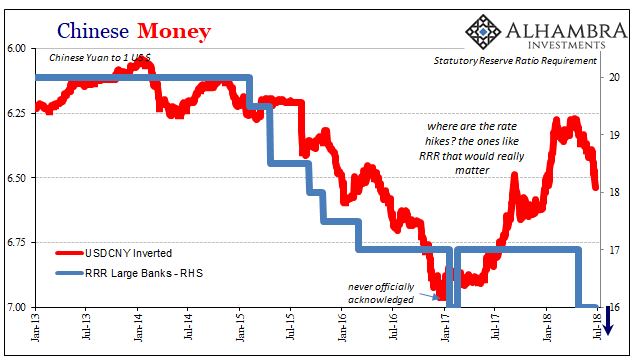

Like 2015, in 2018 we know that the PBOC and the rest of China’s various government authorities want nothing to do with CNY DOWN. On August 12, 2015, the PBOC issued a statement which read:

Looking at the international and domestic economic situation, currently there is no basis for a sustained depreciation trend for the yuan.

Yeah, they all lie when it suits them. There was every basis for CNY’s move, therefore a more honest declaration would have said, “a falling yuan is bad for everyone, so we hope that by admitting this isn’t us devaluing on purpose it’ll stop because we just spent a ton trying to make it stop and we couldn’t get it to.”

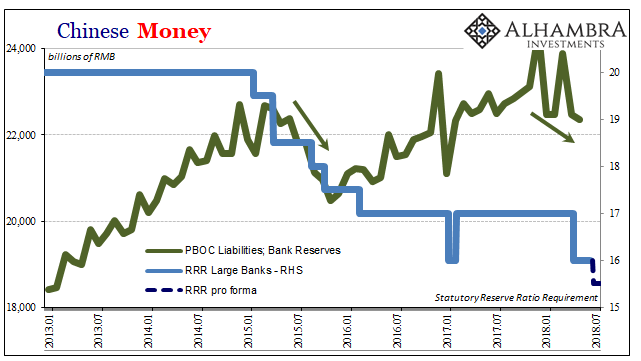

These things have internal consequences, too. The amount of dollars on the PBOC’s balance sheet, the synthetic long, directly affects the level of RMB bank reserves available to the domestic Chinese banking system. It’s simple central bank accounting.

Over the weekend, the PBOC announced a second cut to the RRR rate this year (2018). The central bank had offered a targeted 100 bps reduction in April tied to repayments in the MLF. This latest one, slated for July 5, will be for 50 bps.

This flies in the face of pretty much every conventional assumption about China. In monetary policy terms, the PBOC is supposedly “tightening” because China’s economy is about to take off (sounds a lot like three years ago). Reducing the RRR is contrary to that narrative. Doing it twice is emphatically so.

As noted last week, Chinese bank reserves are contracting again like they were during the middle of 2015. Unsurprisingly, at least from the non-textbook perspective, a lower RRR corresponds to this particular circumstance. A reduction in the required rate for reserves means that private banks don’t have to hold back as much of them, meaning they can use proportionally more for monetary and financial purposes.

And if the overall level of reserves were to decline, then the lower RRR would offset much or all of the contraction in the general balance in the RMB marketplace (in theory). But that raises the important question, why doesn’t the PBOC just keep expanding bank reserves rather than risk upsetting internal RMB conditions by introducing complications and uncertainties? The experience in 2015 demonstrated the dangers.

I’ve already explained the straightforward answer, but here I want to put it in these same terms of China’s “dollar short.” Throughout 2016, the PBOC did do just that. Chinese central bankers “printed” RMB, raising the asset level on their balance sheet so that the liability side could expand somewhat, too, leaving a larger remainder (bank reserves).

But the balance of forex assets was declining sharply at the same time, meaning that Chinese money was in danger of becoming more and more unbacked by anything other than its secretive framework and unpredictable often political intrusions. This sort of risk becomes embedded in the rate eurodollar banks will charge Chinese banks to borrow dollars.

It is not a static charge, either, as the premium demanded to compensate for uncertainty rises and falls with perceptions about uncertainties. If eurodollar banks are already uneasy, then adding to their unease by more and more uncovering RMB money can only further pressure CNY. On the other hand, reassuring them by maintaining a predictable and steady monetary base could, potentially, offset some of that risk premium.

To stop the uncovering necessarily requires an end to the RMB “printing.” That’s exactly what’s been done over the last few months, repeating what had been done during the worst of 2015. And repeating also 2015, the RRR cuts are meant to try and offset any RMB illiquidity arising from purposefully fewer bank reserves.

Will it work? A terribly convoluted plan developed along unclear lines carried out across several dimensions including both offshore and onshore money centers where contradictory behavior is often determined by the same thing at the same time and in which the vast majority of conventional commentary is perpetually confused as to what’s taking place, what could go wrong?

The very fact that this is what they are up to tells you quite a lot about how things may be going over there. But if you think actual devaluation, it’s impossible to determine.

There are a few different elements to it this time around, though, which are important to point out.

First, I don’t think it was the PBOC starting in April who dumped Chinese banks all at once onto eurodollar markets like August 2015. Rather, I would guess that it was the tap out from Hong Kong banks that then (at the margins) unloaded China’s funding demands onto the global money market.

Second, it doesn’t seem like the PBOC is willing to expend resources directly as it was in early 2015 (and throughout CNY’s prior fall). At least not yet. The direct expense of forex is, again, tantamount to buying time. It doesn’t seem as if monetary authorities are even bothering with that this time around, suggesting a more definitive exercise. In eurodollar terms, that would amount to a starkly different interpretation.

In 2015, they may have been trying to ride out the “rising dollar” hoping that it would straighten itself out (at least as far as the Asian “dollar” might have been concerned) if given enough time. Now? Batten down another hatch. That’s the RRR.

CNY is falling again and one thing is certain. It isn’t devaluation.

Hmm, it’s quite right that the market is tearing up CNY as the Fed blows up the peg with rate hikes that China follow. But it is the unwillingness to spend forex reserves to stabilise CNY that is the devaluation.

Advertisement

So long as China crashes CNY, EMs will fall and commodities plus the AUD will follow in due course.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.