The EUR bear market rally took another leg up last night and DXY fell:

AUD was up and away versus DMs tracking EUR:

But EMs are still telling a different story:

Advertisement

Gold is stuck:

Oil fell:

Base metals went sick, mostly on particular supply issues:

Advertisement

Big miners to the moon!

EM stocks rallied like clockwork as DXY fell:

But EM junk ain’t buying it:

Advertisement

As Treasuries were flogged:

And bunds:

Italian debt is on the nose again but contagion is non-existent:

Advertisement

US stocks took off and European wilted:

The prime driver on the evening was a recalcitrant ECB:

Advertisement

ECB’s Praet (Dovish) said inflation expectations are increasingly consistent with their aim, post QE forward guidance on policy rates will then have to be further specified. He further added that markets are expecting an end of QE at end of 2018, this is an observation and input that is up for discussion and that it is clear that next week will need to discuss end of QE program.

ECB’s Hansson (Hawk) said the ECB could lift rates before mid-2019 due to “moderately” rising inflation. (Newswires)

ECB’s Weidmann (Hawk) said that inflation is now expected to gradually return to levels compatible with their target, adding that market expectation of end of QE by end of 2018 is plausible.

ECB’s Knot (Hawk) said it is reasonable to end QE soon inflation outlook is stable and less dependent on stimulus. He adds that the ECB should wind down QE as soon as possible.

Mario Draghi is on the verge of a watershed moment in the European Central Bank’s efforts to leave behind its crisis-fighting monetary policy.

Chief Economist Peter Praet on Wednesday signaled the bank’s first formal round of talks on when to stop buying bonds is imminent. That would start the process of bringing down the curtain on stimulus efforts that have resulted in almost 2.5 trillion euros ($2.9 trillion) of bond purchases since 2015.

…“The bottom line is that this is the end,” said Nick Kounis, head of macro and financial markets research at ABN Amro Bank NV in Amsterdam. “This is a signal that the ECB judges that the inflation conditions to wind down net asset purchases have been met.”

Advertisement

There’s an oil pulse headed to Europe that’ll lift inflation for a while but it’s a false signal. The ECB does have a history of overreacting so it may be about to make Europe’s growth slide even worse.

So the rabble-rousing by Italy’s lawmakers risks reinforcing the fear that QE is too politically charged to use in a fractious environment like the euro zone. Some central bankers may prefer to stop it rather than getting more embroiled in politics.

From an Italian perspective, the populist complaints are foolhardy brinkmanship. The ECB’s top brass is already set to discuss next week what should happen to asset purchases when they reach their scheduled end in September. Peter Praet, the ECB’s chief economist, said on Wednesday that there were “improving” signals of inflation converging toward the objective of “close to, but below” 2 percent. Investors took notice. The yield on all euro zone bonds, including Italy’s, rose sharply.

The governing council will make its decision on the basis of the economic outlook. But by talking so much, the populists may just have given it an extra reason to step back.

Advertisement

We know that the ECB is a weapon of Brussels, either implicitly or explicitly. So, expect Italian debt conditions to get worse fast if the ECB raises the temperature on tightening.

As the ECB applies the heat the new populist government will quickly be required to abandon its fiscal loosening or issue mini-BOTs (new lira) to cover it. Meanwhile, Italian banks will see capital flight intensify both from deposits and equity:

Advertisement

The latest polls still have EUR skeptics in the ascendant:

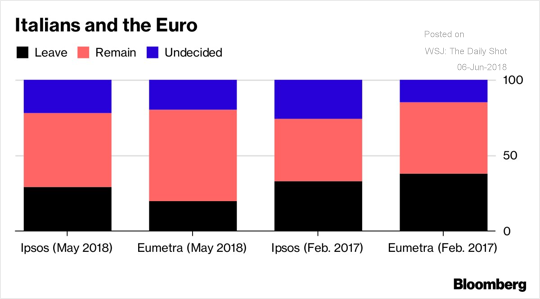

But, paradoxically, more Italians want to keep the EUR:

Advertisement

It’s still not obvious to me why anyone would want to own EUR. This is a powder keg.

—————————————————————

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

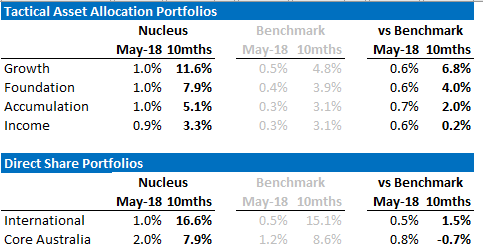

The recent performance of both is below:

Advertisement

If these themes interest you then contact us below.

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.