Friday night saw a little gain for EUR and stable DXY:

The hilarious EUR long remains massive:

But AUD was smashed against developed markets (DMs). It closed at new lows versus USD:

Advertisement

Here’s a closer look at AUD/USD:

AUD CFTC positioning shifted less bearish at -15k contracts:

Advertisement

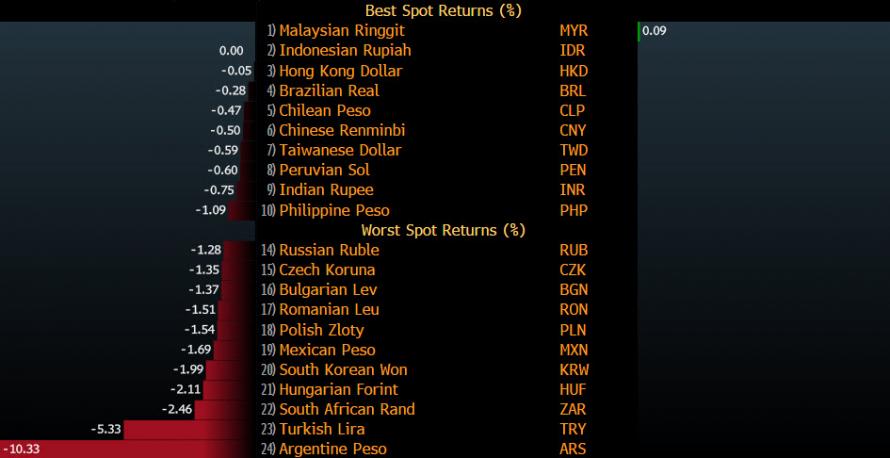

AUD was also weaker than most emerging market (EM) FX:

Which is really saying something given last week’s carnage:

Advertisement

Gold broke:

Oil broke:

Copper broke:

Advertisement

Miners broke:

EM stocks broke:

EM junk held on:

Advertisement

Treasuries were bid:

Bunds too:

Italian debt is the man!

Advertisement

Stocks were soft:

US data was solid with the NY Fed index surging, consumer confidence booming and industrial production soft. US GDP forecasts for this quarter are still booming. BofAML is at 3.7%, Goldman at 4%, the Fed’s GDPNow is at 4.8%!

Advertisement

The big news was tariffs as the G2 trade war is go, via FT:

Beijing announced it would retaliate against new US tariffs on $50bn in Chinese imports that will go into effect within days, taking the world’s two largest economies to the brink of a full-scale trade war.

The new American import duties, aimed at forcing Beijing to stop what the White House claims has been systematic theft of US intellectual property, will apply to products ranging from cars and helicopters to bulldozers and industrial tools and machinery.

China’s commerce ministry responded on Friday that it would “immediately introduce countermeasures of the same scale and strength”, though it did not immediately provide a full list of the tariffs or details about when they would be imposed.

“All the economic and trade-related achievements previously reached by the two sides will be rendered invalid,” the ministry said, referring to the results of earlier rounds of China-US trade talks.

It’s all old news so didn’t impact things too much. The key for markets is that the more tariffs that Trump applies, the higher will be US output and inflation (to a point), so the trade war only exacerbates US late cycle leadership in growth and monetary tightening. This was too much for commodities and the AUD which puked into the weekend.

Advertisement

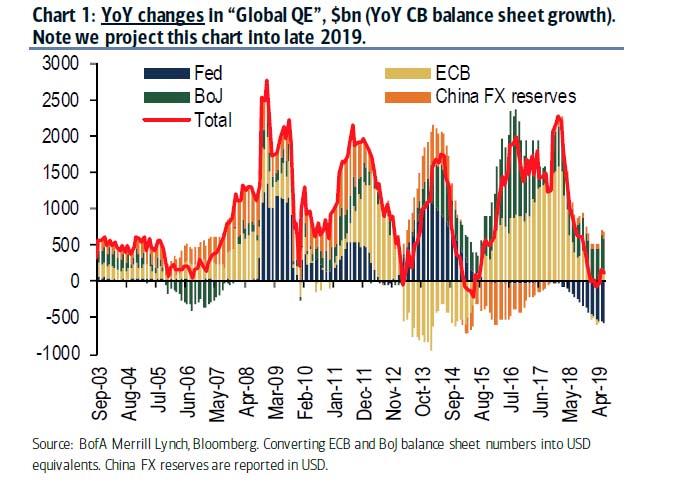

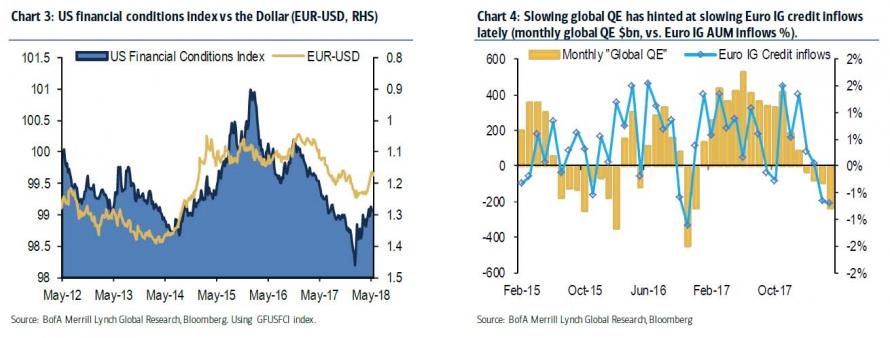

A measure of the severity is the global USD tightening already triggered by the Fed was offered by BofAML:

Note how fast the YoY growth in global QE has declined of late. What’s behind such a quick drop? The ECB has been purchasing fewer bonds in ‘18 and China FX reserve growth has cooled (on the other hand, BoJ QE has been relatively stable, and the Fed continues with modest balance sheet run-off).

…the volume of monthly global QE buying has declined significantly over the last two months, commensurate with the USD appreciation.

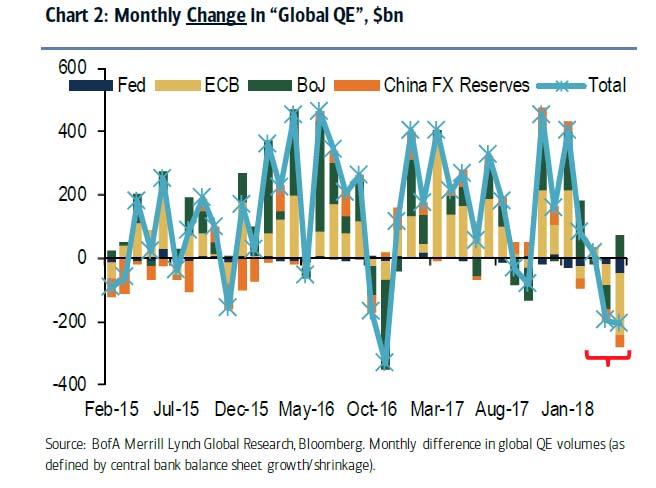

True to form, there has been a reasonable relationship over time between the monthly rate of change of our global QE numbers (in USD terms) and inflows into European IG credit funds. Put another way, slowing global QE means less crowding into risky assets more broadly…which points to less credit inflows (chart 4).

Which brings us back to this key chart that I use every day, EM junk versus US junk bonds:

Advertisement

The road to hell is paved with the carcasses of emerging market high yield debt. Right now, not only is EM high yield in free fall, worse, US junk is recovering. This is unprecedented thanks to Trump’s late cycle fiscal stimulus. As Moody’s notes, the US junk default rate is tumbling:

The overall pace of high-yield borrowing activity dropped by 5.7% annually during 2018’s first five months despite a decline by the average high-yield default rate from January-May 2017’s 5.0% to January-May 2018’s 3.7%. In addition, high-yield borrowing activity has yet to respond positively to a projected slide by the high-yield default rate from its 3.8% average of the three months ended May 2018 to the prospective 2.0% for the three-months-ended May 2019. Nevertheless, if the default rate declines to the 2.6% now projected for December 2018, yearlong 2018’s high-yield borrowing activity is expected to eke out a gain of 3% annually, wherein a projected 12% increase by new bank loan programs outweighs an expected 12% drop by bond offerings.

Growth by high-yield borrowing would be consistent with the 85% of previous year-over-year declines by the default rate that were joined by an annual increase for the moving 12-month sum of high-yield borrowing activity. For example, May 2018’s year-to-year 0.3 of a percentage point dip by the default rate to 3.7% was accompanied by a 5% annual increase for the high-yield borrowing activity of the 12-months-ended May 2018. By contrast, when the default rate rose by 3.6 percentage points yearly to July 2016’s 5.8%, the sum of the high-yield group’s bond issuance and new loan programs contracted by 9% annually during the year-ended July 2016.

Advertisement

That means the Fed is free to keep on tightening into the EM carnage, ensuring that the periphery keeps taking the pain in tightening monetary and fiscal policy as capital outflow accelerates.

The tumble in commodity prices and the Australian dollar Friday night is a warning of what comes next as EM (and China) growth slows. That, in turn, is anchoring DM long bond rates, supporting in particular US asset prices which, in turn, encourages more Fed tightening.

This is the MB Fund’s “reverse decoupling” thesis writ large that is delivering out-sized late cycle returns to Aussie investors positioned in US assets.

Advertisement

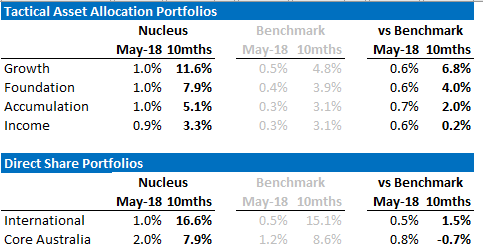

David Llewellyn-Smith is the chief strategist at the MB Fund which is overweight US equities. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

If these themes interest you then contact us below.

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.