But that is worrying markets. Ray Dalio’s Bridgewater especially:

2019 is setting up to be a dangerous year, as the fiscal stimulus rolls off while the impact of the Fed’s tightening will be peaking.

Markets are already vulnerable, as the Fed is pulling back liquidity and raising rates, making cash scarcer and more attractive – reversing the easy liquidity and 0% cash rate that helped push money out of the risk curve over the course of the expansion. The danger to assets from the shift in liquidity and the building late-cycle dynamics is compounded by the fact that financial assets are pricing in a Goldilocks scenario of sustained strength, with little chance of either a slump or an overheating as the Fed continues its tightening cycle over the next year and a half.

…while such strong conditions would call for further Fed tightening, there’s almost no further tightening priced in beyond the end of 2019. Bond yields are not priced in to rise much, implying that the yield curve will continue to flatten. This seems to imply an unsustainable set of conditions, given that government deficits will continue growing even after the peak of fiscal stimulation and the Fed is scheduled to continue unwinding is balance sheet, it is difficult to imagine attracting sufficient bond buyers with the yield curve continuing to flatten.

We are bearish on financial assets as the US economy progresses toward the late cycle, liquidity has been removed, and the markets are pricing in a continuation of recent conditions despite the changing backdrop.

The removal of liquidity is much more of a problem for EMs than it is the US. As Indian central bank chief Urjit Patel argues at the FT:

Dollar funding of emerging market economies has been in turmoil for months now. Unlike previous turbulence, this episode cannot be attributed to the US Federal Reserve’s moves on interest rates, which have been rising steadily since December 2016 in a calibrated manner.

The upheaval stems from the coincidence of two significant events: the Fed’s long-awaited moves to trim its balance sheet and a substantial increase in issuing US Treasuries to pay for tax cuts. Given the rapid rise in the size of the US deficit, the Fed must respond by slowing plans to shrink its balance sheet. If it does not, Treasuries will absorb such a large share of dollar liquidity that a crisis in the rest of the dollar bond markets is inevitable.

Consider the scale of both events. Starting in October 2017, the Fed began reducing reinvestment of the coupons it receives from debt securities holdings. That shrinkage will peak at $50bn a month by October and total $1tn by December 2019. Meanwhile, the US fiscal deficit is projected to be $804bn in 2018 and $981bn in 2019, implying net issuance by the US government of $1.169tn and $1.171tn, respectively, in the two years.

So, the withdrawal of dollar funding by the Fed, as it reduces its reinvestment of income received, is proceeding at roughly the same pace as that of net issuance of debt by the US government. Over the next few years, the government’s net issuance will stabilise, albeit at a high level, whereas the Fed’s balance-sheet reduction will keep rising.

This unintended coincidence has proved to be a “double whammy” for global markets. Dollar funding has evaporated, notably from sovereign debt markets. Emerging markets have witnessed a sharp reversal of foreign capital flows over the past six weeks, often exceeding $5bn a week. As a result, emerging market bonds and currencies have fallen in value.

There are now three drains on liquidity not two. When you add Italexit risk, which makes EUR un-investable, then you get a default rising US dollar draining even more liquidity .

I’m sure Mr Patel knows the answer: ‘it’s our dollar but it’s your problem’. Hike rates mate.

As I’ve said before, this is all pretty normal for a Fed tightening cycle. Places like Argentina, Turkey and Venezuala are known unknowns expected to get into some kind of trouble as late cycle tightening transpires. The thing that will shake markets sooner or later is the unknown unknown victim. Until that appears there is no need for the Fed to stop.

It could be China, which we know will slow during H2, probably adding commodity prices to the list casualties, via Bloomie:

Chinese companies must repay a total of 2.7 trillion yuan of bonds in the onshore and offshore market in the second half of this year, and together with another 3.3 trillion yuan of trust products set to mature in the second half, the problems may get worse. More than eight high-yield trust products have delayed payments so far this year.

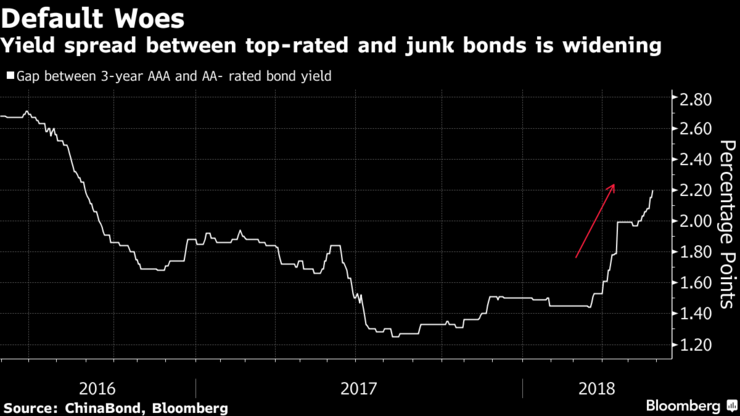

…In an indication of the recent pressures on weaker firms, the yield premium of three-year AA- rated bonds over similar-maturity AAA notes has widened 72 basis points since March to 225 basis points, the highest level since August 2016, according to Chinabond data.

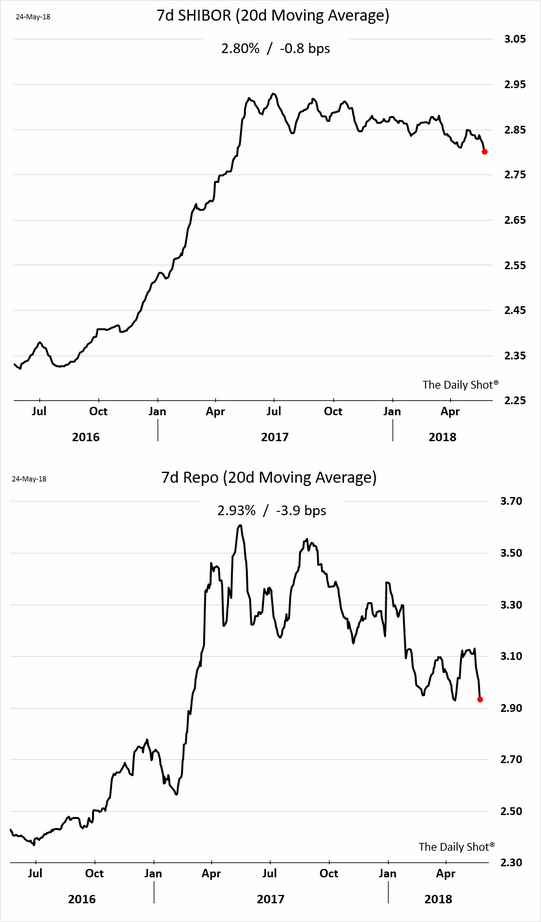

This is despite the PBOC guiding money market rates lower as it also aims to prevent China from slowing too fast:

The accident could be somewhere else altogether. We can never know and that’s the point.

Beyond the very short term, Australian dollar has nowhere to go but down.

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

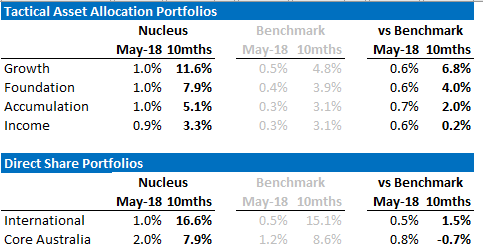

The recent performance of both is below:

If these themes interest you then contact us below.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Markets are already vulnerable, as the Fed is pulling back liquidity and raising rates, making cash scarcer and more attractive – reversing the easy liquidity and 0% cash rate that helped push money out of the risk curve over the course of the expansion. The danger to assets from the shift in liquidity and the building late-cycle dynamics is compounded by the fact that financial assets are pricing in a Goldilocks scenario of sustained strength, with little chance of either a slump or an overheating as the Fed continues its tightening cycle over the next year and a half.