AUD was hammered across all developed markets (DMs):

Emerging markets (EMs) were weaker still:

Sadly, CNY is crashing too:

Advertisement

Gold was soft:

Oil was soft:

Base metals were slammed:

Advertisement

Big miners too:

EM stocks are on the road to hell:

Though EM junk held on:

Advertisement

Treasuries were bid:

And bunds:

Italian debt sold:

Advertisement

Stocks fell though came off the lows:

The emerging markets rout is getting worse and will intensify. EUR is under pressure form the ECB as Draghi went dovish in a speech, via the FT:

Mario Draghi reinforced his dovish message on the European Central Bank’s retreat from ultra-loose monetary policy, saying interest rates would only rise at a slow pace from September next year.

As it called time on three years of quantitative easing during which it bought €2.4tn of bonds to prop up the economy, the ECB last week shifted its focus to a more conventional tool — interest rates.

The bank said last Thursday that it expected rates to remain at record lows “at least through the summer” of 2019, leading most investors to bet on early autumn for the first rate increase. In a speech about that change in the message on rates at the bank’s annual Sintra conference on Tuesday, Mr Draghi said:

“This enhanced forward guidance clearly signals that we will remain patient in determining the timing of the first rate rise and will take a gradual approach to adjusting policy thereafter.”

Advertisement

It’s no wonder, the runaway EUR has killed Europe. As well, Japan has done what Japan does and slowed. Meanwhile, the US powers ahead, via UBS:

What bounce? Our DM real GDP now-cast model (see “DM hard data nosedives”) accurately predicted the slowdown in DM growth from 2.4% in Q4 to 1.6% in Q1. We had presumed that this ‘soft patch’ would be temporary and that by end-Q2 DM growth would be back above 2% (for reference: the 2010-2017 average for DM is 1.8%). The simple logic was that (i) most of the Q1 weakness was temporary (bad weather, disruption from strikes, and a German flu that took 7% of the labour force off line), (ii) surveys were still sitting firmly in expansionary territory, and (iii) there was simply no logical explanation why DM growth would suddenly fall off a cliff. However, based on the available data thus far for Q2—we have 83% of the April data but only 52% of the May data—we are tracking DM growth at only 1.44%, below the Q1 level (see Fig 1).

Strength in the US…… The weakness in the DM now-cast may seem odd in light of the strength of the US data. We are formally tracking US Q2 GDP growth at 3.8%, and it may well be in excess of 4% (the Atlanta Fed is tracking at 4.8% on a higher inventory estimate). That tracking estimate is done by our US team which maps data releases into national accounts, i.e. it is separate from the ‘judgment-less’ factor augmented MIDAS model we use here for DM growth as a whole. That model (based on 70 indicators) is useful in helping sift through the barrage of DM data, but it is not a substitute for bottom up GDP tracking. In any event, the hard data component of the factor model is showing a 180bp acceleration in Q2 US growth (albeit from an under-predicted Q1 base)— broadly in line with the acceleration the US team is tracking.

…but substantial weakness in Europe and beyond. It will surprise no one that Europe is dragging down the DM now-cast in Q2 (weakness in IP, strikes in France), but what is perhaps surprising is the extent of the weakness (even though our model includes variables of supposed strength such as labour market indicators and consumer confidence). Fig 5 shows how Eurozone growth appears to be tracking at only 0.5% annualized, less than a third of the disappointing Q1 outcome. That’s for the full model (r-square 0.9); the ‘hard data’ component is worse, pointing to a slight contraction (-0.2%). The caveat is that we are using only a subset of large Eurozone economies to avoid skewing the factor to a particular region of DM. Our Eurozone team is tracking the hard data in Europe roughly unchanged from Q1 (at a bit over 1% annualized) and the survey data are still consistent with a modest bounce. Interestingly, the ‘DM ex US’ now-cast estimate does not improve if we exclude the Eurozone from the data, highlighting that the weakness is not limited to Europe.

US dollar broke out last night and it can only go higher from here. Its strength will be aided further by the trade war with China which will, in the short term, boost both output and inflation. As well, in response, China is already letting the yuan tumble.

Advertisement

That means all major currencies ex-US are under pressure leaving a one way bet for a strong DXY with the corollary that the EM crush will get much, much worse before it gets better.

The Australian dollar is in free fall now.

——————————————–

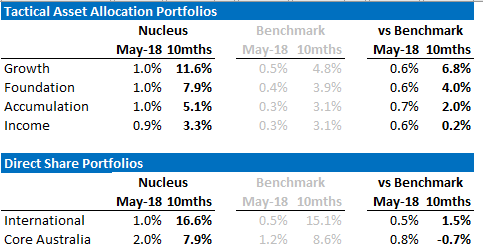

David Llewellyn-Smith is the chief strategist at the MB Fund which is over-weight global equities that benefit from a weaker AUD. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

If these themes interest you then contact us below.

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.