DXY was down last night as the EUR bear market rally continued:

But that couldn’t save the AUD which fell on all DM crosses:

Advertisement

As EM FX crashes, now led by Brazil:

Gold is stuck:

Oil caught a bid:

Advertisement

Base metals are deluded. Where EMs go they will follow:

Big miners broke:

Advertisement

EM stocks fell sharply:

EM junk is ready for downside:

Treasuries were bid:

Advertisement

Bunds too:

Italian debt was flogged:

And stocks held on:

Advertisement

It is interesting to note that the EM forex rout is now happening with or without a rising DXY. Markets are moving in anticipation of another Fed hike next week and more EM central bankers are panicking. Turkey jacked up repo rates by 125bps. Brazil intervened in its currency. The central banks of Indonesia and South Africa both complained about the booming US dollar.

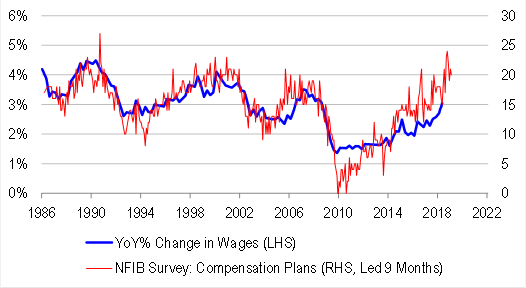

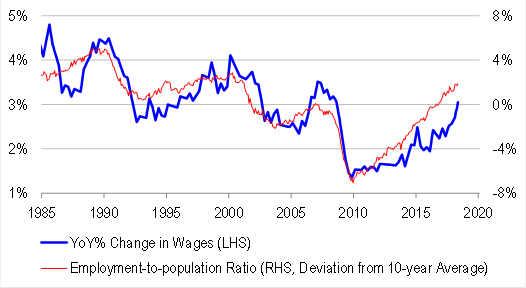

It’s not surprising. The late cycle fiscal stimulus in the US is starting to warm up wages at last. I could show you many charts but a couple from CS tells the tale nicely:

Advertisement

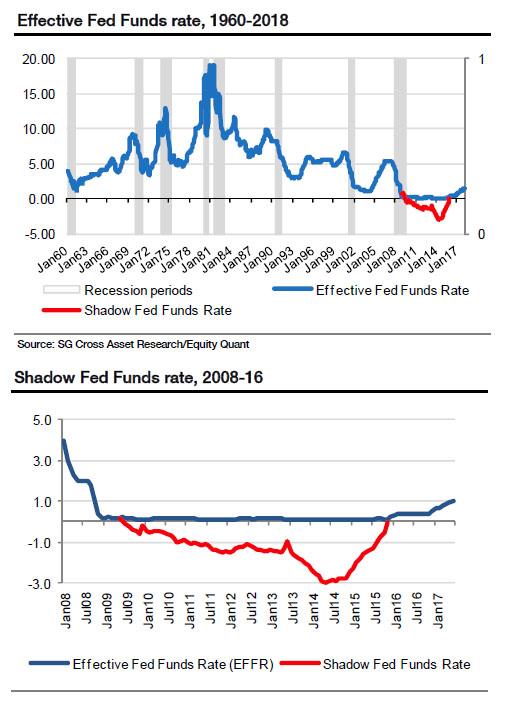

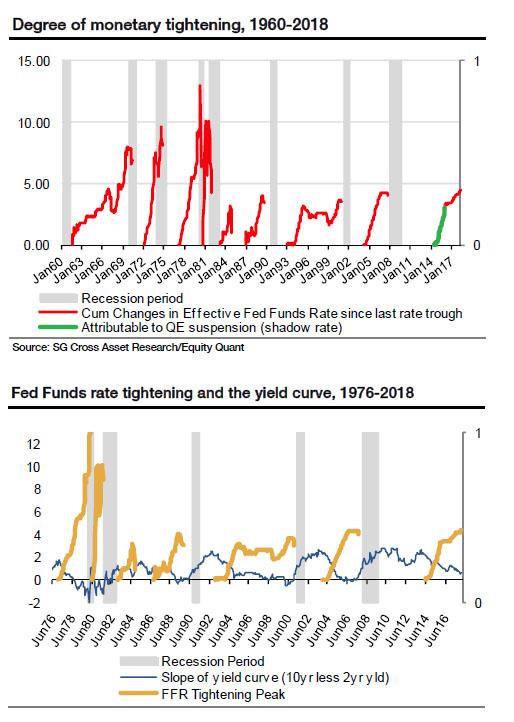

That brings us back to the Fed. Soc Gen is arguing that the tightening to date is much steeper than it appears owing to the quantitative component:

Solomon adopts the methodology for estimating shadow short rates for the US found in the widely circulated Wu and Xia (2016) paper. He shows that the Shadow Fed Funds rate hit negative 3% in mid-2014, but more importantly that a pronounced tightening cycle actually started through 2015, and by the end of that year the Shadow rate had converged back with the effective nominal Fed Funds rate (see charts below).

Solomon notes that although the six Fed Funds rate hikes since Dec 2015 amount to a total of 170 basis points (bp) of tightening, one can argue that if we add the 300bp (Shadow) rate hike to the current Fed Funds rate of 1.70%, the degree of monetary tightening in the current cycle stands at 470bp.

Advertisement

…if that is not enough and the Fed is to be believed, rates are heading to 3.4% (ie another 170bp rise) for a total of 640bp of tightening at a time when the US corporate sector is drowning in a sea of debt. That might be the time for me to revisit Yosemite and Sequoia where the bears should be a lot more visible.

I doubt they will get that far, the Fed has made it plain it wants to run the economy “hot”. But they’ve certainly got more tightening to go. Another two or three hikes this year and more next before it all breaks. US EPS is excellent. It’s debt spreads are fine. The housing market is healthy. The real economy is starting to deliver rising wages. Nor is the yield curve flat enough yet to raise alarm bells. I still expect an inversion somewhere around 3% or above. That’s another four hikes away:

Advertisement

As Europe struggles with Italexit and China slows over H2, the US dollar is still the only game in town. EM contagion is going to get worse and the AUD will get sucked further into it as commodities break down.

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

Advertisement

The recent performance of both is below:

If these themes interest you then contact us below.

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.