JPM runs a neat global bond curve index that is worth a mention:

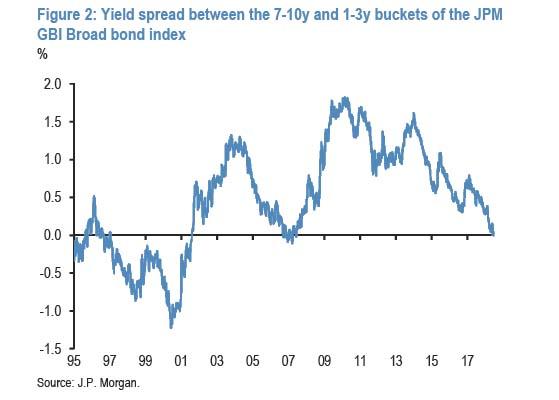

In particular, the yield spread between the 7-10 year minus the 1-3 year maturity buckets of our global government bond index (JPM GBI Broad bond index) shifted to negative territory this week for the first time since 2007. This can be seen in Figure 2.

This is because in terms of the relative stocks of government bonds globally, there are a lot more short-dated US government bonds relative to longer-dated ones as the US has lagged other countries in terms of the duration expansion trend that took place over the past ten years.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.