Recall the UBS take on the Westpac mortgage book via the Royal Commission data dump:

Royal Commission releases APRA’s ‘Targeted Review’ into mortgage books

In recent days the Royal Commission into Bank Misconduct has released hundreds of subpoenaed exhibits including: internal reviews; board papers; and correspondence with regulators. Given the Royal Commission’s focus on Responsible Lending it released numerous reports on this topic, including APRA’s ‘Targeted Review’ of Mortgage Serviceability Assessments on the four Major Banks dated May 2017. Following the reviews, APRA Chairman Wayne Byres found WBC to be a “significant outlier”, with PwC finding 8 of the 10 mortgage ‘control objectives’ were “ineffective”.

Underlying data behind WBC’s mortgage ‘Targeted Review’ released

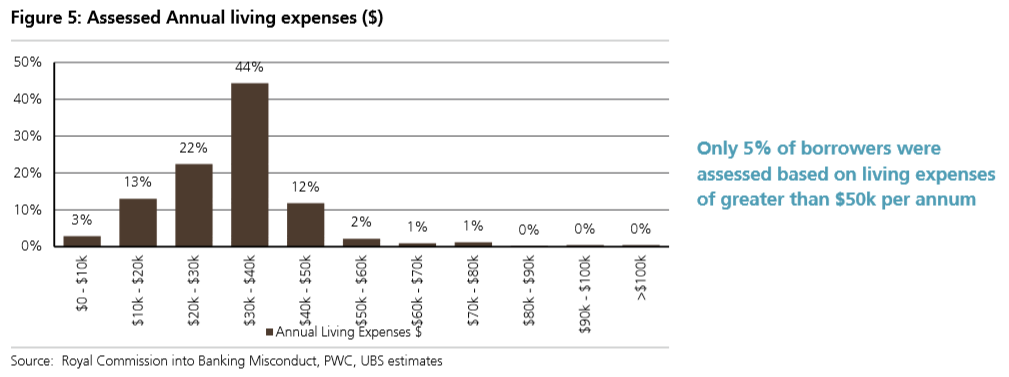

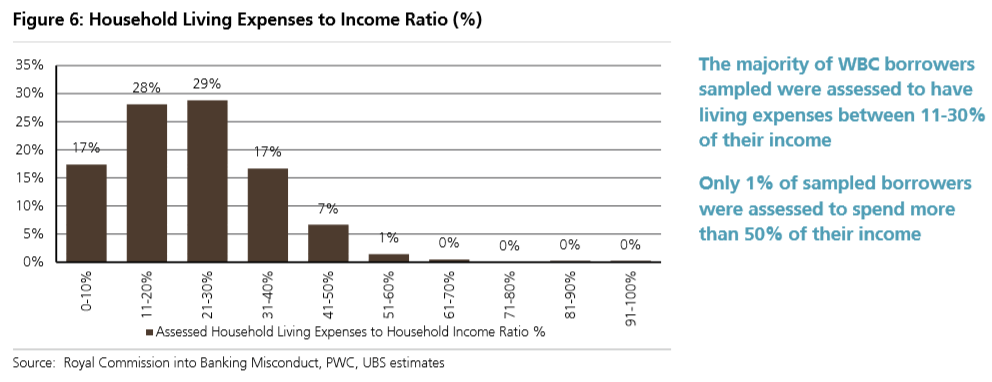

The Royal Commission also released a spreadsheet with the data on the 420 WBC mortgages analysed by PwC (a representative sample). From our analysis of this data we estimate: (1) All minimum income verifications (eg payslip check) were not completed for 29% of the sample; (2) 86% of the sample had assessed living expenses equal to the HEM benchmark; (3) 66% had no itemised living expenses collected; (4) The median assessed household living expenses represented just 23% of household income; (5) In 30% of the sample the borrower’s financial position was suggested to have been misrepresented; (6) In 9% of the sample the loan would not have been approved if the “true financial information” was used in serviceability assessment.

Debt-to-Income much higher than we believed

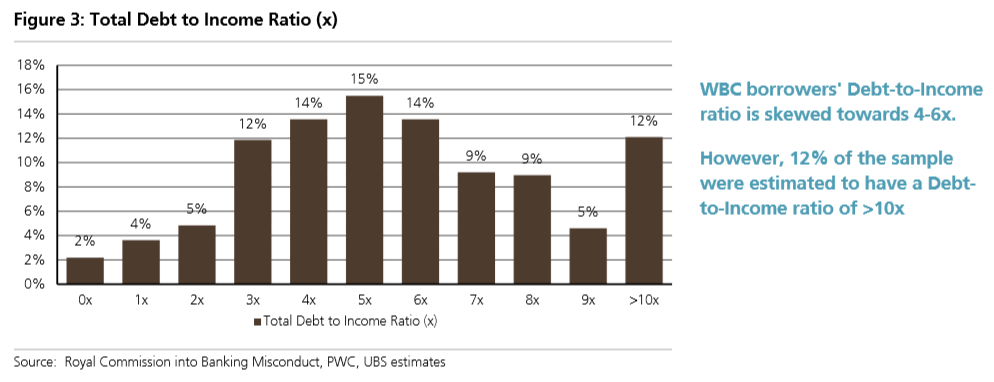

For the first time information on borrower’s Total Debt-to-Income ratios (not Loan-toIncome) has been made available. We found WBC’s median Debt-to-Income at 5.4x, with 35% of the sample having Debt-to-Income ratios of >7x. Further 46% of the mortgage applications had an assessed Net Income Surplus of <$250 per week…

Will WBC need to further tighten underwriting standards following the Royal Commission?

Yes. The release of the APRA ‘Targeted Review’ into residential mortgage serviceability and related Board papers shows WBC is a “significant outlier” with much weaker underwriting than we had believed. This has led to management reporting its concerns over compliance with Responsible Lending laws and potentially the enforceability of the mortgage security to the Board. Since these reports in mid-2017 WBC has started to tighten underwriting standards. However, we believe there may be much further to go before the concerns of the Royal Commission are addressed…

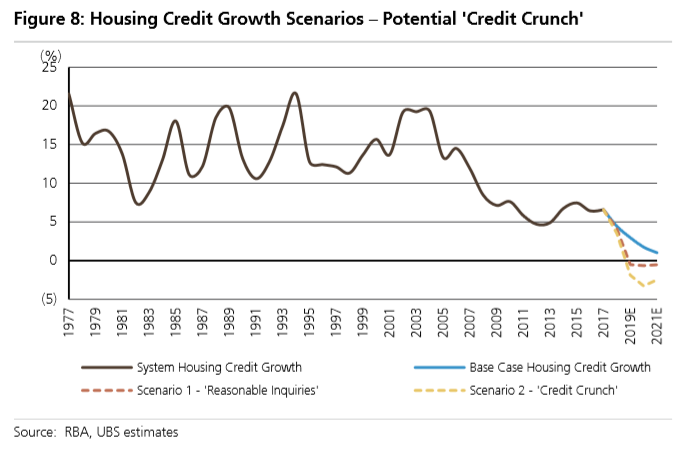

We believe the Royal Commission is a game changer for Australian financial services. In particular its focus on ensuring the banks “obey” the Responsible Lending laws and with Boards and Management likely to be much more risk adverse, further tightening of underwriting standards are highly likely across the industry. This could potentially lead to a sharp reduction in credit availability…

Are these Westpac or Industry wide issues?

We have been concerned with the mortgage underwriting standards of the Australian banks for some time (refer UBS Evidence Lab reports). However, the Royal Commission has been a game changer and is likely to permanently transform the Australian Financial Services landscape. Evidence presented so far has been damning, ranging from fraud and bribery, breaches of Responsible Lending, not reporting misconduct to ASIC and corruption in the financial planning businesses.

The Royal Commission has recently released hundreds of Exhibit documents to its website. We have not had the chance to review all of these documents in detail. However, we have focused on the major banks’ APRA’s ‘Targeted Reviews’ of their mortgage serviceability. These reports have not been flattering with all the banks having material deficiencies. However, WBC’s review appears to have been the weakest, with the APRA Chairman, Wayne Byres describing WBC as a “significant outlier” in its proportion of high Loan-to-Valuation and Interest Only lending.

In addition, Round 1 of the Royal Commission focused on the banks’ Responsible Lending requirements under the National Consumer Credit Protection Act 2009. This states that the banks must make “reasonable inquiries” about the customer’s financial position and take “reasonable steps” to verify the customer’s financial situation. While all of the banks rely heavily on the Household Expenditure Measure (HEM) to assess customer’s living expenses, WBC appears to be the highest user of this benchmark, estimated at ~86% in the sample above.

We believe that overuse of the HEM benchmark is a material concern (and a focus of APRA).

However, this risk was elevated given the Commissioner’s statement:

“An available point of view may be that there is a trade-off between administrative convenience and obeying the law. Now that’s a very awkward trade-off”

WBC has already put in place a number of measures to tighten its mortgage underwriting process following discussions with APRA and its auditor. As of Tuesday 17th April, WBC increased the number of living expense categories to 13 (from 6) and is now requesting new-to-bank borrower’s online banking login and password to assess income and living expenses. However, we believe there is still much further to go until it may fully comply with the Responsible Lending laws. The other banks also appear to be tightening their underwriting standards.

That said, we believe that a number of other factors further increase the risk of a ‘Credit Crunch’. These include:

Bank Boards and management are likely to turn much more risk adverse following the Royal Commission’s allegations;

Mortgage brokers potentially moving from upfront and trail commission to a flat fee-for-service. This could potentially be paid by the customer and would be likely to significantly reduce the demand for mortgage brokers’ services;

The introduction of Comprehensive Credit Reporting (CCR) from July 2018 which will enable the banks to see borrower’s complete debt positions;

Potential changes to negative gearing rules should Labor win the next Federal election in around 12 months;

Interest only mortgagors rolling to Principal and Interest.

In the event of a ‘Credit Crunch’ scenario we believe that WBC’s weaker mortgage underwriting practices than peers will place it in a more adverse situation…

The AFR is convinced that WBC has “demolished” the critique. Last week we had Chris Joye:

Westpac demolished Mott’s allegations on loan quality, revealing that of the 420 loans in the sample file just one borrower (0.2 per cent of the total) was three months or more in arrears, which is “well below [Westpac’s] portfolio average for delinquencies”.

…PwC found that 38 of the 420 loans failed APRA’s loan assessment standards and should not, on this test, have been originated. On Thursday Westpac disclosed that PwC used a limited data file on each borrower, and once Westpac applied its full data file 37 of the 38 loans were, in fact, appropriately approved. And the one loan that should not have passed its credit scoring system is “currently ahead on its repayments”.

Finally, Westpac highlighted that 90 of the 420 loans have already been fully repaid, which combined with its other evidence suggests that the bank’s loan portfolio remains of a high quality. Westpac’s chief financial officer Peter King hammered this point home, noting that “our mortgage delinquencies and losses remain low both relative to historical and industry standards”. That’s important because Westpac has aggressively raised its interest-only loan rates, which should have propagated higher defaults.

Advertisement

That’s a pretty ordinary “demolition”. There is nothing in the WBC response that contradicts UBS. Dodgy loans can fly through without a problem until either there are so many of them that they destabilise the system or some exogenous shock exposes them.

Which is precisely the problem with WBC’s own defense launched yesterday at the RC and today celebrated at the AFR:

Westpac has hit out at the banking royal commission’s release of documents suggesting its lending controls were ineffective, saying a report by PwC had been taken out of context and confused the market, the bank’s chief financial officer Peter King said.

Mr King said PwC’s report in Westpac’s mortgage lending, which was based on a sample of 420 loans, had only used information on customers’ credit files. “This is very important because they did not look at all the information that was available to the banker when they made the decisions,” he said.

“The dataset was incomplete – so conclusions from it will likely be incorrect.”

Advertisement

Looking backwards at credit quality does not tell us anything except that the boom has not unwound yet. Ponzi-borrowers that get out in time make a killing.

If WBC had no issue with its lending standards why did it apply an entirely new and granular expenses screening regime just weeks ago. Moreover, from Banking Day, if WBC’s mortgages were so pristine, why has its issuance collapsed -45% since standards were tightened?

The vitals of the CBA and Westpac and all other profit engines are surmounted in doubt.

Credit growth, the perennial headwind in banker speak: it’s flatlining, falling fast from its recent level of six per cent, at least in the case of mortgage funding. Westpac is one major bank speeding up this fall.

“Australian mortgages performing well” was the stale headline on one important slide yesterday.

Over the first half of 2018 Westpac said it originated $5 billion in mortgages. So call that $10 billion over a year, or the same as the bank funded as far back as 2014.

In 2017 the bank funded $18 billion in mortgages and it was $17 billion the year before that.

As for the economy, the bank could only talk up the global story with the local outlook so challenging.

Advertisement

The only demolition going on here is to AFR credibility.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.