From Bill Evans at Westpac:

As we contemplate the remainder of 2018 and 2019 there are a number of key themes that we believe will dominate economic and market developments. Our advice to customers throughout 2017 has been to expect Australia’s growth rate to likely be anchored below trend in both 2018 (2.7%) and slowing to 2.5% in 2019. That has contrasted with official forecasts (Reserve Bank and Treasury) which anticipate growth picking up to 3.25% in both 2018 and 2019.

We have recognised a solid ongoing boost to growth from non–residential construction; government investment (especially at the state level) and exports. However we are much more cautious than official forecasts on the consumer; residential construction and equipment investment.

Slowing household incomes

Signals from the December quarter national accounts are more encouraging for the official view. Household spending has been revised up from an expected 2.1% to 2.9% following the release of the December quarter national accounts. This picture of households has changed from “lacklustre” to “slightly below trend”.

However this was associated with a weak savings rate of 2.7% despite a boost in nominal labour income growth to 4.8% for the year largely due to an extraordinary lift in hours worked of 3.5%. With hours worked increasing so rapidly, labour income growth should have been boosted further but was constrained by wages growth and a drift to lower paid jobs – non-farm compensation per employee remained flat in the December quarter to be up an insipid 1.8% for the year.

Labour productivity fell over the year with GDP per hours worked falling by 1% over the year and unit labour costs growth lifting to 2%. This adverse development in labour productivity is tempering the recent strong demand for labour we experienced in 2017. In the four months to April the annualised employment growth rate has slowed to 1.3%.

There will clearly be a slowdown in the 2017 break neck pace of growth in hours worked over the course of 2018 and into 2019. Weak wages growth and the drift to lower income jobs looks set to continue putting downward pressure on growth in labour incomes. With the savings rate now probably at its lows, another year of below trend consumer spending growth can be expected.

Business investment

New business investment lifted by 5.8% over the past year, a sharp turnaround from a 6.2% decline over 2016. Over the year, infrastructure work fell 1.2%; non-residential building advanced 12.3% and equipment investment spending increased by 8.4%.

Mining equipment investment lifted by 31% over the year, reflecting the final fit out of three major projects. It is more encouraging that non-mining equipment investment lifted by 6.2% over the year following a slowdown in 2016 partly associated with the uncertainty around the 2016 election.

With another Federal Election due by May 2019 and even greater uncertainty associated with that election (conservative government was expected to win the 2016 election whereas the Labour opposition is ahead in the current opinion polls), we may start to see equipment investment run into some headwinds from that political uncertainty from the second half of 2018. A less upbeat outlook for consumer spending in 2018 and 2019 is also likely to discourage equipment investment.

Housing downturn

Dwelling investment contracted in 2017 by 5.8%. Based on the downturn in the trend in high rise approvals and a flat outlook for detached housing, we expect this downturn has further to run with the contraction accelerating into 2019. Oversupply and a marked slowdown in sales to foreigners are weighing on the outlook for residential building. House prices are now falling. On a six month annualised basis, prices are now falling in Sydney (–7.3%); Melbourne (–1.2%); Perth (–0.4%) and Brisbane (–0.1%).

The regulator’s macro prudential policies are restricting interest only loans and tighter guidelines for all new loans are slowing house prices and credit growth. In previous cycles the authorities have relied on raising interest rates to slow the highly cyclical housing market. This time, the same effect has been achieved by the regulator as banks have independently raised loan rates; foreign demand has slowed; and regulations have significantly squeezed the availability of credit. This process will continue for the foreseeable future and the supply of credit is expected to tighten markedly.

On the demand side the attractiveness of investment properties has diminished. Land taxes and lacklustre rental growth have tightened rental yields. Prospects of adverse tax changes in the event of a change of government are also impacting investor confidence. All major banks (with the exception of Westpac) are predicting rate increases out to end 2019. New lending to investors tumbled by 9% in April to be down 26% over the course of the last year.

The current fall in investor loans is comparable to the fall in 2015/2016. That subsequently reversed in the aftermath of the May and August rate cuts – prospects for a repeat of rate cuts seem unlikely.

We expect an extended period of falling house prices (up to 10% over the course of the next two years) with weakness particularly centred on the Sydney and Melbourne markets. This will represent a considerable change in the “atmospherics” around housing wealth and may weigh further on prospects for consumer spending.

While the wealth effect was modest in the period of rising house prices it is reasonable that there will be a more marked effect through the downswing.

Inflation below target

Inflation is also likely to remain benign holding a little below the bottom of the Reserve Bank’s 2–3% target band. In this regard we are in broad agreement with the Reserve Bank which is forecasting that underlying inflation will hold at around 2.0% in 2018 and 2019. Note that underlying inflation has held below the 2–3% target band in 2015; 2016 and 2017.

With underlying inflation likely to therefore register five consecutive years at or below the bottom of the target range it is reasonable to argue that Australia is experiencing a structural fall in inflation. Arguably, without the risk of overheating the housing market (as would have been a concern through 2016 and 2017), interest rates would have been even lower in Australia in recognition of this structural fall and the disappointing progress in restoring inflation to the target range.

Interest rate outlook

Throughout 2017 and 2018 we have been of the view that the official cash rate will remain on hold in both 2018 and 2019. With 3 Past performance is not a reliable indicator of future performance. The forecasts given above are predictive in character. Whilst every effort has been taken to ensure that the assumptions on which the forecasts are based are reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The results ultimately achieved may differ substantially from these forecasts. Westpac weekly rates on hold in Australia and the US Federal Reserve continuing to raise rates, Australia’s cash rate has now fallen below the Federal funds rate. By end 2018, it is set to be 63 basis points below the Federal Funds Rate, and by end 2019, 112 basis points below the Federal Funds Rate.

Sustained period of negative Aus–US rate spreads

The US economy is operating with much less ‘slack’ in its labour market (unemployment rate of 3.9% compared to an estimated full employment rate of 4.5%) than Australia (unemployment rate of 5.6% compared to a full employment rate of 5.0%) but, to date, wage pressures have only recently emerged (six month annualised pace for the wages component of the ECI has lifted to 2.9%)

Of most concern to markets has been the planned lift in government spending ($300 billion over 18 months) and the Tax Cuts ($1.5 trillion over 10 years) in the US. These policies are likely to boost the Budget deficit by around 2% of GDP providing a solid boost to demand when the economy is already operating at full capacity in the labour market.

We expect two 25 basis point hikes in June and September from the FED. That would see the USD/AUD yield differential in the overnight market contract to minus 63 basis points – a situation we have not seen since early 2000. Two further FED hikes are expected in the first half of 2019.

AUD/USD Bond Spread

Back in August 2017, Westpac had been forecasting that AUD cash rates would fall below the US Federal Funds Rate by around 40 basis points by end 2018. That, in turn, would drive the 10 year bond spread to zero, from around 60 basis points. At that time markets were priced for the US rate to be around 35 basis points below Australia.

But now markets are expecting a yield differential of around minus 75 basis points by year’s end. We now expect RBA rates to be even lower than Federal Funds at minus 63 basis points by end 2018 and minus 112 basis points by mid-2019. The likely result is that AUD 10 year bonds will trade around 40 basis points below US bond rates by mid-2019.

Commodity Prices; China; and the Australian Dollar

Recent general euphoria around the global economic outlook has changed to caution. Uncertainty around trade; falling PMI’s in Europe; Japan and Korea and rising bond rates in the US all signal caution. Growth in the Chinese economy is expected to slow as consumption and net exports are unable to compensate for the ongoing slowdown in investment. However, the big uncertainties and risks centre around the Chinese financial system.

China realises that it must move away from its growth model based on credit fuelled exports and investment. In particular the role of the financial sector must change from channelling high savings at low cost to strategic sectors, to facilitating China’s economic transformation to a more sustainable model based on services and consumption. But the “old” model has resulted in financial assets growing from 260% of GDP in 2011 to 470% in 2016 (IMF, 2017). The excessive growth (around 30% per annum over the last 10 years) has been in the largely unregulated non– bank sector. President Xi has nominated poverty; pollution and financial leverage as his key “challenges”. The “shadow banking sector” particularly funds property development and speculation; local governments (which explain 80% of infrastructure investment); and commodity speculators. All these users of funds expect excessive returns and can service higher loan payments . The sector is beginning to be squeezed.

We are already seeing some evidence of this squeeze on the non–bank sector. Banks are no longer allowed to guarantee wealth management products; entrusted loans (corporates borrowing to lend to other corporates with banks operating as agents) have been banned; rapid growth in short term interbank funding has been slowed; and general funding for wealth management products is being restricted. Growth in the nonbank sector is severely lagging the pace of 2017.

These forces are likely to weigh on iron ore and coking coal prices. Some lift in supply from Australian producers is also expected to lower prices. These atmospherics for commodity prices along with the widening interest rate differential; and more appetite for the USD in an uncertain world are eventually expected to weigh on the AUD. We target AUD at USD 0.74 by end 2018 and 0.70 by 2019.

Being more bullish on the USD, I see 70 cents this year and further downside next but that’s splitting hairs. The thesis is right.

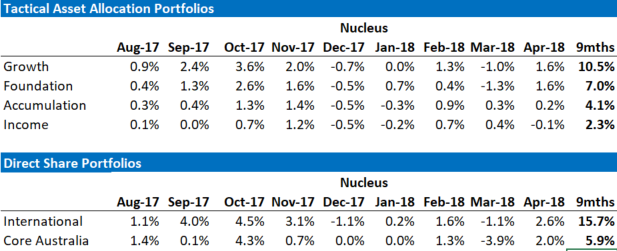

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.