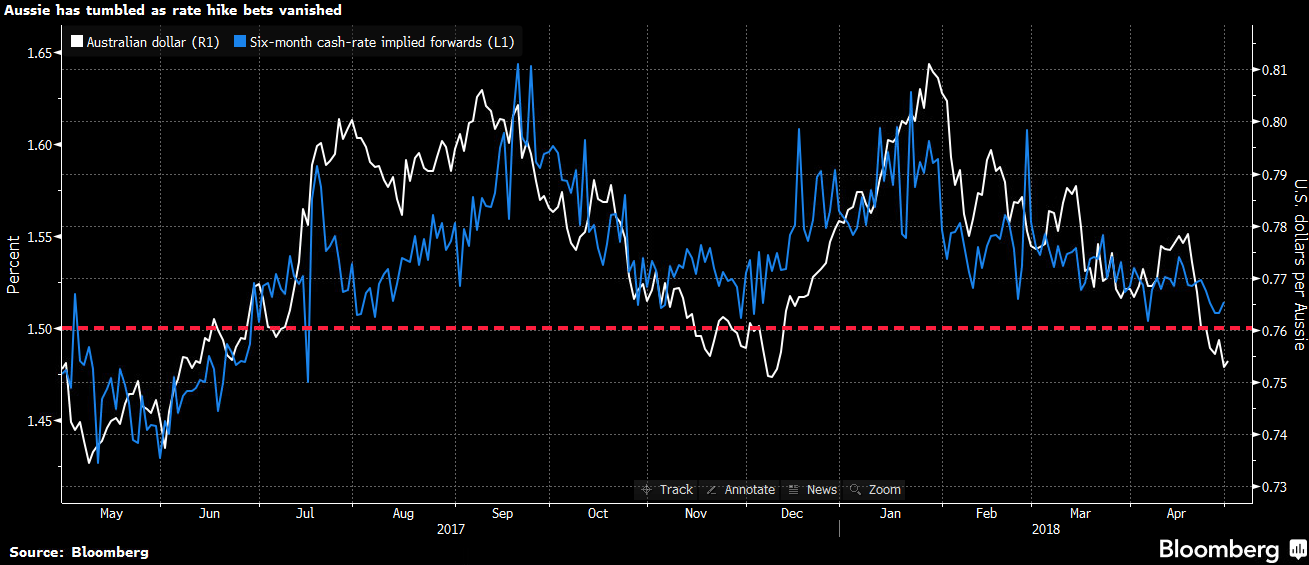

There’s no doubt that the Aussie dollar has fallen away owing to the widening yield spread to the US. In recent terms:

And over the long term:

But the real determinant of the currency over the very long term is the terms of trade, in no small part because its income impacts also determine the cash rate:

The ToT is pretty much set by four commodity prices: iron ore, coking coal, thermal coal and gold:

LNG is not such a factor because oil and gas imports and exports largely offset one another, though the growth of profitless gas exports has lifted the base level of the ToT, sadly.

The ToT rose in the first quarter but has since fallen quite sharply as each of the coals and iron ore have fallen 10-15% each through the end of April with iron ore at $65, coking coal at $176 and thermal coal at $95.

There are two headwinds bearing down on these prices dead ahead. Into the end of the financial year, all three are usually destocked by Chinese firms seeking to rebalance books for tax purposes. I expect that will mean iron ore reaches $50, coking coal $140 and thermal coal $85 by July.

That is a very large ToT shock but it is paced by longer term contracts which use quarterly average pricing so it does not all arrive at once. Moreover, I expect prices will rebound for a while afterwards.

But only for a few months. By the time we reach September, mills again destock commodities as they enter the seasonal slow period across Winter. This year that ought be on made worse as Chinese growth slows which we can see in credit today:

Then I reckon all of the bulks will sink well below even the mid-year prices before rebounding a little into the new year but remaining down heavily year on year. Gold will probably keep falling as well as the Fed tightens and the USD rises.

Those price outcomes will be enough on average to unwind most of the post-2015 term of trade rebound:

Falling term of trade and crushed yield spreads are the very combination that triggered the Australian dollar rout of 2014/15 in which the currency fell -25% in a year.

In the circumstances of a hiking Fed, possible cutting but definitely stalled RBA, and a most assuredly expanding yield spread, the Aussie dollar is going to go off another waterfall:

We have a target of 70 cents for the year-end but it could easily overshoot into 2019.

———————————————–

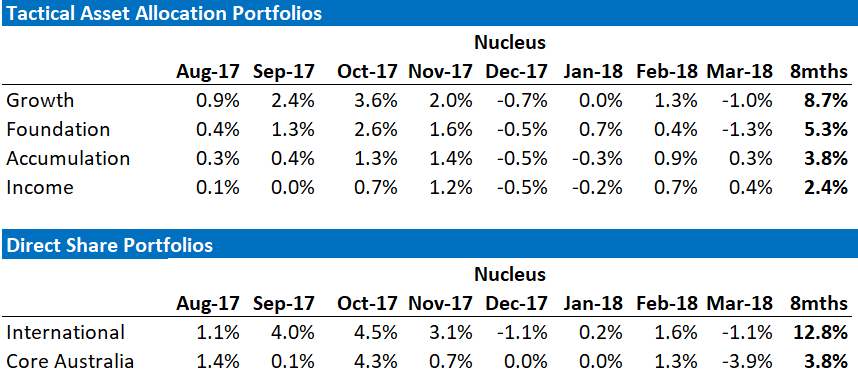

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to get your money offshore so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively to international stocks but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.