Shadow Board No Longer Favours Keeping Interest Rate Steady Ahead of Budget

The last month brought no important economic news. Attention now focuses on the budget; given the consolidation of the Australian economy, an expansionary budget will heighten the need for an interest rate increase. Domestic CPI inflation remains at 1.9%, below the Reserve Bank of Australia’s official target band of 2-3%; unemployment is unchanged at 5.5%. The RBA Shadow Board rules out any likelihood that a reduction in interest rates could be called for. Instead, it attaches a 49% probability that holding interest rates steady at 1.5% is the appropriate setting, while the confidence in a required rate hike increased for the fourth month in a row, to 51%. Thus, the Shadow Board finds that a rate increase of 25 basis points is most likely the best setting, if only by a small margin.

The seasonally adjusted unemployment rate in Australia, according to the latest ABS figures, is unchanged at 5.5% in March but employment has been modest. No new data about wages growth has been released. Stagnant real wages, as Australia has experienced for the past few years, appears to be a global phenomenon and remains a puzzle. Economists and policy makers keep looking for signs that real wages will finally rise and reverse the secular decline in the labour income share.

The Aussie dollar, relative to the US dollar, sold off noticeably in the past few days, without any obvious reason to point to. It now trades around 75.5 US¢. Yields on Australian 10-year government bonds have risen from approximately 2.6% at the end of March to above 2.8%. This increase may well be a reflection of the market taking note of recent comments by the RBA that interest rate increases are probably in the pipeline, even if not in the immediate future. The Australian stock market bounced back from its recent trough; the S&P/ASX 200 stock index currently stands 200 points higher.

Recent releases about the budget (scrapping of the medicare levy hike, income tax cuts) suggest that the fiscal policy may become more expansionary than previously thought. This will likely swell the deficit and increase pressure for the RBA to raise the overnight rate.

Global stock markets have continued to consolidate, apparently shaking off the jitters experienced in January. Volatility indexes are also falling slightly. Mixed signals abound about the global geopolitical risks; on the one hand, the US are sabre rattling with North Korea and Iran, on the other hand, the Koreas have announced peace talks. US trade policy, along with any retaliatory measures by its trading partners, remain a source of uncertainty but this does not appear to have immediately affected global trade.

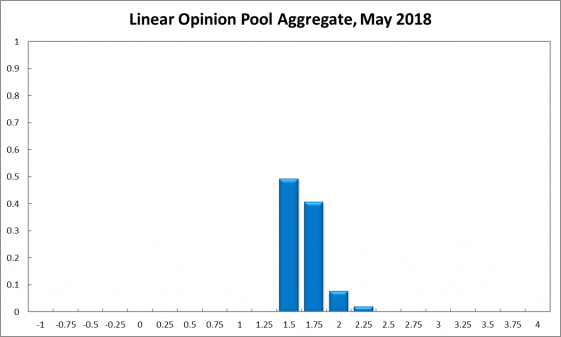

Since the last round in April 2018, the distribution of the Shadow Board’s policy preferences has again strengthened slightly in favour of an interest rate increase. The Shadow Board is 49% confident that keeping interest rates on hold is the appropriate policy, 3% lower than one month ago. It attaches zero probability that a rate cut is appropriate (unchanged) and a 51% probability (48% in April) that a rate rise, to 1.75% or higher, is appropriate.

The probabilities at longer horizons are as follows: 6 months out, the estimated probabilities are unchanged. The probability that the cash rate should remain at 1.50% equals 21%, the estimated need for an interest rate decrease 4%, while the probability attached to a required increase equals 76%. A year out, the Shadow Board members’ confidence that the cash rate should be held steady equals 14% (unchanged from April), while the confidence in a required cash rate decrease equals 3% (4% in April), and in a required cash rate increase 84% (82% in April).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.