The Reserve Bank of New Zealand’s (RBNZ) officially introduced loan-to-value ratio (LVR) restrictions targeting investors on 1 October 2016, although banks began informally applying the rules since they were first announced in mid-July 2016.

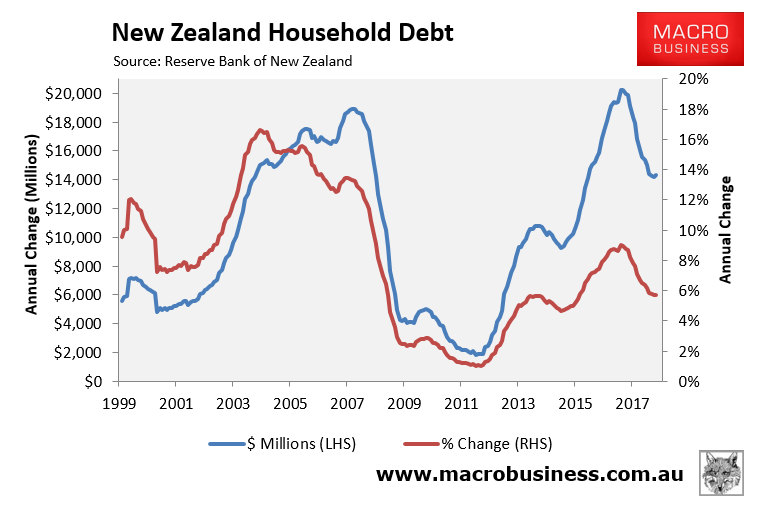

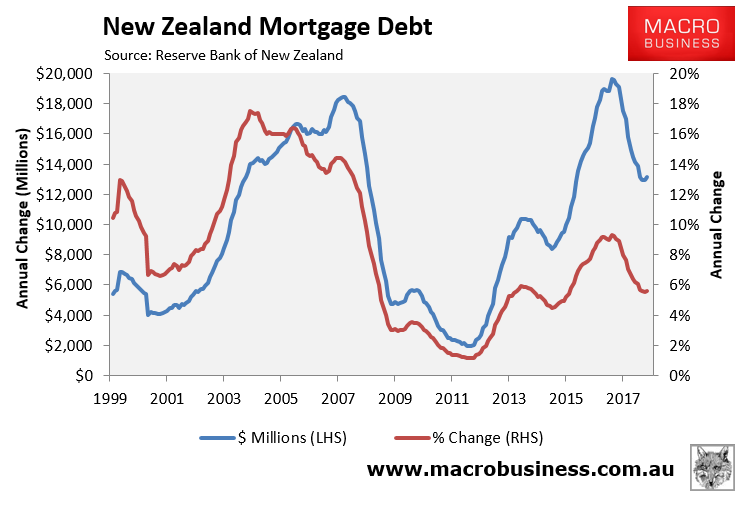

The latest mortgage data shows that household and mortgage credit growth has cooled significantly in New Zealand following LVR restrictions:

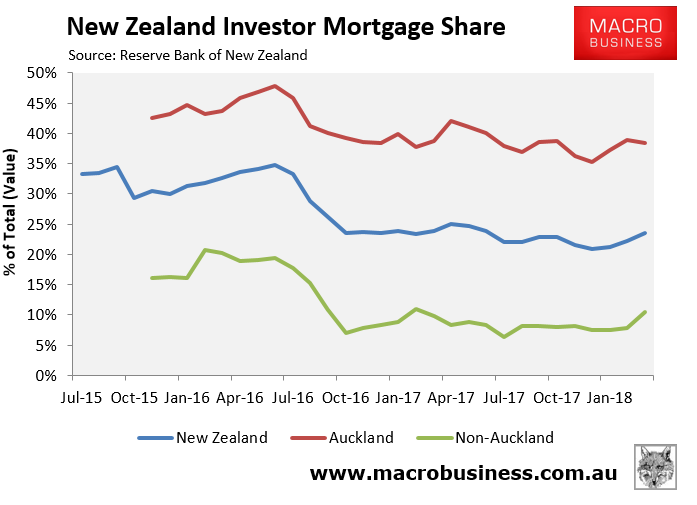

As well as a reduction in the share of mortgages going to investors:

With these facts in mind, it is interesting to report that the RBNZ will persist with its LVR restrictions until lending growth and housing risks reduce further. From Interest.co.nz:

In delivering his first Financial Stability Report, RBNZ Governor Adrian Orr said said both lending and house price growth had slowed in the past 12 months – in part due to the RBNZ’s imposition of loan-to-value (LVR) ratio restrictions.

“This more subdued lending growth needs to be further sustained before we gain sufficient confidence to again ease the LVR restrictions,” he said…

On the subject of LVRs, the RBNZ said that while house price growth has moderated, the level of house prices remains high relative to household incomes.

“Slowing credit growth and house price inflation have eased risks related to household debt in the past 12 months. Reflecting this, the Reserve Bank announced a small easing of the LVR policy in November 2017 to allow a higher proportion of loans to be made at high LVRs.

“The full effect of this easing is still working through, and no further change in policy settings is deemed appropriate for now. The policy will be eased further in the future if housing market risks decline and banks’ lending standards for new mortgage loans are prudent.”

Good job RBNZ.