The minutes of the May monetary policy meeting of the Reserve Bank Board repeated the assertion that first appeared in the April minutes. That is that “members agreed that it was more likely that the next move in the cash rate would be up rather than down”. This observation is contingent on the economy evolving in the way the Bank currently expects which is “a gradual pick-up in inflation as spare capacity in the economy is absorbed and wages growth gradually picks up”. Nevertheless the Board observed that spare capacity in the labour market would remain for some time.

Using this terminology might create challenges for the Bank in future. If the term is ever deleted from the minutes markets are likely to take that as a sign that the Bank’s policy stance has changed.

In a new turn of phrase, the minutes note that while this expected development was unfolding, “it would be appropriate to hold the cash rate steady and for the Reserve Bank to be a source of stability and confidence”.

That implies a badge of honour” to have steady rates rather than a stance that needs to be justified in a world where other central banks are tightening policy.

In these minutes, there is a more detailed discussion on the outlook for housing. In particular, the Board notes that “a further tightening in lending standards in Australia, particularly in the context of the current high level of public scrutiny of Banks, was possible which would affect household borrowing and spending”. The recent release ( since the Board meeting) of housing finance data showing that new lending to investors was now down 26% over the year is certainly consistent with those concerns.

The clear positive development for the economy has been the strong boost to non-mining business investment particularly non- residential construction. The Bank is justified in expecting that this strong momentum will be sustained.

However there remains the concern that wage pressures may take some time to emerge. Indeed the Deputy Governor highlighted the key risk to the Bank’s outlook in his speech this morning. He nominated that risk as being that the level of the unemployment rate needed to spark wage and inflation pressures might be lower than the Bank’s current unemployment forecast which is for about a ¼ per cent fall by June 2019. The Board discusses this prospect when it talks about the wage price index not picking up as quickly as in the past when business surveys identified some shortage of suitable labour. The Board discussion moved to international evidence which shows similar inertia in wages and they discussed possible reasons including competitive pressures from globalisation and technological change.

The Board is sticking with its above-trend growth outlook which they believe will be sufficient to reduce spare capacity in the economy and restore the move to a lower unemployment rate.

There may be some source of embarrassment in these minutes in that it is noted that “recent data on retail” suggested that momentum had continued in early 2018. Since the Board meeting, the retail sales report showed that real retail sales had grown by a very modest 0.2% in the March quarter.

There is a sign that confidence in the global economy has waned a little. The Bank’s forecast now indicates that global growth is expected to ease, albeit still above-trend, over the next couple of years. Rising bond rates, particularly in the US, might take some momentum out of the world economy.

The Bank continues to be quite relaxed about the Australian Dollar noting that “it had remained in a narrow range over the previous two years relative to the US dollar and in trade weighted terms”.

Conclusion

If anything, these minutes seem to imply even greater patience with the current policy of steady rates. In describing the current policy as “a source of stability and confidence”, the Bank is clearly contrasting its policy with the Federal Reserve’s ongoing tightening cycle, but feels no embarrassment with its stance. The issues remain the same, associated with developments in the labour market, inflation and wages. In that regard however, the evolution of consumption in the context of a very low savings rate and the impact of tightening financial conditions on the housing market and house prices will be critical.

Westpac continues to expect that the Bank’s policy of “stability and confidence” (rates on hold) will be maintained throughout 2018 and 2019.

Damien Boey at Credit Suisse is less polite about it:

The “one thing” according to RBA Deputy Governor Debelle

RBA Governor Debelle delivered a typically hawkish speech this morning. He reiterated the RBA’s bullish growth forecasts, and dismissed focus on modal forecasts as an exercise in “false precision”. But it was interesting to note that the key risk he identified to the RBA’s growth outlook from the very outset were movements in interbank funding costs. He also suggested that there could be more tightening of property lending standards to come in the wake of the Bank Royal Commission.

Debelle remains optimistic in the circumstances, pointing to recent narrowing of interbank credit spreads, and expressing his view that credit tightening would adversely impact house prices more than consumption. But we note that:

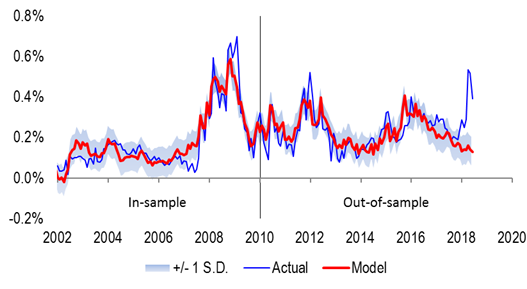

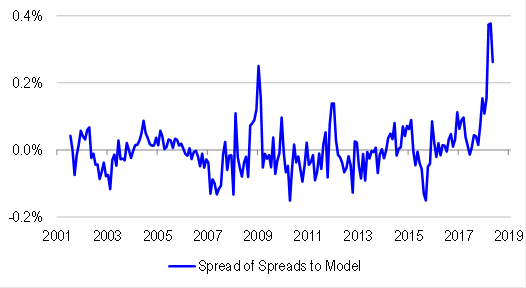

1. Although interbank credit spreads have come off their highs, they are still elevated by historical standards, and consistent with a sharp slowing in loan growth. Indeed, the unexplained portion of interbank spreads (relative to our model based on credit default swap spreads, stock market volatility, the slope of the yield curve and housing sentiment) remains higher than it was during the 2008 crisis.

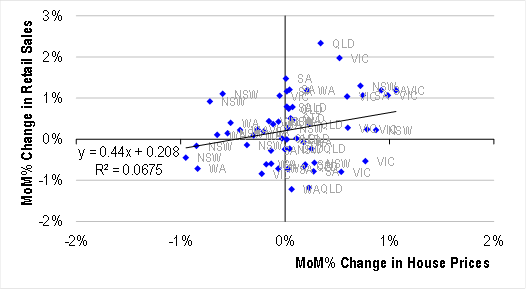

2. Recent data show very clearly that there is a strong linkage between falling house prices and soft retail sales outcomes. The states with the fastest (slowest) house price inflation are also the ones tending to experience the fastest (slowest) retail sales growth.

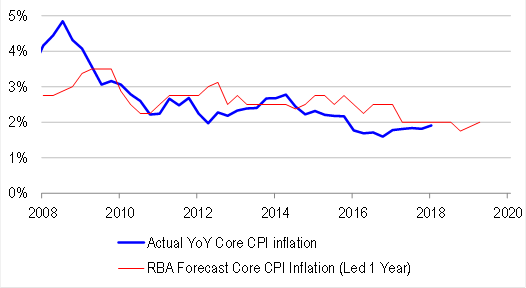

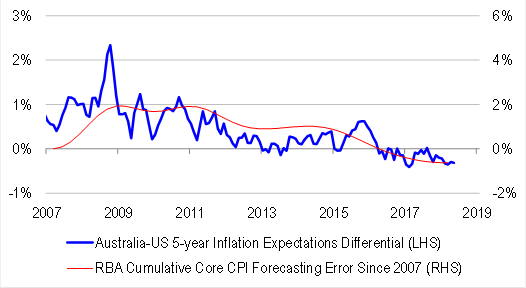

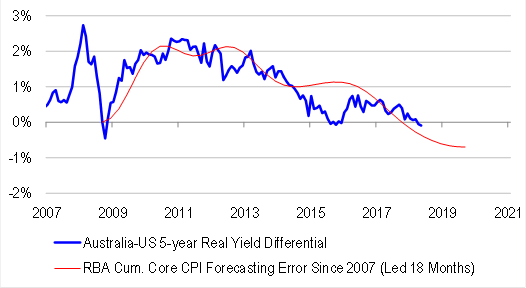

Also, we disagree with Debelle’s view about the insignificance of the RBA’s modal forecasts, and forecast errors. Our backtesting clearly shows that the bond market pays attention to deviation of CPI from the Bank’s forecast trajectory, because Australian-US yield differentials can be predicted using cumulative CPI misses. In other words, investors price Australian inflation as the sum of US inflation and its own forecast credibility gap.

Dovish closing statements in the RBA minutes

Following on from Debelle’s hawkish comments, the RBA published some rather dovish paragraphs in its early May meeting minutes. Specifically, we note more open-ended comments about risks, with the discussion of risk factors seemingly linked to official’s need to re-assure themselves that the next move in rates is up, rather than down. We also note the curious comment that holding rates steady would have positive signalling effects.

“Members noted that there were risks to the forecasts in both directions. Among these, an appreciation of the Australian dollar would be expected to result in a slower pick-up in economic activity and inflation than otherwise. Members also noted that a further tightening in lending standards in Australia, particularly in the context of the current high level of public scrutiny of banks, was possible, which would affect household borrowing and spending. In the other direction, it was possible that global inflation could turn out to be higher than expected. Domestically, there were uncertainties around the extent and speed of the pick-up in wages growth and inflation that might occur as the unemployment rate declined.

In the current circumstances, members agreed that it was more likely that the next move in the cash rate would be up, rather than down. As progress in lowering unemployment and having inflation return to the midpoint of the target range was expected to be gradual, members also agreed that there was not a strong case for a near-term adjustment in monetary policy. Rather, members assessed that while this progress was unfolding, it would be appropriate to hold the cash rate steady and for the Reserve Bank to be a source of stability and confidence.”

Cornered

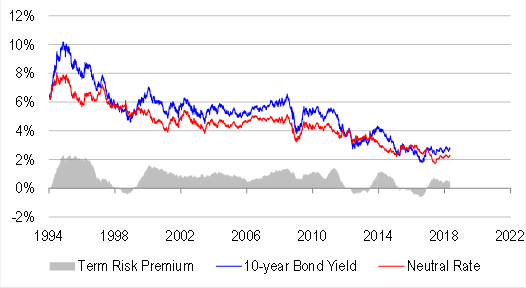

The market is challenging the RBA’s credibility to the point that officials are now having to disclose their own uncertainties. This is not surprising. We are well past the point where higher rates are a sign of good growth, because the term risk premium in Australian bonds (the spread between bond yields and what investors actually think rates will average over the forecast horizon) is materially positive – not negative. When the term premium is negative, there is scope for rates to rise, and central bankers to claim that easing is still being delivered, supporting the “feel good” narrative. This is because there is still a long-term capital subsidy being delivered by negative risk premia, and the marginal benefit to savers from rate hikes overshadows the marginal tightening for borrowers. But when the premium is positive, and normal, we experience a regime shift, where higher rates really are tightening. In the current context, the premium is positive, and market rates have risen. At the same time, tightening of lending standards is occurring, lowering our assessment of where neutral rates actually are.

We expect to see more negative data surprises as incremental tightening manifests. And this time, we think that bank officials are sensitive to downside surprises.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.