Trade deals are front and centre of worries on Asian markets today on the back of the Fed’s release of its latest minutes, which seem to be pushing out the June rate rise. Treasuries remain poised at the 3% yield level while the USD remains strong, stocks are mixed going into the European session.

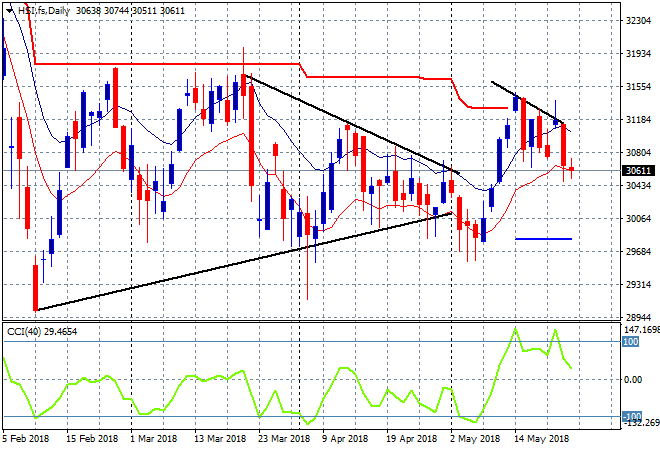

The Shanghai Composite continued its slump after failing to make good on its recent breakout above strong overhead resistance at 3200 , falling nearly 0.5% to close at 3154 points. The Hang Seng Index had a better session, lifting a few points to close at 30710. This keeps the wolves at bay with price right on the low moving average on the daily chart at 30600 as key support that must hold:

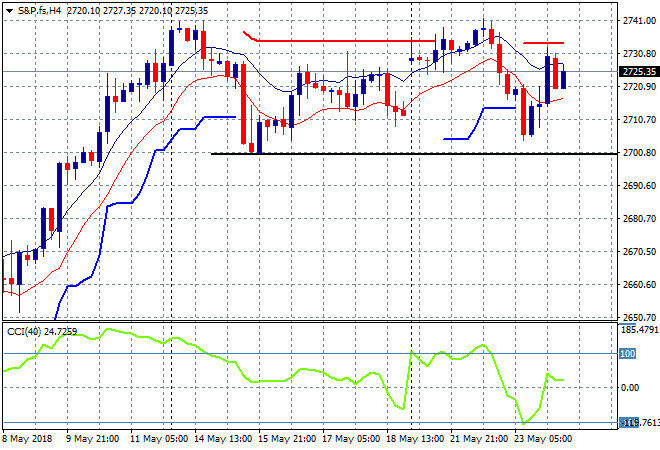

S&P futures are up slightly as are EuroStoxx futures but its nothing to write home about as last week’s continuation pattern unfolds into what looks like another lost week here:

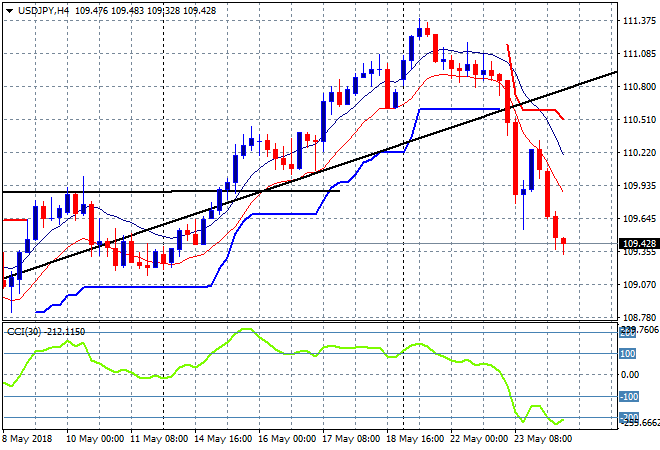

The rising Yen caused selloff in Japanese stocks with the Nikkei 225 falling back 1.1% to closed at 22437 points, right on trailing ATR support and ready to capitulate. The USDJPY pair has broken down further after last night’s rout on the safe haven bid to be above the 109 handle and erasing the last two weeks of buying support in USD:

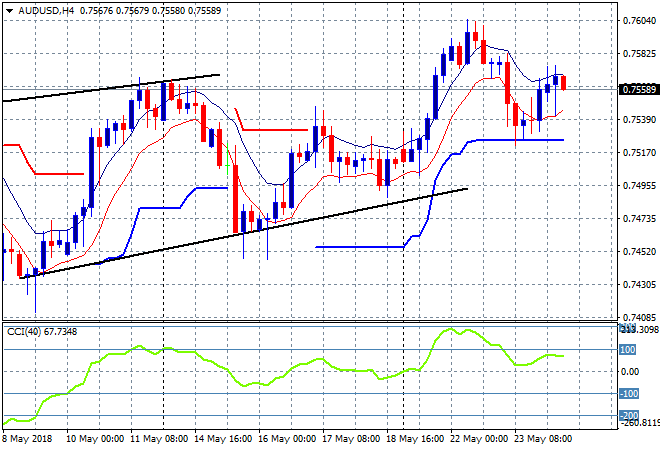

The ASX200 didn’t have a stinker for the second day in a row now, actually putting on a few points to close about 0.1% higher at 6037 with key support at 6000 holding for now. The Aussie dollar has bounced off trailing ATR support on the four hourly chart, getting up to the mid 75s versus USD, but not up to its highs earlier in the week, so I’m watching for a follow through here tonight:

The economic calendar is again UK centric tonight, with BOE Governor making a closely watched speech, followed by the release of the ECB financial stability review. In the US its the next round of initial jobless claims plus some housing data.