Yet another quiet day here in Asia with Japanese stocks reopening, the rest of the region was taking a break that will extend overnight to Europe as well. The USD maintained its strength against the majors, but this did not drag commodities down with oil remaining strong as WTI closes in on $69USD per barrel.

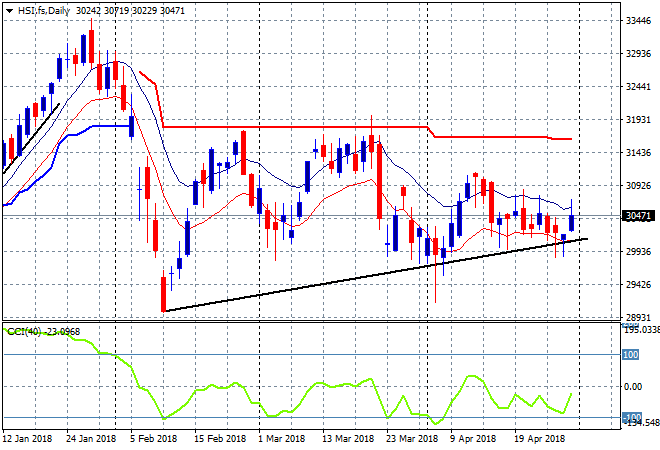

The Shanghai Composite was closed again today alongside most other stock markets including the Hang Seng Index. The daily chart bears watching again and shows a sideways move with a bearish bias as the series of lower highs is starting to intersect with the higher lows from the February correction. I’m watching 31000 on the upside for a breakout:

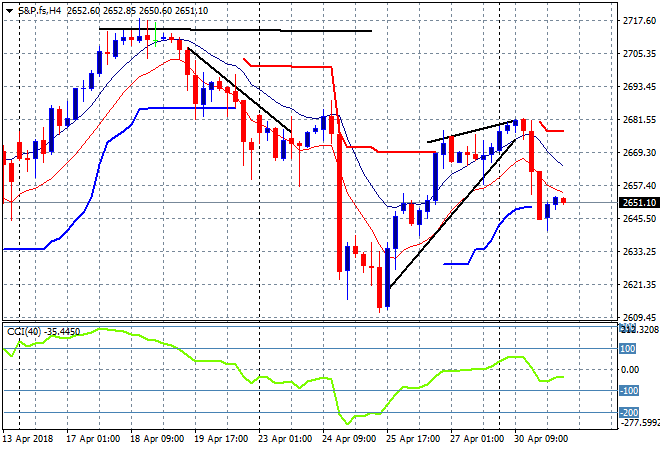

S&P futures are up only slightly and traders will be cautious given the lack of a genuine lead and coming into tomorrows FOMC meeting. The bearish rising wedge worked on the four hour chart splendidly, taking the markets back down to 2650 points but not to a new weekly low:

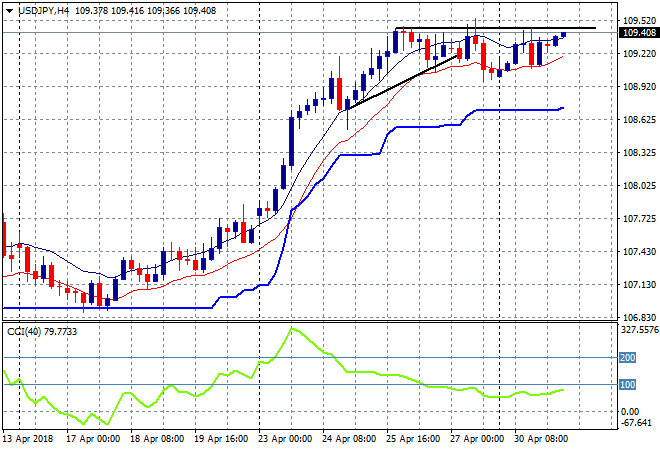

Japanese stocks reopened today, but it was basically a scratch session with the Nikkei 225 barely moving, finishing 0.18% higher at 22508 points. This takes it a new high but daily price action suggests a lot of selling above 22500 or so. The USDJPY pair also barely lifted, not yet making the mid 109s and ready to breakout above that level, all dependent on the Fed meeting of course:

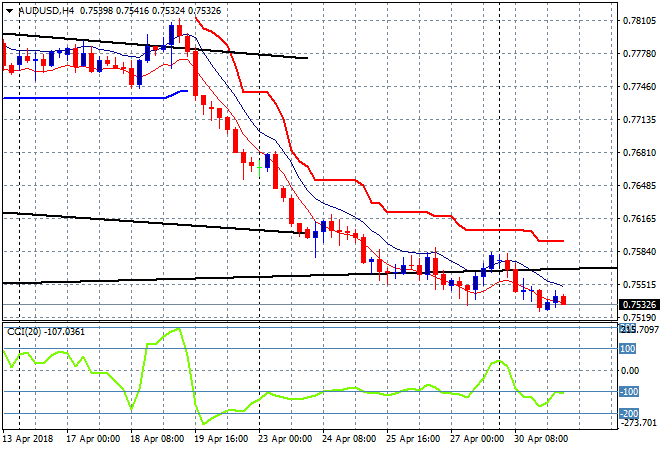

The ASX200 finally got over 6000 points, helped by the banks in the main, lifting 0.5% to 6015 points. There was some help in the form of a weak Aussie dollar, which is slowly slipping to the 75 handle against USD after the RBA was unmoved today. This is all about the strength of the USD:

The economic calendar continues with Canadian GDP, US ISM manufacturing for April and then NZ unemployment in the morning.