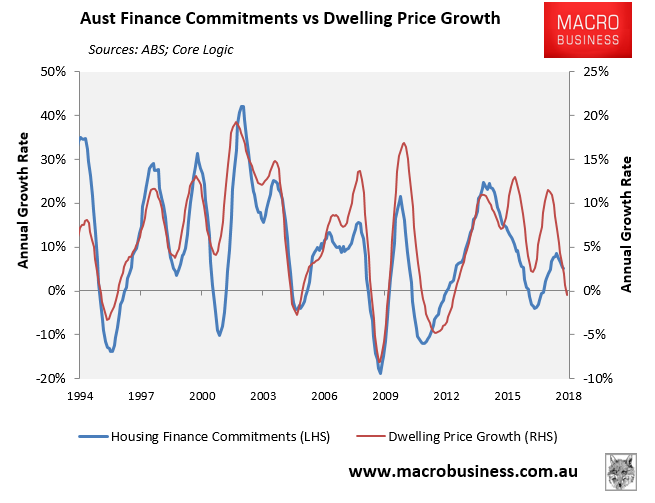

MB has frequently argued that the best immediate predictor of the future direction of Australian house prices is the growth in the value of housing finance commitments (excluding refinancings), since they are the fuel driving the housing market and have displayed a very strong correlation with house prices for decades:

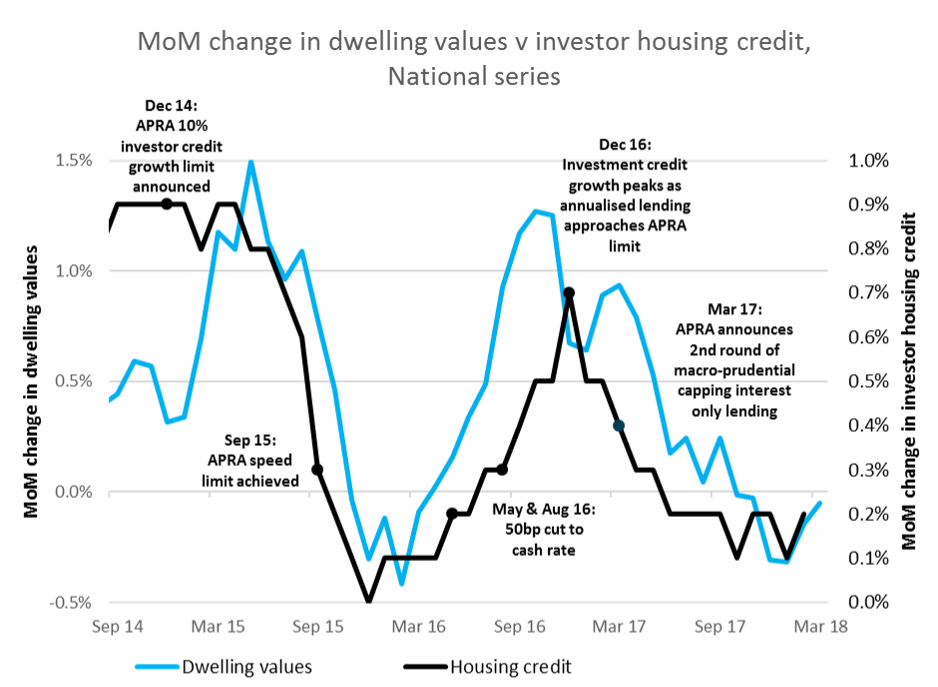

Yesterday, CoreLogic’s Tim Lawless penned an article arguing that since 2015, “the correlation between dwelling value appreciation and housing credit has become tighter; especially when measured against investment credit”.

Lawless then produced the below chart showing the strong correlation between monthly investor credit growth and dwelling value growth, and noted that Sydney’s and Melbourne’s dwelling values, in particular, began to slow precisely after “credit policies were tightened in response to the APRA limits”:

Lawless also noted that “the Royal Commission” means “there is a great deal of focus on lending practices”, therefore, investor credit will likely remain constrained.

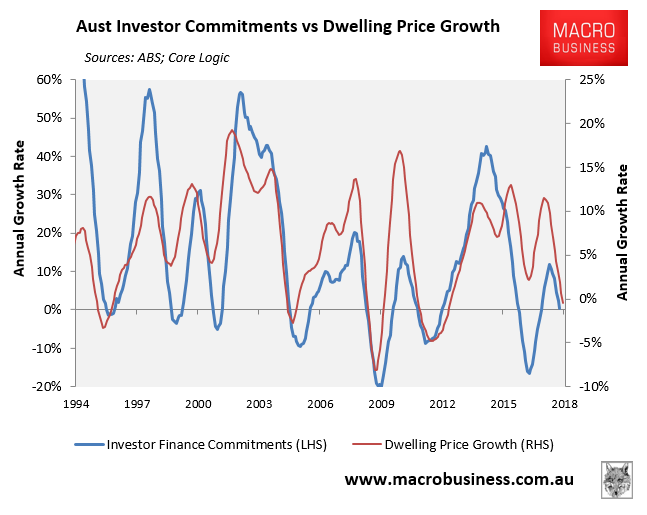

After viewing the above chart, I decided to plot the growth in the value of investor credit against the growth in dwelling values across Australia’s major jurisdictions to ascertain whether values are inextricably linked to the flow of investor credit.

First. below is the national picture dating back to the mid-1990s:

As you can see, the correlation is incredibly strong.

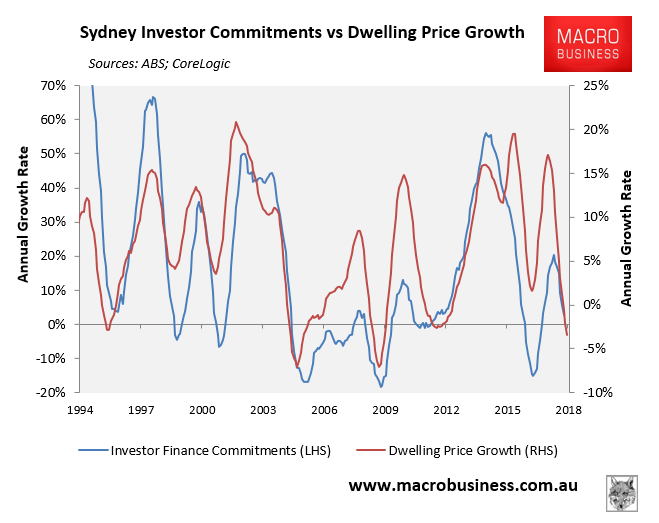

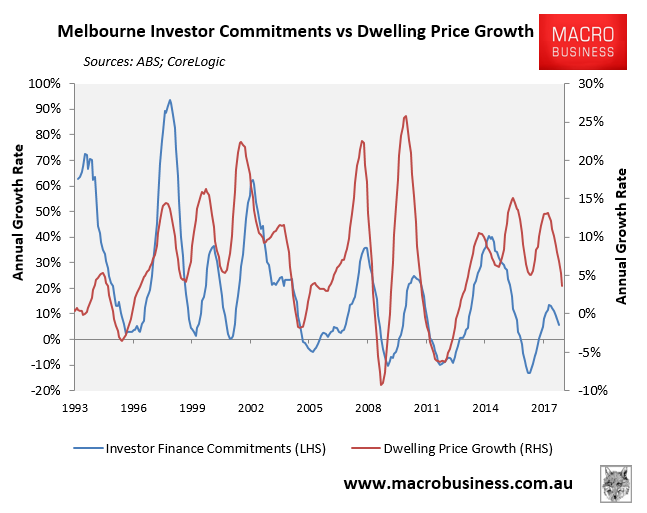

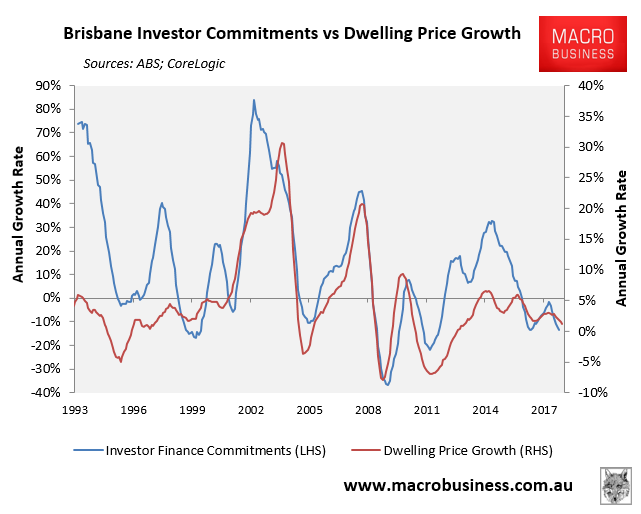

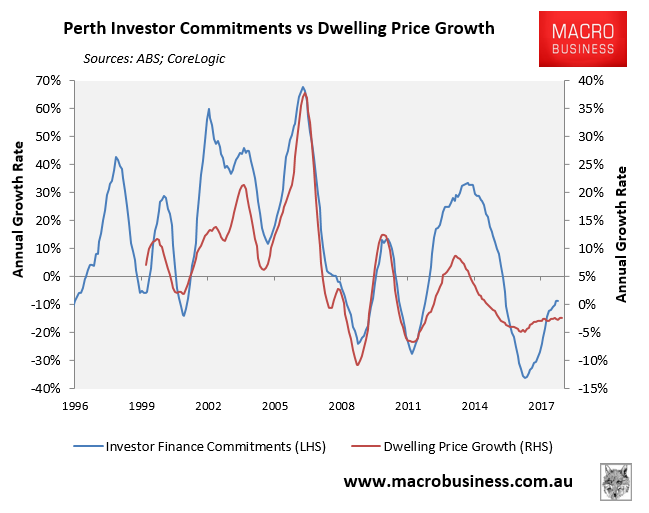

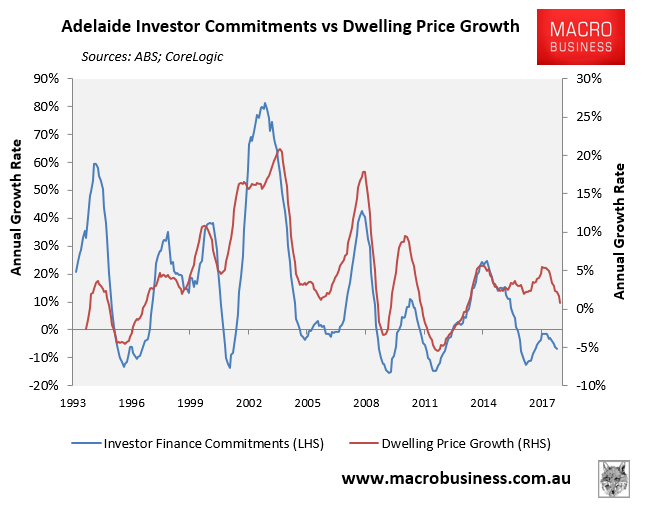

Next, below are the charts for the major capital cities:

Again, the correlations are very strong, particularly in the investor hotspot of Sydney.

What the above charts tell us is that if you want to get a good gauge into the future direction of housing prices, then watch not only total housing finance commitments, but investor credit specifically. They are the marginal price setters in the market.

We already know that investors are likely to face stiff headwinds in the period ahead due to:

- The massive roll-over of interest-only mortgages into principle and interest (raising repayments by 35% to 50%);

- Tightening lending standards arising from the banking Royal Commission;

- Rising bank funding costs; and

- Labor’s negative gearing and capital gains tax reforms should it win the next election.

These factors combined will continue to weigh on housing values and make investing in property a particularly risky proposition.