1. US 10-year yields to fall by 15bps to 2.78%, and German 10-year yields to fall by 8.4bps to 0.26%. US yields are at their lowest since April this year, while German yields are at their lowest since mid-2017.

2. Italian spreads to bunds to blow out to 290bps – their widest since early 2013.

3. The Italian 2s/10s curve to invert.

Also, equities sold off, with low-beta stocks and small caps outperforming. Quality stocks underperformed slightly, while momentum and value subtracted alpha.

Italians will return to the polls in July to try to resolve the deadlock, with many framing the vote as a “stay or leave” (the monetary union) decision. The would-be coalition’s proposal for a mini-BOT parallel currency is adding to the hype, and investor concerns about euro zone break up.

In this note, we argue that:

1. There is no exit. We are not talking about Italy leaving. Rather, we are talking about the ECB not being able to exit quantitative easing.

2. For as long as sovereign debt risks are front of mind in Europe, US Treasuries are likely to receive a bid as an alternative safehaven. Despite copious amounts of government spending, and a shift in liquidity regime, there still is a shortage of safehaven assets in the world.

Within the equity market, this outlook favours low-beta, and high quality exposures over value and momentum plays.

There is no exit … for the ECB

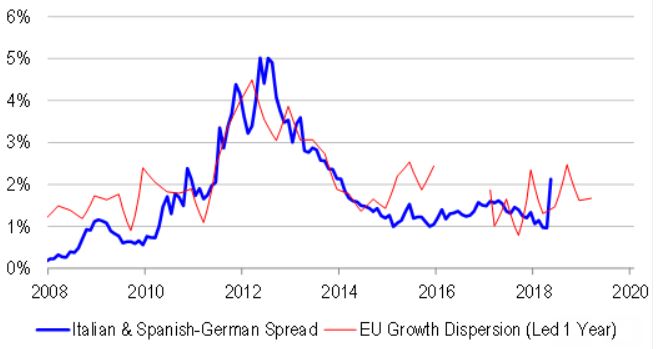

For all the volatility we have seen in peripheral European bond markets over the past week or so, the weighted average peripheral European sovereign spread to bunds is still not at panic levels. Rather, we see the spread merely returning back to more normal levels. One of the most powerful leading indicators of the spread is the dispersion of real GDP growth outcomes in the monetary union. Greater (lesser) dispersion makes it harder (easier) to argue that the “one size fits all” solution that is the monetary union is appropriate for all member states, heightening (lowering) break up risks. At current levels, spreads are merely in line with current levels of growth dispersion. They have risen sharply recently, to be sure, because the ECB is now threatening to withdraw from its quantitative easing program which up until now, had been suppressing risk and volatility. But spreads have by no means overshot fundamentals.

The key issue therefore is the ECB’s threat or promise to exit quantitative easing. In the monetary union, member states do not have the ability to deficit spend on overdraft-like terms with the ECB. Rather, they have to raise funds from the public first before they spend them. In other words, they are revenue constrained. Put differently again, they merely re-distribute cash in the economy, rather than create it.

ECB quantitative easing does not change the revenue constraint. The ECB offers to buy bonds from banks and investors in secondary markets. It does not, and cannot buy primary issuance according to its constitutional mandate. By purchasing bonds, the ECB is not financing member states in their spending. Rather, it is making the act of borrowing from debt markets a risk free exercise. If investors have the option of on selling primary issuance to the ECB in secondary markets, technically government funding risk disappears. Accordingly, peripheral sovereign spreads to bunds tighten.

But now, if the ECB is withdrawing this privilege, member states also lose access to risk free funding. This makes them concerned about running excessively large deficits or debt levels, and forces them back into austerity. The problem is that if growth is slowing sharply, governments lose the option of running larger deficits to stimulate the economy. Indeed, larger deficits would merely “crowd out” private sector spending.

In recent years, there has been no problem with these dynamics. Private sector credit creation has been relatively strong, and accelerating. Loans have been creating more than ample deposits, which could be used to fund public spending. But now that financial conditions have tightened, and growth is slowing, the private sector in troubled nations is looking to pass the baton on to their respective public sectors. And these entities are not well placed to take this baton, especially if the ECB is not actively supporting them. Indeed, wider sovereign spreads make it harder for banks to lend, and the private sector to borrow, exacerbating de-leveraging risks, and undermining confidence.

Over the past year or so, the ECB has been talking about tightening prospects, because private sector credit creation has been strong. But now, the outlook has changed dramatically, and the markets are doing the tightening for the Bank. Once the problem has been diagnosed, we expect that the ECB will change its tune on policy. Even then, it has a problem – it, and other central banks spent so long trying to convince us that higher rates were a sign of good growth. Now, they have to convince us that lower rates are a positive. Yet the very reason why we ended up in this quagmire to begin with was that low and negative rates became a form of tightening because they penalized savers more than they benefited borrowers …

Europe has driven tantrums in the US bond market

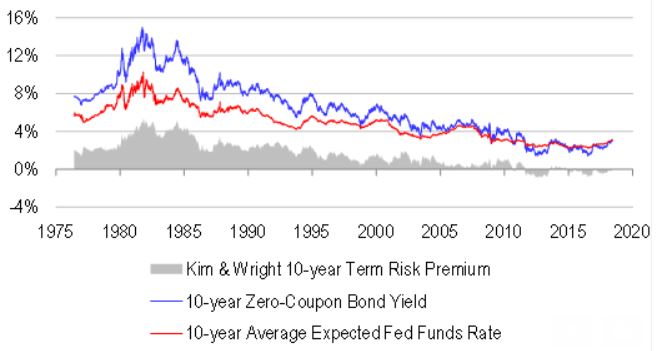

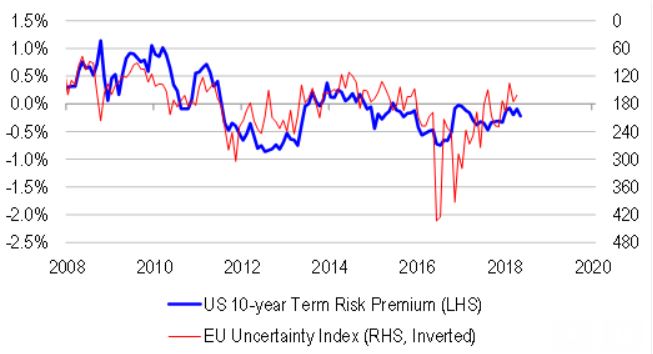

The two most notable US bond market tantrums occurred in 2013, and late 2016. On both occasions, yields had fallen to extremely low levels – indeed, to levels below investor expectations for terminal rates. In other words, term risk premia – the compensation investors receive for taking on duration risk, over and above their mean forecasts for rates, had turned negative.

We find it interesting that episodes of negative term risk premia have coincided with deep uncertainty in Europe. Over the past decade or so, the US 10-year term risk premium has been highly negatively correlated with the European uncertainty index. In 2011-12, the peripheral European debt crisis caused uncertainty to rise, and investors to flee to US Treasuries as an alternative safehaven asset class. In 2016, Brexit had a similar effect on pricing. But on each occasion, once the uncertainty dissipated (eg because of ECB President Draghi’s commitment to do “whatever it takes”), US yields ratcheted higher to be more in line with “fundamentals”, while peripheral European sovereign spreads to bunds tightened.

Another way of looking at negative term risk premia is in terms of liquidity value. Safehaven bonds, such as US Treasuries have a high degree of moneyness (or collateral value) when it comes to repo transactions in the shadow banking system. When the moneyness of other sovereign bonds deteriorates, there is a natural increase in demand for US Treasuries, because the stock of safehaven bonds and good collateral in the system shrinks. More recently, we have seen Basel III elevate the moneyness of reserves in the banking system over US Treasuries, contributing to the unwind of negative term risk premia. But now, the regulatory effect is being swamped by a renewed search for scarce and safe collateral.

Never mind Fed balance sheet reduction, fiscal stimulus, inflation risks or Chinese selling of Treasuries. History tells us that the real explanation for abnormally low bond yields is a shortage of safehaven assets in times of uncertainty. And Europe has been the greatest source of uncertainty over the past decade, because there we see politics meet true funding constraints.

Could Italy leave?

So far, we have merely discussed how to price the risks of euro zone break up. We have not tried to explicitly guess the likelihood of Italy leaving the monetary union. And we will not do so here either. But what we can do is provide some additional context for understanding the incentive structure.

Technically, money has value because the sovereign state has the right to demand payment in the unit of currency that it chooses. In other words, money has value because we need to pay our taxes. With this in mind, everyone in Italy that needs to pay their taxes must hold whatever currency the Italian government chooses to demand tax payment in. Therefore, there is a natural source of demand for mini-BOTs, or neo-Liras.

The complication is that much of Italy’s debt is denominated in EURs, rather than alternative currency. Therefore, Italy technically faces risks from having foreign currency-denominated debt. After all, it cannot print EURs – only alternative currency in a new regime. And should it choose to hit the printing presses, the new currency could devalue sharply relative to the EUR, exacerbating debt problems in the short-term.

When Greece threatened to leave the monetary union, it found itself crippled by:

1. Lack of access to the information technology running the banking system

2. A lack of size. By the time Greece decided to leave, holdings of its debt by core European banks had diminished. The damage it could inflict on the rest of Europe was less than the damage it could inflict upon itself through leaving. Therefore, it was less of a “time bomb” for the rest of Europe, and exit was less of a credible threat.

But Italy is a different story all together. The state has a more credible case for leaving.

Investment implications

De-leveraging risks are high. The ECB is contributing to these risks by threatening to tighten. It is more likely than not to delay, or abandon these plans in light of turmoil in bond markets. But even if it keeps up quantitative easing, there are problems to deal with. Private sector demand in Europe is slowing on the back of tighter financial conditions. And the very case for tightening in the first place was predicated on the evils of low and negative rates …

In this sort of macro-environment, there are no easy fixes. Uncertainty in Europe is likely to remain high, contributing to a safehaven bid for US Treasuries and Australian government bonds.

From a stock selection perspective, this outlook is consistent with low-beta and quality investing. It is inconsistent with naïve value and momentum investing. We seek certainty in uncertain times – not value traps, nor yesterday’s growth stories.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.