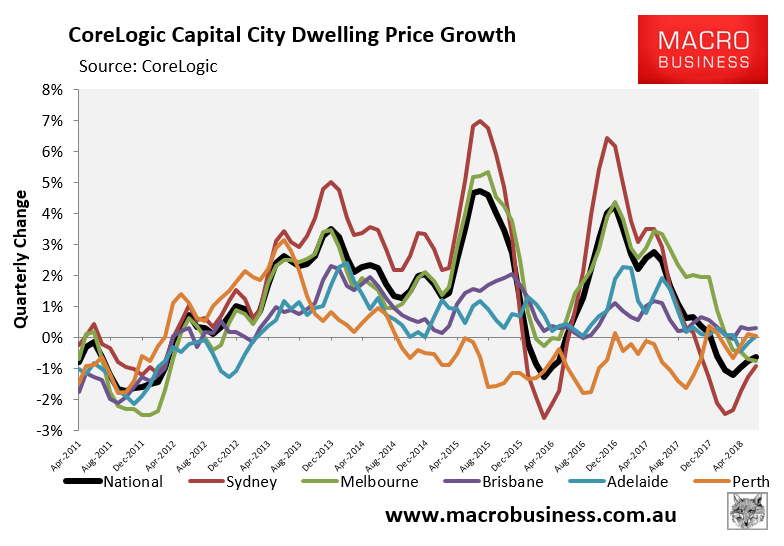

CoreLogic’s Daily home values index shows that quarterly values are falling fastest in Sydney (-0.94%) and Melbourne (-0.77%), which has dragged the five-city index down by 0.65% over the quarter:

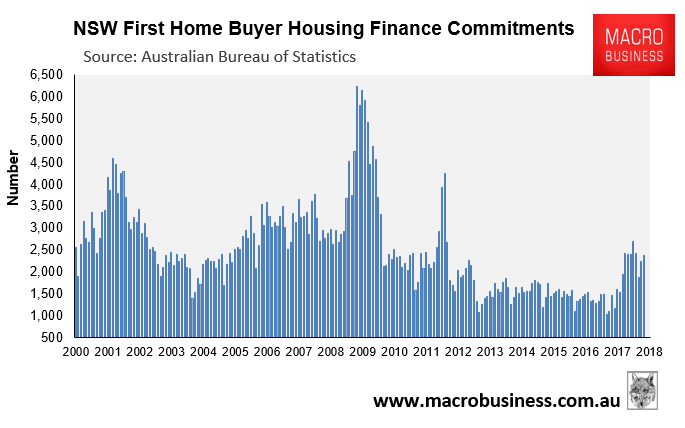

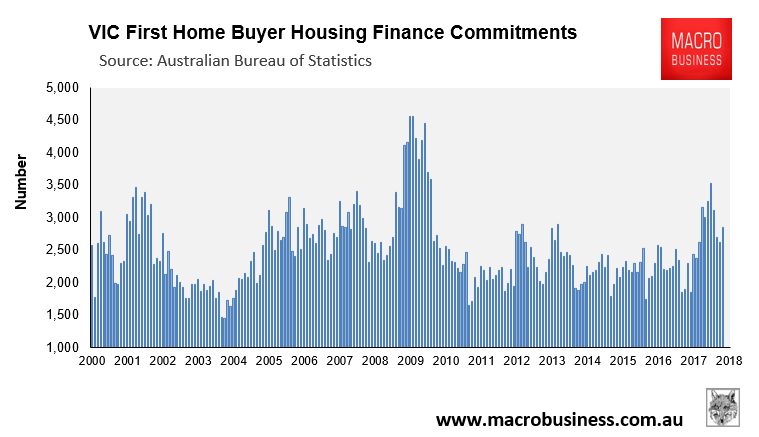

As we have reported previously, first home buyer (FHB) stamp duty incentives were introduced in both NSW and VIC from 1 July 2017, which has driven a 63% and 24% respective lift in the number of FHB housing finance commitments versus the prior year:

Not surprisingly, these FHB bribes have led to much stronger price performance across so-called ‘affordable’ price points – i.e. the bottom 25% of properties by value – in both Sydney and Melbourne.

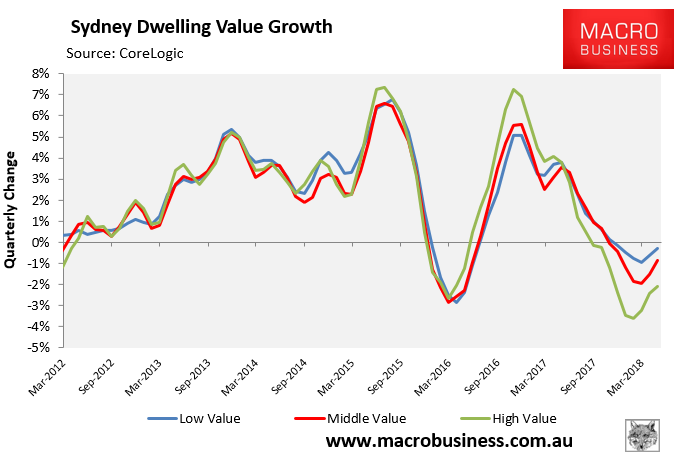

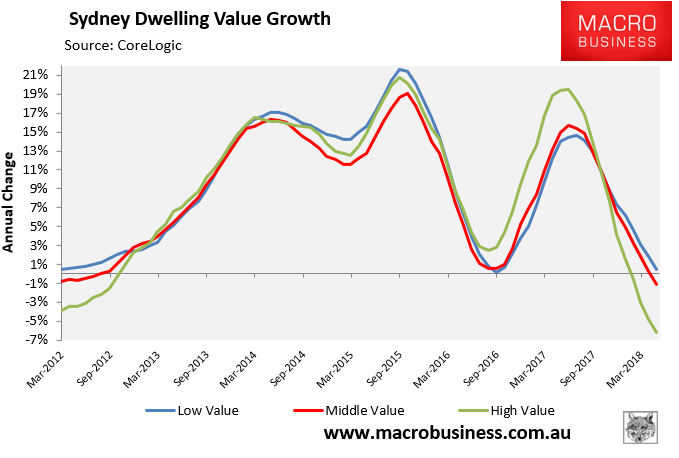

As shown in the next chart, CoreLogic reports that the bottom 25% of dwellings by value in Sydney fell by just 0.3% in the April quarter, versus a 0.9% decline across the middle 50% of properties by value, and a 2.1% decline across the top 25% of properties by value:

Similarly over the year, the bottom 25% of dwellings in Sydney actually rose in value by 0.5% as at April, versus a 1.1% decline across the middle 50% of properties by value, and a 6.2% decline across the top 25% of properties by value:

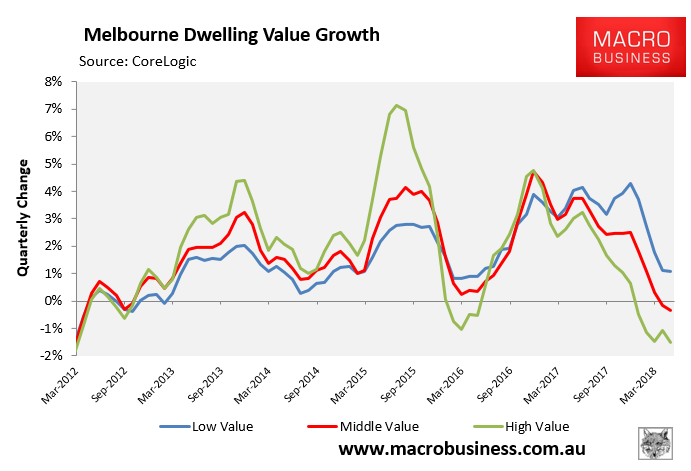

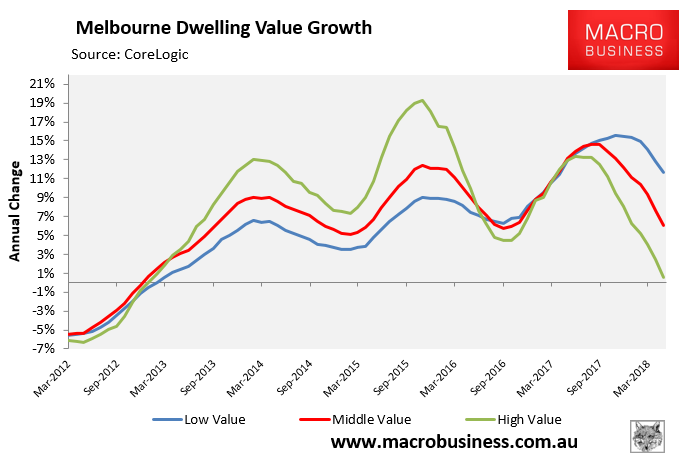

Likewise in Melbourne, CoreLogic reports that the bottom 25% of dwellings in Melbourne actually rose by 1.1% in the April quarter, versus a 0.3% decline across the middle 50% of properties, and a 1.5% decline across the top 25% of properties by value:

Whereas over the year, the bottom 25% of dwellings in Melbourne rose in value by 11.7% as at the April, versus a 6.1% increase across the middle 50% of properties, and a 0.6% rise across the top 25% of properties:

The above charts suggest that dwelling prices would have fallen much further in Sydney and Melbourne if not for the FHB bribes implemented by both state governments.

FHBs are being used as cannon fodder against a property correction.