Overnight, we published a note about the likely economic impact of the FY19 budget (“Budget FY19 – no stimulus here”, dated 8May 2018). In short, we see:

1. Modest fiscal tightening: The underlying deficit is likely to shrink to 0.8% of GDP from 1% of GDP. Levels of and changes in the deficit matter for the economy. But deficit changes matter more arithmetically for economic growth. While the government will continue to expand debt and money supply at a moderate rate, fiscal policy is notionally having a tightening effect on the economy to the tune of 0.2% of GDP.

2. No stimulus for the consumer: In FY19, the scrapping of planned Medicare levy hikes, and tax cuts for low- and middle-income earners is expected to add $760m to households, or 0.1% of annualized disposable income. The stimulus is modest. Indeed, it is not stimulus at all, because the measures really try to avoid negatives from hitting the economy (notably bracket creep).

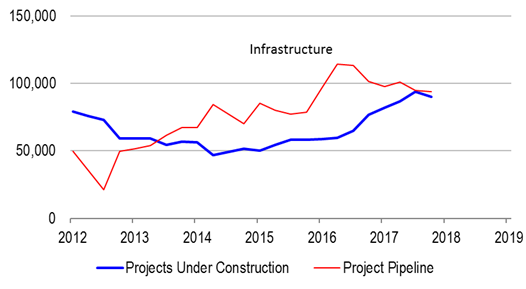

3. No intentional uplift to infrastructure capex: The government has reiterated its commitment to building Australia via its multi-year $75 billion infrastructure plan. However, the details of the spending plan point to planned reductions in annualized capex spend over the forecast horizon – not increases.

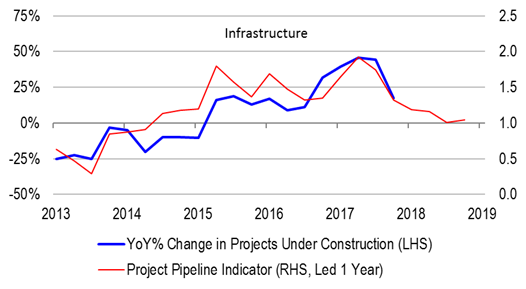

Also note that looking across Federal and state government budgets, the infrastructure capex pipeline is not deep enough to support growth. Access Economics data suggests that the pipeline of projects under consideration is roughly equal to work underway.

AAA: Australia’s austerity alibi

The government plans to return to surplus by FY20 rather than FY21. It appears that the austerity mandate is still very strong, and the government has tried to sell this to the public.

In all likelihood, the government will succeed in preserving its AAA credit rating for now. But why does this matter? Technically speaking, the Australian monetary system is a closed one:

1. The Federal government spends AUDs before it raises them using an overdraft-like facility with the RBA. It does not need to raise AUDs first via taxes or bond issuance, before spending. Indeed, bond issuance is a sterilization operation – not a financing operation.

2. The Federal government has negligible foreign currency-denominated debt.

3. The Banks have taken on board significant offshore wholesale funding – but not to purchase foreign currency denominated assets. Bank loans create deposits. Australian households use AUDs – not foreign currency – to buy houses. When banks go abroad in search of term funding, they are doing so for duration matching purposes – not funding purposes. Essentially, they borrow foreign currency and via an FX swap transaction, use the proceeds to buy back the very deposits they created in the first place. In the event that foreign funding availability dries up, banks would simply revert back to deposit funding.

Given that the Australian system is closed, the AAA rating is largely irrelevant. Indeed, the US experience during the 2012 debt crisis shows that for closed systems, sovereign ratings downgrades tend to push down bond yields, rather than push them up.

To be sure, there is an argument that Australian banks hold significant amounts of AAA-rated government bonds, and that a ratings downgrade could have an indirect negative effect on them. But note once again, that banks do not technically need offshore funding.

In light of these considerations, we are a little puzzled why the Federal government has not taken the opportunity to stimulate the economy, sparing the RBA from having to do more work. Austerity seems to be a goal in itself, rather than a means to a greater (financing) end. Perhaps government officials still see monetary policy as being more flexible as a demand management tool than fiscal policy, even though this thinking is from a bygone era.

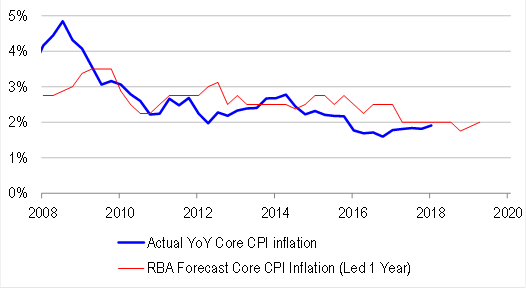

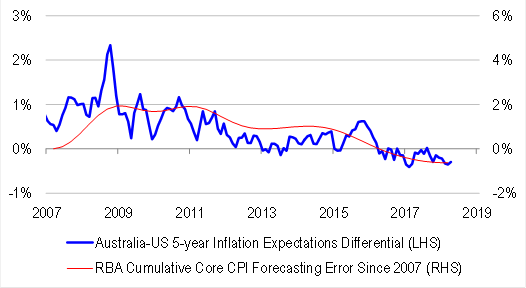

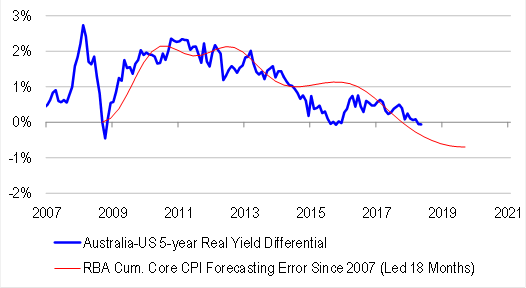

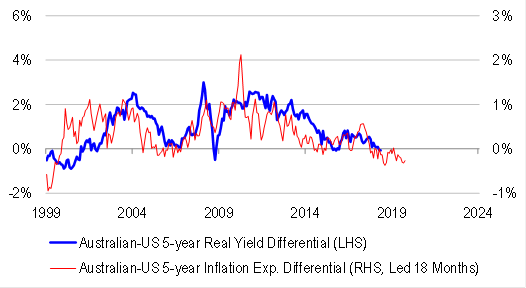

Even though the AAA rating is not really in jeopardy, there could still be collateral damage for the AUD/USD from a benign budget. The issue is whether investors feel the government has done enough to prevent de-leveraging risks from surfacing. If policy makers cannot meet their growth and inflation objectives using current settings, investors will likely question their inflation-targeting credentials even more. Historically, cumulative CPI misses relative to forecast are a powerful leading indicator of Australian-US yield differentials. In other words, investors price Australian inflation as the sum of US inflation and the credibility loss from missed targets. If yield differentials invert further, we should expect to see the carry trade appeal of the AUD/USD diminish even further.

Investment implications

We remain positive on quality exposures. The FY19 budget does little to change the growth outlook, or the balance of risks seen by the RBA. Our proprietary activity tracker is currently only pointing to growth between 1.5-2.5% annualized in the short-term – well below official forecasts, and well below most estimates of potential. Therefore, disinflation looms large, and the risk is that we see the economy undershoot RBA and Treasury forecasts. The Australian yield curve could flatten further, while Australian-US yield differentials invert further.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.