Excellent stuff from Damien Boey at Credit Suisse:

RBA officials are too optimistic about consumption

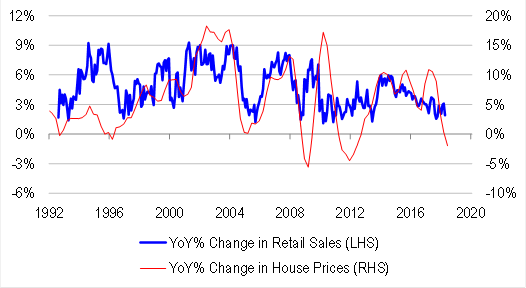

RBA Deputy Governor Debelle said recently that he could see house prices falling, but consumption growth holding up, despite housing market weakness. Presumably, he was thinking that strong labour income growth would provide households with the necessary insulation against moderate house price declines. After all, disposable income and house prices do historically explain most of the variation in consumption.

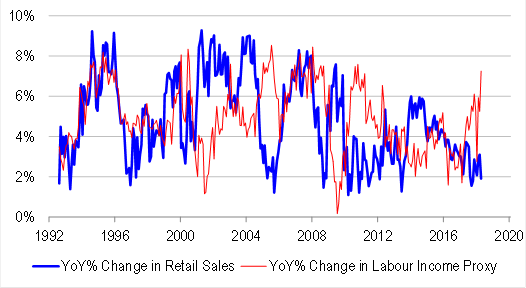

Debelle appears to be right on labour income growth. As noted yesterday, year-ended growth in hours worked has picked up to 5.4% in May – its strongest pace in recorded history. We have our reservations about data quality in lieu of heavy and positive sample rotation biases in recent months – but let us cast aside these concerns for argument’s sake. Using our proprietary wage tracker, we estimate that wages rose by slightly less than 2% in the year-to-May. This all means that nominal labour income growth is running at 7.4% annualized.

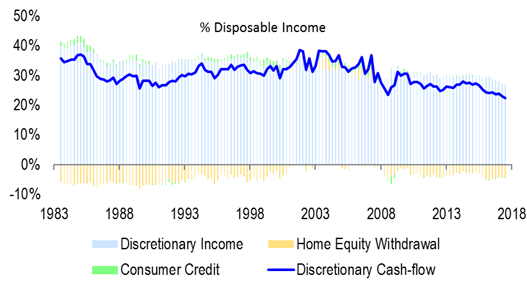

But according to NAB’s cashless retail index, retail sales probably fell between 0.2-0.6% in April, after falling slightly in March. Assuming the higher estimate materializes, this would take year-ended growth in nominal retail sales down to 1.9% from 3.1%. The slowing is very much at odds with strong labour income growth and Debelle’s thesis. It suggests that households have materially increased their saving. And historically, the saving rate has been a function of asset prices, credit availability and debt servicing requirements.

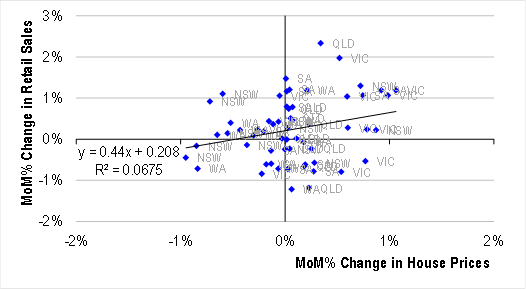

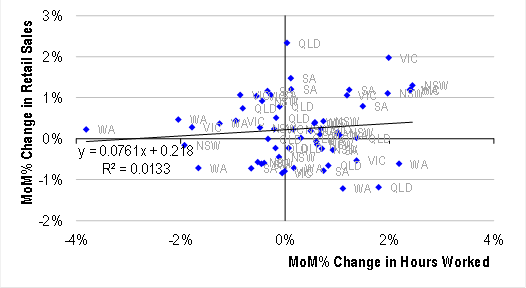

For what it is worth, the correlation between retail sales and house prices has strengthened through time, while the correlation between spending and labour income has weakened. Pooling data across states over the past year, we can also see these trends. The cross-sectional correlation between retail sales and house prices is much stronger than its counterpart with employment growth.

This is not to say that labour income has become irrelevant in driving the consumption outlook. But it is to say that many, including RBA officials, are underestimating the impact of a housing market slowdown on the consumer, because in a credit- and consumer-driven economy, consumption and credit drive employment, rather than the other way around. Also, we need to monitor the ongoing cashflow squeeze that households are experiencing from the combination of anaemic wage inflation, and rapid non-discretionary CPI inflation. Falling house prices and housing turnover due to tightening credit availability may make this situation worse by causing households to become larger net injectors of equity into their homes.

Policy implications

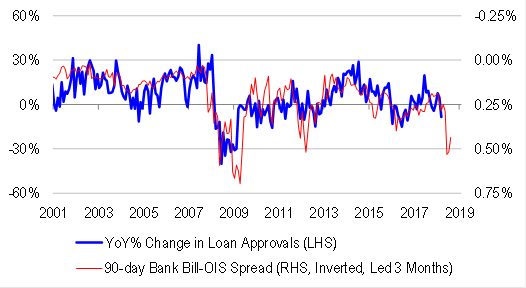

We have not yet seen the full impact of credit market tightening on the economy in the available partial indicators. But even before we do, the consumer seems to be on the ropes – and this despite apparently strong labour income growth.

These observations are significant in our view, because RBA officials are open to downgrading their outlook on the back of:

1. Credit, and money market tightening,

2. Evidence of weakness in consumption, the lion’s share of GDP.

We also note that despite recent narrowing in USD interbank credit spreads, AUD interbank credit spreads have started to widen again.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.