By Gareth Aird, senior economist at CBA:

Key Points:

- A second estimate of 2018/19 spending plans of around $90bn would imply no change to investment intentions compared to the first estimate.

- We expect the sixth estimate of 2017/18 spending plans to come in near $118bn.

- Our forecast is for the actual volume of Q1 capex to increase by 1.5% which would leave annual growth 4.3% higher.

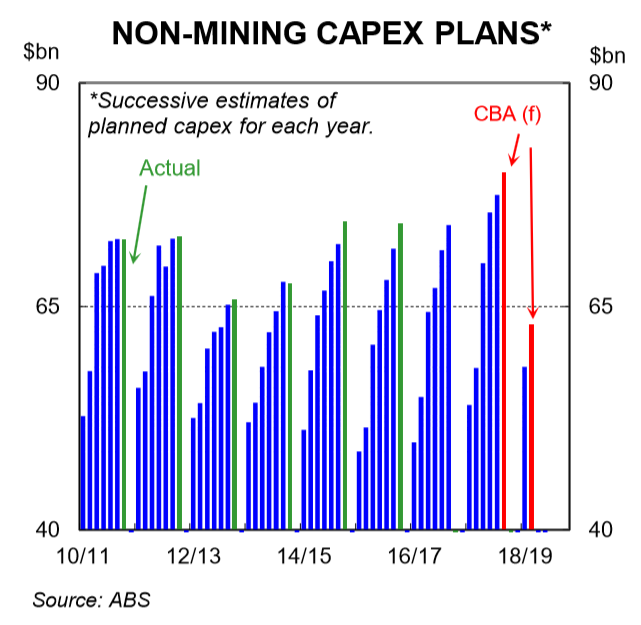

There are three key figures in this week’s capex survey: (i) Q1 2018 actual spending; (ii) 2017/18 expectations (6th estimate); and (iii) 2018/19 expectations (2nd estimate). Markets will focus on the forward looking expenditure plans, particularly the second cut of 2018/19 spending intentions.

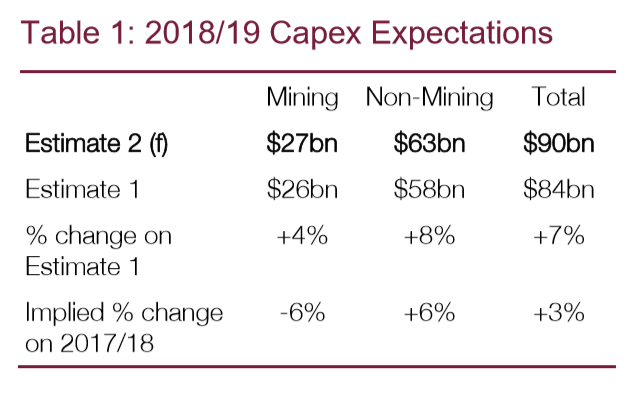

2018/19 expectations (2nd estimate) – see Table 1.

The first estimate of 2018/19 capex plans came in at $84bn. The figuring implied a lift in non-mining investment of around 6% when compared with 2017/18 and a fall in mining capex of around 6%. All up, a modest lift in total nominal investment of around 3% (note that the capex survey excludes a number of large and important industries which include agriculture, health and education).

Second estimates for spending plans can vary significantly from actual spending. A comparison of previous second estimates with actuals shows that non-mining firms will almost always underestimate their capex plans at both their first and second stabs. But the magnitude of the miss can vary greatly in any given year. We consider a second estimate that comes in larger than $63bn as an upgrade on the first estimate and also a good outcome. Less than $63bn would imply a downgrade (see Table 1). Non-mining investment has lifted over the past 1½ years and policymakers will want to see that trend continue, particularly as the unemployment rate has been stuck at 5½% over the past 9 months.

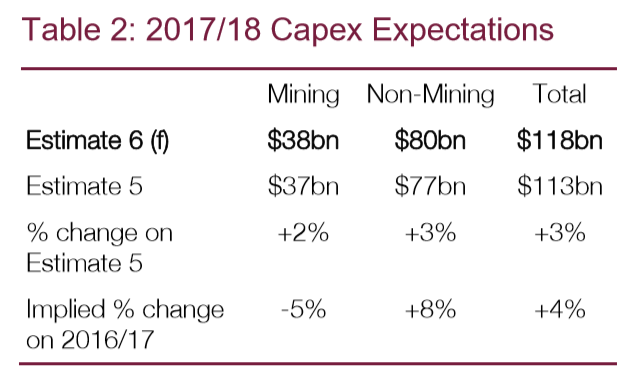

2017/18 expectations (6th estimate) – see Table 2.

The last reading from three months ago implied a 4% increase in nominal capex this financial year. The detail suggested a fall in mining capex of 5% and a solid 8% increase in non-mining investment. We anticipate that we won’t see too much change in the estimate for mining capex. But we expect an upgrade in non-mining investment of around 3%. We consider a sixth estimate that comes in larger than $118bn as an upgrade on the fifth estimate. Less than $118bn would imply a downgrade.

Q1 2018 actual

We expect the actual volume of Q1 capex to rise by 1.5% after a 0.2% fall in Q4 2017. Such an outcome would leave annual growth 4.3% higher. The actual spending data will help us to firm up our estimates of Q1 GDP (due 6 June).

Risks

While employment growth has eased, the business surveys remain strong. And job vacancies continue to lift in the resources sector. On balance, these factors point to some modest upside risk on our forecasts for 2018/19 capex expectations.