BofAML says falls are over:

The China backdrop remains negative but appropriately priced, while the fact that Australia is becoming a more diversified economy means that positive domestic factors should be more supportive moving ahead.

The Australian dollar trade weighted index is trading close to its lowest level since 2015-16, a time when the China macro backdrop was far more negative and it is in fact undervalued relative to interest rate differentials and terms of trade. We think this is a good time to buy AUD crosses amidst broader USD strength and remain long AUD/JPY; the longer-term outlook for even AUD/USD is bullish – we expect a move toward the mid-0.80’s by 2019.

The trade-weighted index and terms of trade don’t look especially out of whack to me:

If they are it’s because the TWI is a more real time indicator whereas the terms of trade lags.

It remains obvious that the high terms of trade are still holding up the dollar versus interest rates, today being the only period in history when a trend fall in the interest rate spread was not matched by the same in the AUD:

There is one way that the AUD could rocket to 85 cents. China stimulates again just as the US slows. That could happen in twelve months time. But it’s not on the radar right now. China has its slowdown in hand and the US is still booming.

The other possibility is that that remains the case until the Fed goes too far. But even then the AUD would first fall a long way as global recession loomed before it rebounded on Fed stimulus.

Meh, the risks remain down for AUD as domestic demand softens with housing and China slows dragging down iron ore. 70 cents by year end remains the MB view.

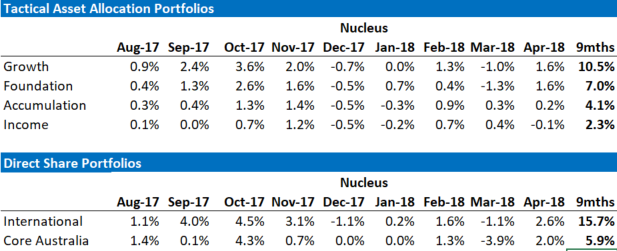

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.