The Australian’s Judith Sloan has slammed Paul Keating’s latest spruik calling for Australia’s superannuation guarantee to be raised from 9.5% to 12%, labelling compulsory superannuation a “giant con”:

It is becoming increasingly apparent that Australia’s system of compulsory superannuation is essentially a giant con…

When it comes to the dependence on the Age Pension, it has to be said that superannuation has been a failure. The proportion of old people on the Age Pension has barely shifted (about 80 per cent) and the projections into the future point to little change to this figure.

… the nirvana of more and more people providing for their own retirement is unlikely to be achieved. Don’t be fooled by the excuse that the system is still immature — it has been in operation since 1991.

Note also that the government gives up considerable tax revenue on an annual basis by virtue of the concessional taxation of superannuation.

From a holistic public finances viewpoint, superannuation looks like a bad deal because the cost of these concessions are not being fully clawed back by lower spending on the Age Pension…

The plan is that the SCG will be 12 per cent by July 2025. Every 0.5 percentage point increase costs the budget about $2bn a year.

This is the absolute last thing that should be happening — asking workers to forgo even more in current consumption while the ultimate value of having a larger superannuation balances is so dubious.

The real beneficiaries will be the superannuation industry and its vast number of hangers-on.

Keating has many economic policy achievements of which he should be proud, but he should hang his head in shame when it comes to the system of compulsory superannuation. It is a complex mess that lets down far too many superannuants, particularly young people, while failing to meaningfully relieve the budget of the net cost of paying for the Age Pension. Its main purpose is to enrich the industry itself.

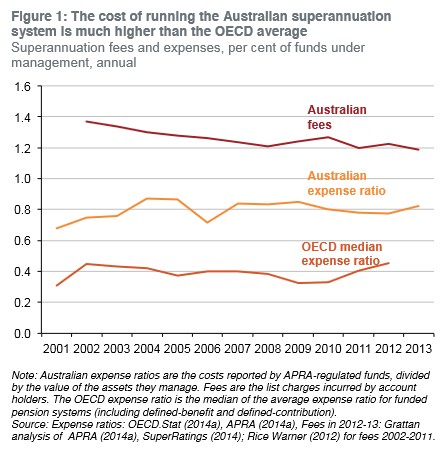

If superannuation was a well functioning and competitive market, average fees would have fallen as the value of funds under management has risen. This is because it should not cost ten times more to manage $1 billion of funds under management than it does to manage $100 million – i.e. basic economies of scale.

Instead, despite the huge explosion of superannuation balances since the superannuation guarantee (compulsory super) was introduced in 1993, average fees and expenses have barely changed and are way above the OECD average, according to the Grattan Institute (see below charts).

As noted by Grattan:

A larger system of larger funds should have incurred lower costs and charge lower fees, because big funds have lower costs…

Australian funds charge fees that are three times the median OECD rate, on average… Many countries have superannuation pools much smaller than Australia’s, yet their funds charge customers much less.

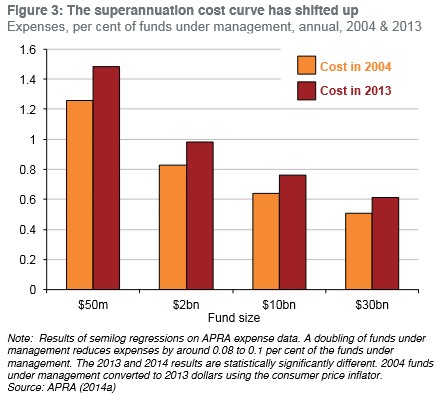

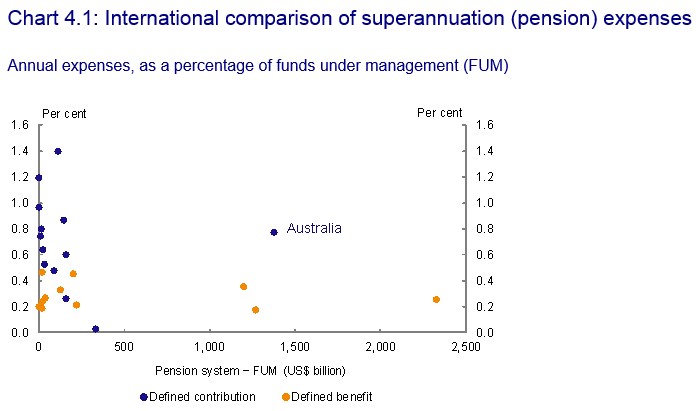

The Murray Financial System Inquiry noted similar concerns, as illustrated in the below charts:

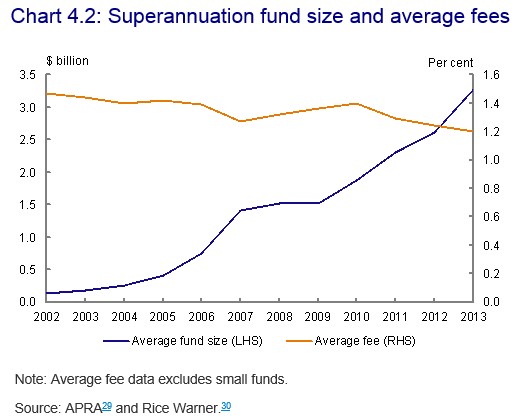

And that super fees had not fallen in line with what could have been expected given the substantial increase in scale:

Clearly, then, Australia’s superannuation funds are not just inefficient, but are also gouging members. And this has been facilitated by Australia’s compulsory contributions (currently set at 9.5% of employee wages), which has provided the industry with a “sheltered workshop” by which to operate.

Worse, the Grattan Institute estimates that increasing in the superannuation guarantee to 12% would overwhelmingly benefit the wealthy in addition to worsening the Budget by $2 billion a year:

“Increasing the rate will not help these earners in retirement: most of the benefits will flow to high-income earners, while low-income Australians could cop both lower incomes in retirement and lower wages today”…

The institute also repeated its criticism that future increases should be scrapped because of the budgetary impact of revenue foregone thanks to the concessional tax rates enjoyed by superannuation. It believes the budget would be $2 billion a year worse off if the guarantee hits 12 per cent.

Therefore, raising the superannuation guarantee would do little to boost superannuation savings for lower income workers – those most likely to become reliant on the Aged Pension – given the lion’s share of superannuation concessions would flow to higher income earners (even after the recent modest reforms).

Such a move would merely heighten inequities already present in Australia’s superannuation system. It would rob younger (and lower paid) workers of much-needed disposable income at a time when real wages are falling, and worsen the long-term sustainability of the Budget.

About the only winners from such a policy would be the superannuation industry, which would get to ‘clip the ticket’ on more funds under management and earn fatter profits.

This is why reforms to fix the underlying problems in Australia’s inefficient and inequitable superannuation system (e.g. excessive fees, unequal distribution of concessions on contributions/earnings, etc) is vital before the government even considers raising the compulsory superannuation rate.

unconventionaleconomist@hotmail.com