The DXY charge was back last night as EUR fell:

AUD was slammed:

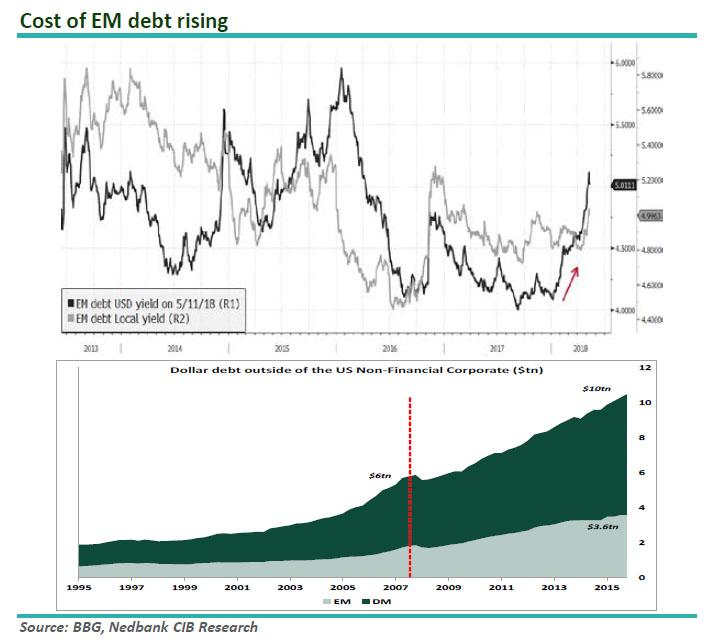

But EMs fell more:

Confirming the USD charge is gaining momentum, gold was smashed:

Oil held up:

Base metals were mixed:

Big miners fell:

EM stocks were smashed:

As EM junk gave way:

Treasuries were pounded and the curve even managed to steepen:

Bunds copped it too:

And stocks fell as yields took off:

The culprit? Good US data versus softening in Europe and China. The NY Fed shots the lights out at 20. Retail sales hit 3.6% annualised in April after running at a revised 9.6% in March. And builder confidence rebounded. German GDP missed and yesterday’s China data showed clear signs of slowing. Making matters worse, Italy’s new government looks pretty radical.

The result is capital flight everywhere from India to Argentina to Turkey:

Even CNY was smacked to a new low which will not please anybody:

That’s monetary tightening right across emerging markets as all of that USD funding gets more expensive fast:

The next shoe to drop is Chinese growth and commodity prices.

AUD is toast.

———————————————–

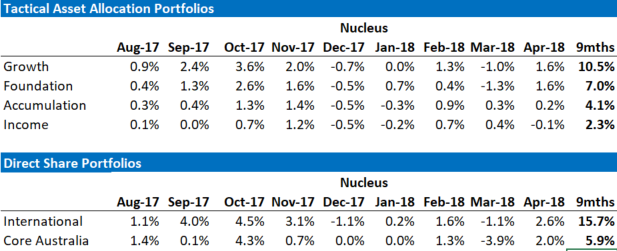

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively international stocks, but with bonds and other assets as well to ensure a more conservative mix.

The recent performance of both is below:

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.