Phil Lowe uttered the words finally in a speech last night:

Domestically, for some time, we have seen the main risk to be related to household balance sheets. For a while, trends in household credit were quite concerning. On this front, things now look less worrying than they were a while back, although the level of household debt remains very high, which carries certain risks. In terms of financing, we also discussed the potential for some tightening in financial conditions in Australia. In the United States, the cost of US dollar funding has increased for reasons not directly related to monetary policy and this increase is flowing through into higher money market rates in Australia. We expect some of this to be reversed in time, although it is difficult to tell by how much and when. It is also possible that lending standards in Australia will be tightened further in the context of the current high level of public scrutiny. We will continue to watch these issues carefully.

Though the credit crunch is still couched as risk not reality. Futureboom must always remain in place.

“People are still going to want to buy and own a home, so it’s not like any of this changes fundamental demand, but it will change the process and it probably will make it harder for people to be successful in their applications,” Mr Elliott said on a call with analysts.

“And it probably means that banks are going to be just that little bit more cautious, either just psychologically, because of a little bit of fear, or putting in place more processes, and in that environment, that will just slow things down I imagine.”

“That will by necessity slow down, I imagine, most people’s ability to get a loan,” he said. “You’ll have to be more prepared.”

Mr Elliott said there would be more likely they’ll say “no” to marginal customers who would previously have been given credit. “It will be a little bit harder at the margin, but not en masse,” he said.

It only needs to happen at the margin. That’s where price changes come from. Domainfax found a moment of clarity:

Capital Economics’ Paul Dales, for example, believes the end of the country’s housing boom will probably mean economic growth will fall shy of expectations.

Crucially, falling house prices married to high debt may well “prompt households to stop spending beyond their means”, Dales says. “Consumers won’t continue to offset low income growth by reducing their saving rate.” His base case is that the RBA won’t lift until late 2019.

…Where does the RBA go from here? Nowhere fast. As a result it’s looking more and more likely that we will roll into the next inevitable recession with very little monetary policy ammunition.

Advertisement

Add the coming China slowdown and the RBA will have no choice but to cut, for all the good it will do.

Damein Boey at Credit Suisse sums up the reality a lot better than Phil Lowe does:

We are concerned about the Bank’s dismissiveness of rising bank funding costs. We feel that the cause of rising funding costs is not yet well understood. Even though offshore USD funding costs have moderated in recent weeks, Australian funding costs remain very wide by historical standards.

We are concerned about incremental tightening of lending standards coming through in the wake of the Bank Royal Commission.

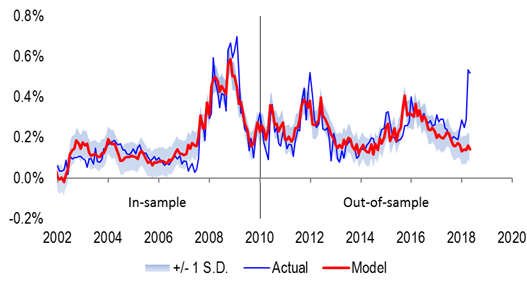

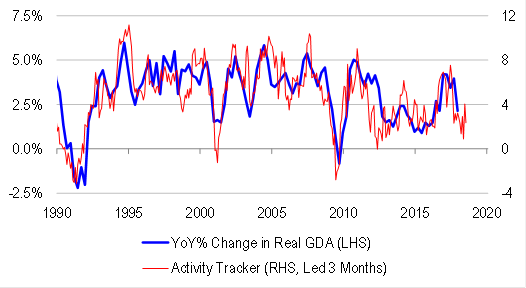

We are also concerned that the RBA is not changing its growth and inflation forecasts despite the fact that the data is surprising to the downside…For what it is worth, our proprietary activity tracker continues to point to sub-trend activity growth (measured across production and income measures of activity). In the near-term, the risk is that growth and inflation continue to undershoot the Bank’s forecasts, putting more downward pressure on yield differentials:

Advertisement

Falling house prices, forced tightening and all out of rate cuts.

Futureboom!!

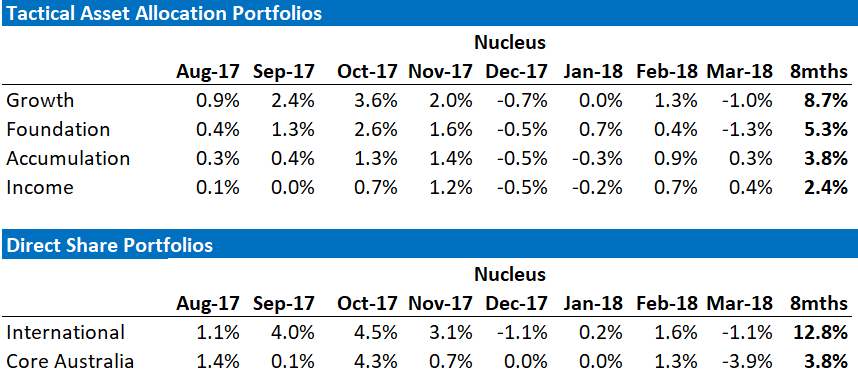

David Llewellyn-Smith is the chief strategist at the MB Fund which offers two options to benefit from a falling AUD so he is definitely talking his book. The first option is to use the MB Fund International Stocks Portfolio which is always 100% long as a part of your own asset allocation mix. The second option is to use an MB Fund tactical allocation in which we choose the asset mix for you, including exclusively to international stocks but with bonds and other assets as well to ensure a more conservative mix.

Advertisement

The recent performance of both is below:

If these themes interest you then contact us below.

Advertisement

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.