By Catherine Cashmore

The proposal to cut the company tax rate from 30% to 25% has received much media attention.

We are repeatedly told it is needed to boost investment.

The rational follows that companies are more likely to invest in productivity if they don’t have to pay as much tax on their gross income.

It sounds great to businesses. Especially smaller companies that are struggling against a macro economic environment that is not conducive to growth.

But will a company tax cut really profit productivity and labour? Or is there something missing in the equation?

A similar query came up when Thomas Piketty released his magnum opus ‘Capital in the Twenty-First Century’.

It attracted more attention than any other economics book in recent history.

Praised by Nobel-prize winners and politicians alike, Piketty claimed to have produced a ‘new theoretical framework that affords a deeper understanding of the underlying mechanisms of Capital and Inequality.’

According to Piketty, the world risks ‘terrifying consequences’ unless a global wealth tax is implemented — a policy that requires universal recognition across country borders.

Without it, Piketty argues that the accumulation of capital will become increasingly concentrated in the hands of the rich, accentuating the inequality gap and keeping the poor, poor.

It took a 26-year-old US grad student (Matt Rognlie) to realise that Piketty had ‘Got it wrong!’

Rognlie split Piketty’s data between the net capital income from land, and the net capital income from all other sources and noticed something ‘shocking.’

‘A single component of the capital stock—housing (land)—accounts for nearly 100% of the long-term increase in the capital/income ratio, and more than 100% of the long-term increase in the net capital share of income.’

In other words, it is land (not capital) that has taken all the gains.

Bloomberg declared it ‘a dramatic, startling insight that was somehow overlooked before Rognlie came along.’

The Economist heralded it the ‘most serious and substantive critique that Mr Piketty’s work has yet faced.’

But of course, Rognlie had merely done what the classical economists had been doing for centuries.

He separated land from capital (that which is man-made), and in doing so uncovered the obvious.

The insight should not be surprising to any Australian – especially those living in Sydney and Melbourne.

They face the highest real estate prices against wage income we have ever witnessed in this country – and as a consequence, hold highest household debt in the OECD.

The total value of Australian residential real estate is over 6.6 trillion.

Land makes up at least 60% of that value in our two biggest capitals.

The economics term used to quantify this is “land rent” or “economic rent.”

Land rent is not an annual payment made by a tenant.

It’s the revenue that can be earned from sitting on a block that is appreciating in value with no effort or enterprise.

Can you imagine what it would do to productivity if we lowered the price of land (and private debt levels) instead of granting a company tax cut?

After all, company tax is not payable unless the company actually makes a profit.

The same cannot be said for the rents and prices that companies and individuals pay for their business premises, or homes.

In the simplest terms, the higher the rent or price paid, the less money available for wages and business investment.

The classical economists understood this.

They also recognised how changes to tax policy have the ability to either mute or inflate the housing cycle.

In a competitive market, real estate prices are merely a reflection of what the banks are willing to lend.

Any tax cut to labour income increases the borrowing capacity of those purchasing land – and as a consequence, land inflation.

In other words – the direct benefit of tax cuts on labour and capital are quickly competed away in higher land prices.

The roll on effects to the broader economy are significant.

Speculation fuels the real estate market when land prices are high and increasing.

Employees need to live further from business premises to access affordable accomodation – increasing commute times and productivity losses.

Properties are held vacant and land is banked, restricting the available supply further.

Homeless numbers increase, putting pressure on the welfare system.

The economy suffers as a result.

Some argue that the equity in land can be invested back into productive labour.

However, the macroeconomic effects highlighted above are clear evidence that this is not really the reality.

There is nothing quite so compelling to real estate investors or home owners as “growing rich in their sleep” – as the classical economists would quip.

Successful producers may reinvest their profits into further production.

But rent seekers – those benefiting from unearned gains – know where the easy profits lie.

Dr Gavin Putland demonstrates this in his latest paper “Trickle Down Economics” for the taxation think tank Prosper Australia.

The report investigates the relationship of land’s share of GDP against economic growth.

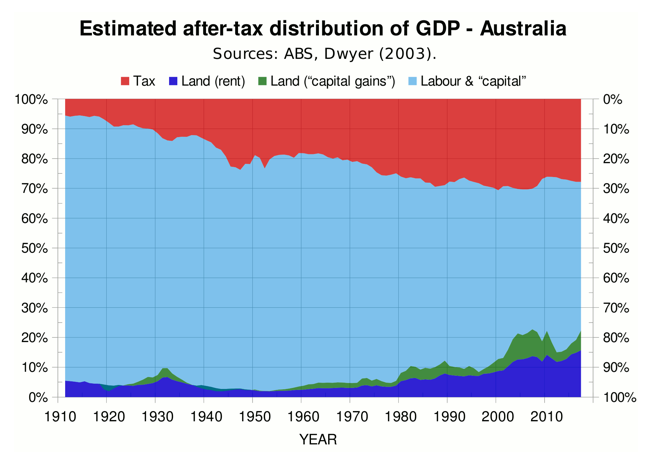

The following graph demonstrates the effect quite well:

The dark blue band (including the small aqua-coloured segments) show the land rent – i.e. the value (assuming a yield of 5% per annum)

The green band shows the real “capital gains”.

This assumes that 6% of the land value is sold each year, having been bought 8 years earlier. (Hence no “capital gains” are shown for the first 8 years.)

Where the green section gives way to the small aqua segments (1919–22 and 1938–49), the “capital gains” are negative. During these periods, the land value is indicated by the top of the aqua band (measured on the left-hand scale), while the land rent plus “capital gain” is indicated by the bottom of the aqua band.

The red band shows tax for all levels of government as a fraction of GDP (measured on the inverted right-hand scale).

Finally, the light blue band is the ‘meat in the sandwich’. It demonstrates what is left over for labour and “capital” when the others (land rent and tax) have taken their share.

The squeeze is significant.

Putland shows that land rent as a proportion of GDP has increased from 2% in the early 1950s to more than 20% of GDP in 2017.

Since 2003, the economic rent of land has consistently exceeded 15% of GDP.

Significantly, the “Global Financial Crisis” in 2008 and the recession of the early 1990s were preceded by notable squeezes on the percentage of GDP accruing to labour and capital, as distinct from land.

Putland is not the only one to point out how high and rising land values can lead to massive economic recessions.

In 2014 the IMF (International Monetary Fund) highlighted that

“..boom-bust patterns in house prices preceded more than two-thirds of the recent 50 systemic banking crises…..” (IMF “Era of Benign Neglect of House Price Booms is Over” June 11 2014)

The double edged sword of higher land prices and damaging productivity taxes (which produce deadweight losses) lead to a drain on the capacity of workers and employers to invest in future growth.

Accordingly, Putland highlights the gains to landowners do not “trickle down” to labour and capital as one may imagine.

There is a “trickle-up” effect: when labour and capital get a greater fraction of GDP, economic growth is faster.

The overall effect of that growth eventually makes landowners better off in *absolute* terms, in spite of their smaller *fraction* of the pie.

However, without changes to land (or tax) policy, the overall bargaining position of labour and capital is reduced, and productivity decreases as more and more wealth is diverted back to landholders.

This is due to David Ricardo’s “Law of Rent.”

*Net* returns to labour and capital tend to become independent of location (due to their mobility).

However, any locational boost to the *gross* returns is claimed by the owners of location itself — through the economic rent of land.

To explain it another way.

Wealth is divided among economic rent (in this case land), wages, and profit as their respective returns.

Production = Rent + Wages + Profit,

To rearrange the equation,

Wages + Profit = Production – Rent.

In other words, wages and profit are not what labor and capital *produce* – they are what’s left after economic rent is taken out!

The locational value of land will always take the gains.

How do we combat this?

Putland’s cure lies within the tax system.

Similar to the Henry Tax Review in 2008 when it concluded “economic growth would be higher if governments raised more revenue from land and less revenue from other tax bases.”

Most of our taxes carry what is termed ‘deadweight losses.’

Deadweight losses are easy to understand.

Income tax is a discouragement to work.

Payroll tax acts as a discouragement to employ – so on and so forth.

Quantifying the effect that deadweight taxes have on the economy as a whole is not easy.

Some researchers suggest it’s as much as $2 for every $1 collected.

In other words – the “revenue” from your income tax payments may as well be thrown down the drain. They cause more harm than good.

(Meditate on that next time you do your tax return.)

Contrary to the above, taxes that improve the competitive position of tenants and land buyers relative to landlords and sellers — such as land-value taxes, and vacancy taxes (applicable to both vacant land and vacant accommodation) — have a negative deadweight!

As Putland highlights.

Taxes that make it uneconomic to own vacant land and buildings, force owners to either build accommodation and seek tenants, or sell their land to someone who will.

A land-value tax does not penalise the building and letting of accommodation.

Rather it increases the amount of accommodation as vacant properties and banked lots are employed into use – thereby lowering rents and prices.

Importantly, land taxes fall exclusively on the owner of land – they cannot be passed onto tenants.

All else being equal, a tax on land, reduces the amount buyers have or are willing to pay upfront. The effect is to lower land prices.

Land taxes are a way to claw back the economic rent that is currently privatised by landowners, (only to be reinvested into more speculative investment.)

Company tax cuts need not be a bad thing if they are replaced by taxes that reduce speculation in the land market.

On their own however, they will merely add to the boom bust nature of our economy.

Putland’s paper will be launched in Melbourne on Wednesday April 18th at 6pm. For more information contact Prosper Australia.