Welcome to the great Australian bank bear market

According to the stock market, Australian banks are not well.

Let’s start with the technicals. The mortgage monsters – CBA and WBC – are both caught in bear markets with the former down -25% and the latter nearly -30% from 2015 highs. Both are exhibiting bearish descending triangle patterns and both are at crucial support levels:

If the lows reached throughout the last three years break then big downside potential opens up. The question is will they break and by how much?

The narrative around the banks is not encouraging. The peak of 2015 was reached as global capital chased yield higher amid lowflation and quantitative easing. But as yields have risen, most especially in the US, that has died away and foreign capital has flowed out. There is no reason to think that that will change any time soon given the RBA will not hike rates and may well be forced to cut when the terms of trade falls resume in H2 as China slows.

And the bank narrative gets worse. The Hayne Royal Commission runs for much of this year and it is now abundantly clear that it will take an enormous dump on the banks throughout. Let’s quickly recount the rain of shit so far, via UBS:

Fraud and Bribery

Counsel Assisting, Ms Rowena Orr, QC: “I want to put to you is that NAB knows, & you know, that there were unsuitable loans, there was false documentation, there was dishonest application of customers’ signatures on consent forms & there was the misstatement of some loans in loan documentation.

The whistleblower is recorded as saying: ‘One customer recently said at a particular branch, they told him he could borrow $800,000, but the valuation was only $450,000. The whistleblower said the money exchanges hands in cash, in envelopes, white envelopes usually over the counter. Money is deposited at CBA, so NAB can’t detect the deposits’. Now, this is the information provided by the second whistleblower. Is that right?”

Mr Waldron, NAB – “That’s correct”

Counsel Assisting, Ms Rowena Orr, QC – “And the whistleblower tells NAB that these people are making up fake payslips, fake ID, fake Medicare cards … They charge $2,800 bribery for each customer for home loans”.

Failure to verify customer income

Counsel Assisting, Ms Rowena Orr, QC – “And it wasn’t just the fact for Mr Meehan, that had submitted more than 50% to a single lender; it was also the fact that the particular lender that he had submitted them to was Westpac because Aussie [Home Loans] had formed the view that the credit assessment processes at Westpac were more lax than at other lenders; is that right? Aussie had formed the view that the fact that they [Westpac] were just requiring a letter of employment, as opposed to payslips, would be something that brokers would become aware of to be easier to provide the documentation that was necessary. And do you mean, by that, a letter of employment is an easier document to falsify?”

Lynda Harris, Aussie Home Loans – “Yes”.

Failure to assess customer expenses

Counsel Assisting, Ms Rowena Orr, QC – “The first issue I think that’s worth mentioning this across home loans…it’s a lack of questions & verifications about expenditure. When we ask for copies of their assessment, is that it looks much more likely that a benchmark has been used than they looked at the consumer’s actually expenditure, which can vary considerably from a benchmark figure. There is also very little evidence that expenditure has actually been verified in any way.”

Mr Ranken, ANZ – “ANZ recognised there were instances where it lacked evidence to show that genuine inquiries had been made”

Failure of internal controls

Counsel Assisting, Mr Dinelli – “The remediation paid demonstrates that processing errors occur across a variety of credit products. They occur predominantly by reason of the application of automated processes, but human errors left unchecked often underlie them.”

Mr Van Horen, CBA – “It was the error we made in our serviceability calculation and the mapping the data flows … without overstating it, doomed to fail … having robust change processes, I think, was our failing and it’s clearly an area of ongoing work.”

Failure to report misconduct to ASIC

Counsel Assisting, Ms Rowena Orr, QC – “NAB knew enough to sack five employees for dishonesty and for conflict of interest, is that right? It knew enough by November to sack people for those reasons. Are you telling me it didn’t know enough to tell ASIC that there was a problem?”

There really isn’t much else to get wrong in banking. The punitive response is unknown but it will likely comprise:

- higher lending standards hitting top line growth;

- intensified borrower scrutiny hitting bottom line growth;

- more capital and possibly mandated dividend cuts.

The RC will submit an interim report no later than 30 September 2018, and will provide a final report by 1 February 2019. There’s not much comfort there. The timetable flows straight into campaigning for the next federal election which is very likely to be May 2019. The RC was Bill Shorten’s baby from the outset and he will turn it into a major electoral event going hard on punitive reforms that will dampen already low profit growth.

Moreover, barring a miracle he’ll win the election. That raises the prospect of the regulatory smash tipping straight into negative gearing reform in the Spring of 2019 and more house price falls. This is likely to transpire against a backdrop of a still slowing China, falling terms of trade and emptying Australian residential and infrastructure building pipelines adding to profit growth pressure via rising bad loans.

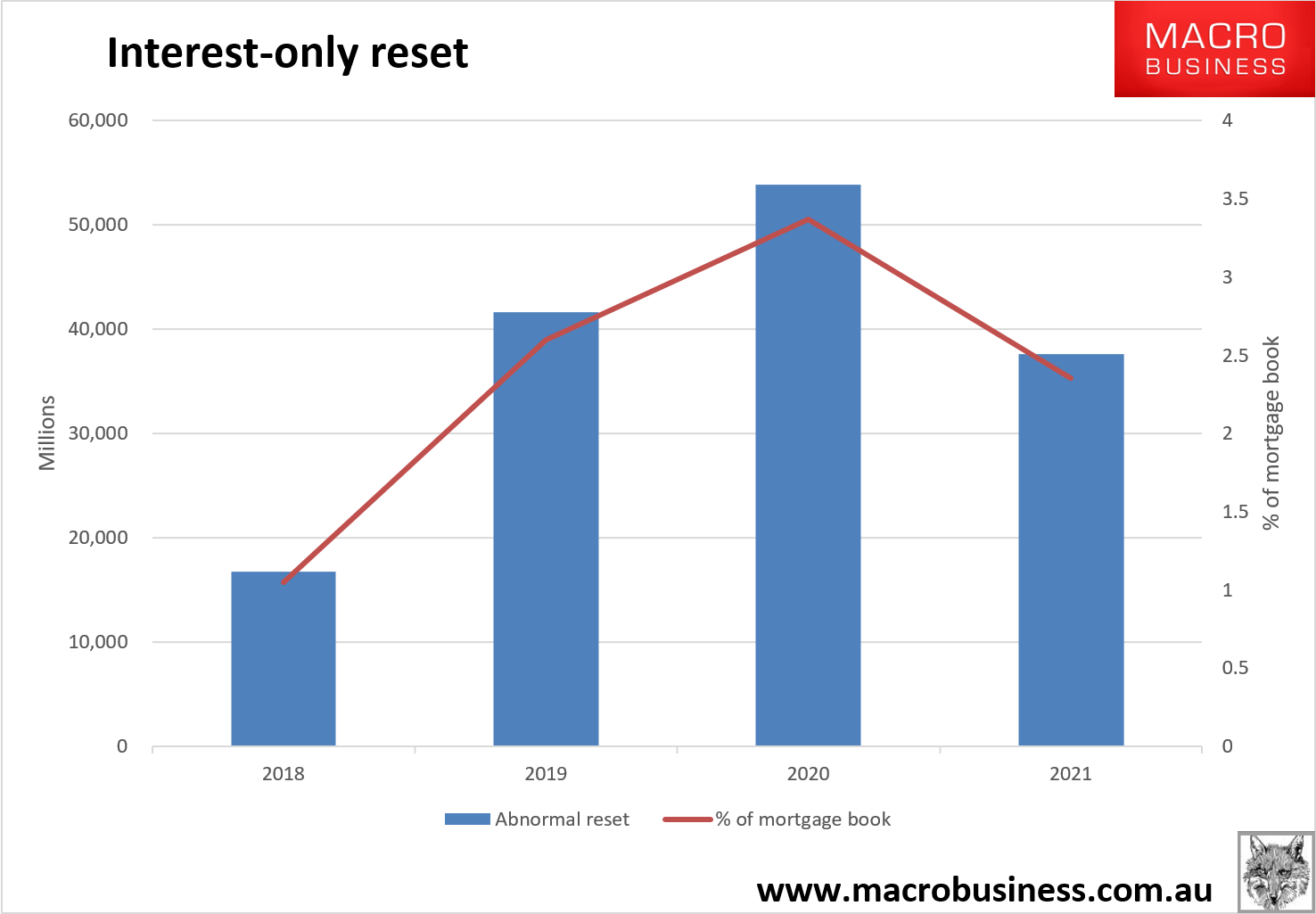

And that is going to run headlong into the baked-in interest-only mortgage reset. There is confusion about how much the back book and front book of the banks can absorb the reset. Banks can only issue 30% of new loans as interest-only now. That’s roughly $40bn per quarter which would mean that the reset could absorb the bank’s entire front book IO capacity. So some large portion will have to transpire in the back book. My best guess how much that will be based upon the history of what the banks have managed previously, I’ve guessed they will be able to manage $25bn per quarter in the back book as the great reset builds. That means we’ll see the following total resets to principle and interest:

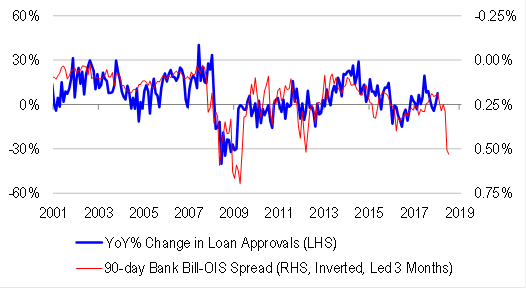

The profit outlook gets worse yet. The global cycle is already throwing up rising short term funding costs:

Which are beginning to impact long term funding as well:

So the outlook for net-interest margins is also deteriorating.

Is enough of this bad news narrative discounted already? Let’s check the critical valuation metrics. The banks are trading on roughly average forward price to earnings ratios of around 12x:

There’s probably still room to fall there. However, versus the wider market the banks are already very cheap:

And the dividends are getting fat, nearly 10% grossed up for tax credits:

Price-to-book is also cheap:

Consensus EPS growth outlooks are already weak but probably not weak enough, especially for an openly corrupt CBA with a serious risk process problem:

So, are the banks cheap enough yet? Perhaps for now given the 10% dividend bribe.

But once we get into the combined challenges of 2019 when funding costs, rising bad debts, the interest-rate reset, regulatory and reform risk all collide in a profits crush then dividend cuts will follow as sure as night follows day.

This bear market has legs.