Who would have thought: Budget measures aimed at helping first home buyers (FHBs) have actually driven-up the price of housing at so-called ‘affordable’ price points, thus proving self-defeating from an affordability perspective. From The Australian:

Grants for first-home buyers are pushing up prices for affordable houses in the most heated markets as first-time buyers get onto the property ladder at the fastest pace in five years.

Buyers in outer Melbourne and Geelong are taking advantage of stamp-duty discounts introduced last year and bidding up prices, while most first-time buyers have also been able to get into the expensive Sydney market…

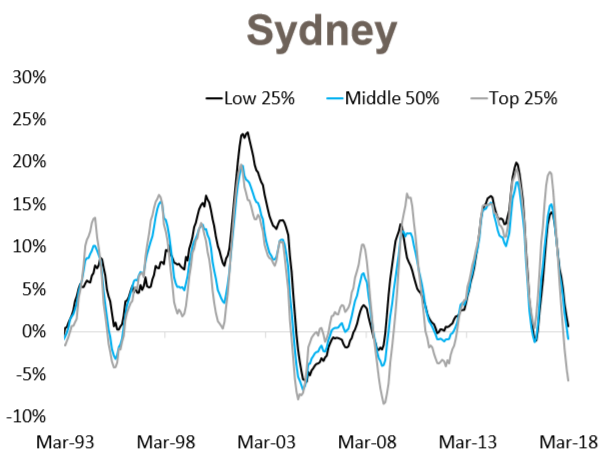

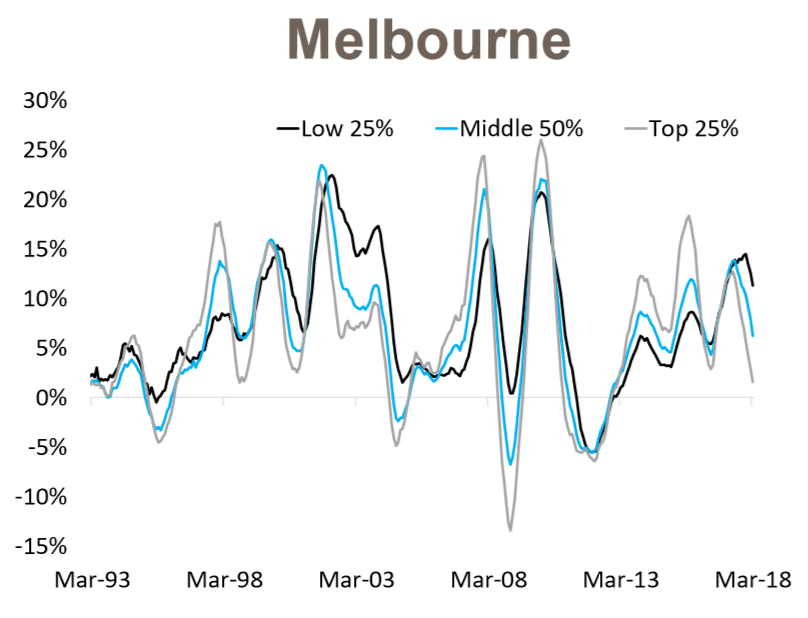

“Despite overall slowing conditions in Sydney and Melbourne, the CoreLogic home value indices results show that the more affordable end of the housing markets in these cities as still seeing values rise and likely generated by first-home buyer activity”…

“We’ve definitely seen an influx of first-home buyers,” said McGrath Geelong principal David Cortous, with buyers moving from Melbourne for affordable homes.

“We’ve also seen a big increase in the price of those properties … anything that was $500,000 jumped up to almost $600,000 because of the demand.”

…the discounts fuelled price growth in entry-level outer suburbs, with houses 20km or more from the CBD up 13.8 per cent last year compared with an 11.1 per cent rise for houses within 10km.

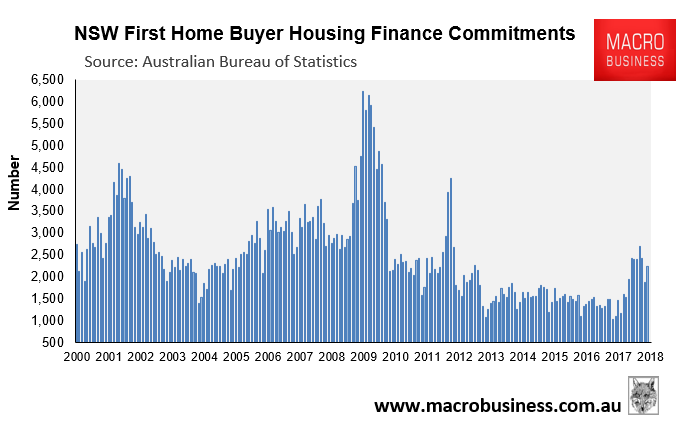

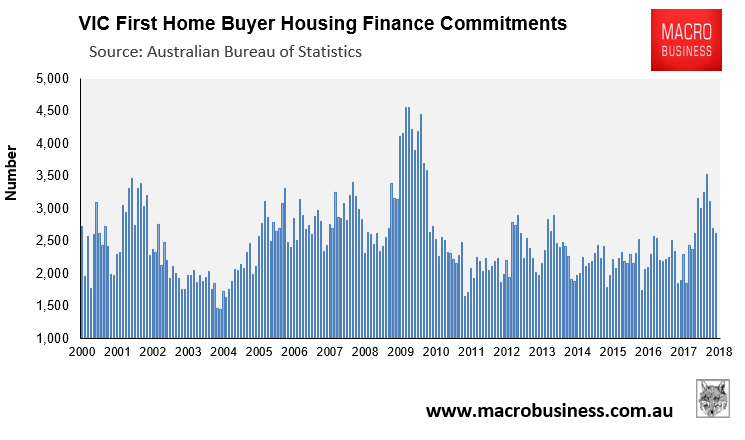

The NSW and VIC state governments implemented stamp duty concessions from 1 July 2017, which has led to a spike in the number of FHB mortgage commitments:

But also stronger price growth at the lower (‘affordable’) end of the housing markets in both Sydney and Melbourne:

All of which goes to show that you don’t improve affordability by sucking marginal buyers into the market with budget bribes, as well as increasing their ability to pay. The end result of these types of policies is always the same: increased demand and higher property prices, thus proving self-defeating.

Rather, what is needed from an affordability perspective is a broad package of policies that reduces the systemic cost of housing by lowering demand and increasing supply, including:

- Normalising Australia’s immigration program by returning the permanent intake back to the level that existed before John Howard ramped-up it up in the early-2000s – i.e. below 100,000 from 210,000 currently [reduces demand];

- Undertaking tax reforms like unwinding negative gearing and the CGT discount [reduces speculative demand];

- Tightening rules and enforcement on foreign ownership [reduces foreign demand];

- Extending anti-money laundering rules to real estate gatekeepers [reduces foreign demand];

- Banning borrowing into property by SMSFs [reduces speculative demand]; and

- Providing the states with incentive payments to:

- undertake land-use and planning reforms, as well as provide housing-related infrastructure [boosts supply];

- swap stamp duties for land taxes [boosts effective supply];

- reform rental tenancy laws to give greater security of tenure [reduces demand for home ownership and reduces rental turnover]; and

- force developers to supply housing for lower income earners via inclusionary zoning [boosts supply of affordable rentals].

MB has actively promoted these reforms for at least five years, yet they continue to be ignored.