Commodity markets have gone crazy in the past two days over the recent PBOC reserve ratio cut despite it being an obvious signal that demand is about to fall and such measures not being anything like a sufficient response to prevent it.

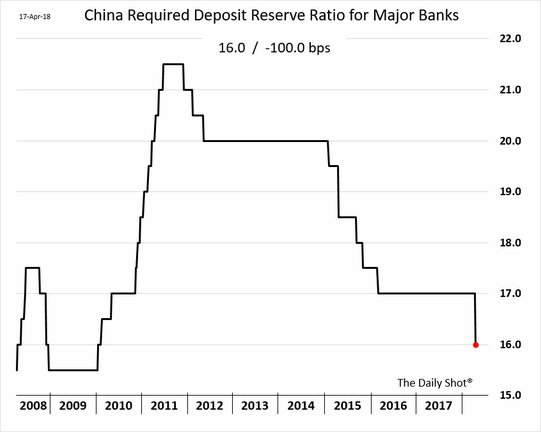

So today I thought I’d run through what will be such a signal. The RRR cut is useful to start with. Notice how the PBOC began easing it right through the demand collapse of 2015:

But it wasn’t until early 2016 that it got any traction. That was achieved via a range of other stimulus. The three most important were interest rate cuts, housing stimulus and infrastructure spending.

Here’s the first:

It will be difficult to cut interest rates any time in the near future. The cuts of 2015/16 played a major part in triggering Chinese capital outflow and the tumbling yuan that nearly dragged the globe into recession. If that were to happen amid the US trade wars it could be very probably triggering a market-rupturing end-of-cycle event.

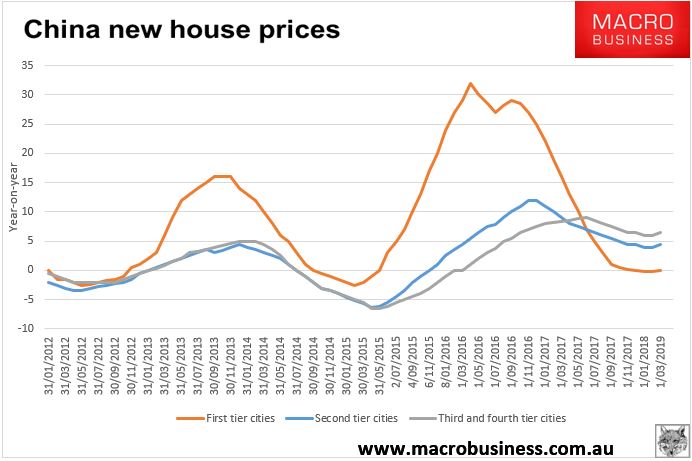

Rates have not risen during the two year mini-boom, either. Yet housing has still slowed markedly:

This has been achieved via city-level and regional macroprudential policies that have controlled mortgage lending:

Yet as things stand, first tier cities are in a slow melt while lower tiers are growing at sustainable levels so there is no real reason to shift policy either way yet. Still, if it comes, the key move will much more likely be the removal of local lending restrictions than interest rate cuts.

The third key signal is deficit spending and especially infrastructure. You’ll see lot’s of announcements from the National Development and Reform Commission (NDRC) and spikes in credit drivers, not in bank or shadow-bank lending, but the bond markets:

It’s pretty unmistakable!

Finally, broad credit will lift:

It appears to me that China has a pretty decent handle on its slowdown today and there is no need to rush into further stimulus. No doubt it will come but it usually follows a string of modest efforts that chase demand down before the big guns are pulled out.