Brokers at Commonwealth Bank subsidiary Aussie Home Loans overwhelmingly favoured its owner’s mortgage products but sold under a number of different brands according to data provided by the broker to the Hayne royal commission.

…in 2015 as much as 39.7 per cent of the mortgages the broker sold by volume and 37.5 per cent by value were manufactured by Commonwealth Bank, BankWest and Aussie Select.

The large proportion of CBA loans sold by Aussie brokers were also discussed in a “Reputational Impact Brief” where the bank’s public relations team discuss ways to deflect the claim after identifying the risk as high.

…Among the potential reasons for the skew in CBA loans the bank might offer the media included the higher level of service they might receive on Aussie products, a speedy 48-hour approval process and growth in white labelled products across the industry more generally.

The obvious solution is forced divestiture but, frankly, it’s not enough. The entire mortgage broking sector is rife with structural conflicts.

Advertisement

The real problem here is the diffused responsibility of having outsourced credit agents at all. That was obvious in the bizarre set-up of Aussie versus CBA:

Mortgage broker Aussie Home Loans does not have the capability to detect fraud committed by its brokers and instead waits until the banks detect scams and alert them as it does not have the resources.

The admissions were made by Aussie Home Loans general manager of people and culture Lynda Harris in a second day of questioning at the banking royal commission from counsel assisting Rowena Orr, QC.

…“We don’t have that, we are reliant on the lenders to provide that expertise because ultimately they are the organisation that is approving the loans,” Lynda Harris said.

Banning commissions does not fix this problem. Only banning brokers does. It is the same problem that was at the heart of the US sub-prime meltdown where shadow banks issued debts that they then sold onto investment banks and thence to investors via securitised vehicles.

Advertisement

If the credit officer and institution does not carry responsibility for the loan over its lifetime then lending standards will always fall.

What is most worrying about this the similarity between it and the 1890s bubble. The RBA described the 1880s Melbourne land bubble like this:

The potential for ‘bubblesʼto have a wider impact strengthened dramatically from the 1880s. The financial system was broadened by an expansion in the number of banks, their greater geographic reach through the establishment of branch networks and by the growth of non-bank financial institutions. The ratio of the assets of all financial institutions to GDP rose from 55 per cent in 1881 to 115 percent in 1891. The growth of credit shifted the demand schedule for all manner of assets to the right, not just Melbourneʼs land and property. Though still a small minority, many businesses that owned and traded in real estate, pastoral land and mining leases had listed on the emerging stock exchanges. A market in secondary claims encouraged more people to participate in the speculation. The market value of securities listed on the Stock Exchange of Melbourne rose from 18 per cent of national GDP in 1884 to 31 per cent in 1889.

The rapid growth in credit fuelled the Melbourne ‘bubbleʼ. The growth of the share market, comprised of more listed companies, and with higher daily turnover was another important contributory factor. Asset prices were marked to market on a daily basis and reported in the press. The gains of holding securities were there for all to see. Transaction costs of trading financial securities were, as John noted, lower than dealing in real property or other physical assets. The market looked relatively safe, risk could be diversified and you could cash out in a liquid market. Market-makers were important catalysts. Company promoters and share brokers assured investors and clients that this game of pass-the-parcel would never end.

The expanded financial and securities markets leveraged the ‘bubbleʼ going up and coming down. There was a new dimension to the end of a ‘bubbleʼ, a secondary Discussion 45 impact as the financial institutions struggled as the customersʼspeculations turned to losses and defaults. The route between the breaking of the land boom in 1889 and the banking collapses of 1893 is long and tortuous, but there is a strong causal link. The liquidations and reconstructions of many Australian banks depressed the real economy for many years. It should be remembered that many British speculators, investors and bank deposit holders shouldered losses as well as the locals.

Advertisement

Australia got very lucky in 2008 when its newly-minted shadow banking sector was destroyed in the GFC without bringing down the entire economy. That was achieved by wholesale public guarantees to both on-balance sheet banks and securitisation markets. These allowed the formal banks to absorb the non-banks without a “sudden stop” in credit.

I have often thought since that that was fortuitous for Australia, a bullet dodged. While other nations were sunk by much larger and more advanced non-bank sectors, we were lucky enough to have ponderous banks and slower deregulation that prevented too much off balance sheet lending lowering lending standards too far before the bust.

Yet the issue with non-banks was not so much the price of credit that they could produce, it was the abandon with which they could lend to lower-end customers. Sub-prime as it were. This was a technical issue in that securitised loans are more care than responsibility but it was also a corporate memory or industry standards issue. The new generation of non-bankers that got their hands on the tools of money creation did not have the wit nor experience to know when and to whom they should not lend.

Advertisement

The broker channel is a clear analogy to the inexperienced bankers of the 1890s. Moreover, the evidence that they have loaned with abandon is in more widely than the Royal Commission, from UBS:

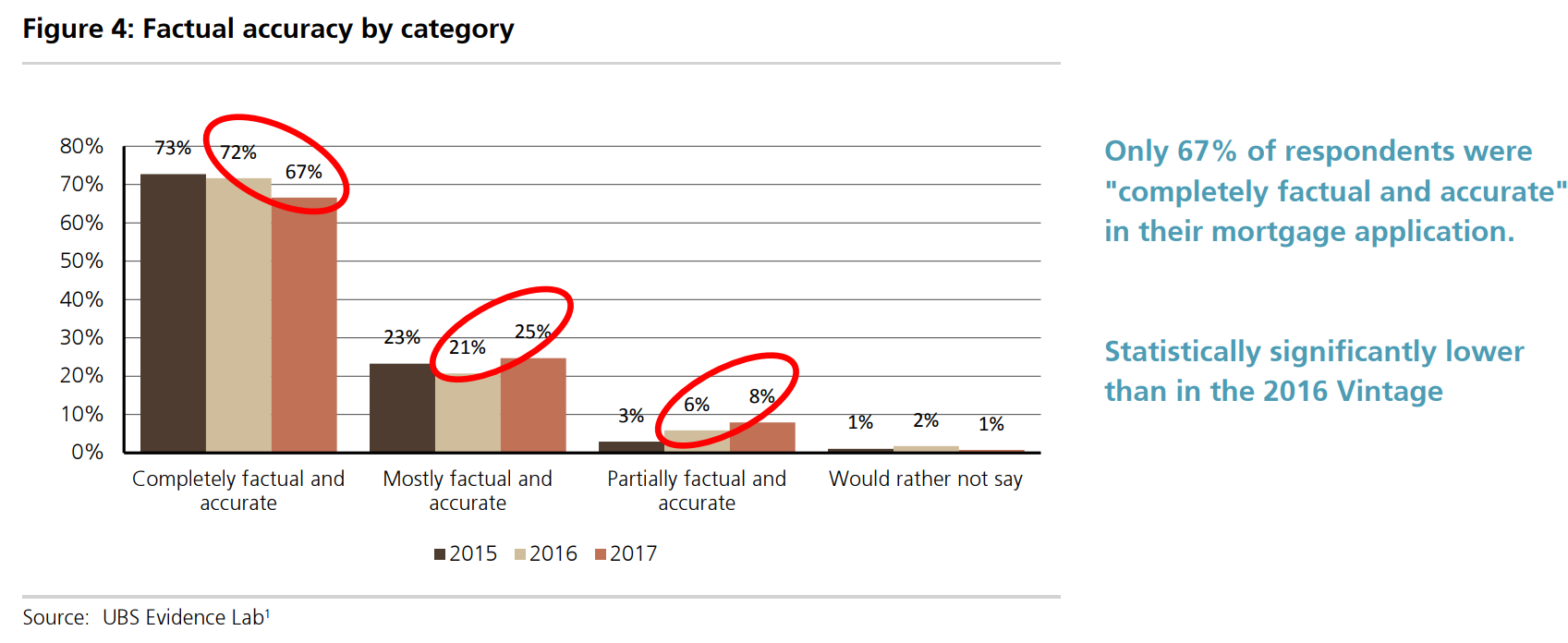

One of the key areas of focus of the 2017 UBS Evidence Lab Australian Mortgages survey was to assess the level of factual accuracy in mortgagor’s applications. While there has been anecdotal evidence for many years that customers are not always accurate in their application, we were lacking hard evidence. As a result the UBS Evidence Lab asked participants who had recently taken out a mortgage the degree of factual accuracy in their application.

The results of this survey were disappointing, with only 67% of participants stating their mortgage application was “completely factual and accurate”. This is a statistically significant fall from the results of the 2015 and 2016 Vintages.

This was offset by a statistically significant increase in respondents who stated their application was “mostly factual and accurate” (25% up from 21% in the 2016 Vintage) and “partially factual and accurate” which reached 8% of applications (up from 6% in the 2016 Vintage and 3% in the 2015 Vintage).

We see these results as disturbing and difficult to reject given approximately onethird of participants stated their application was not entirely factual and accurate.

Further, it is highly unlikely respondents would have stated that they misrepresented their mortgage application when in fact they were truthful. If anything, we believe it is more likely these figures may understate the level of misrepresentation in mortgage applications as some respondents may not want to state they were less than completely accurate despite the anonymity of this survey.

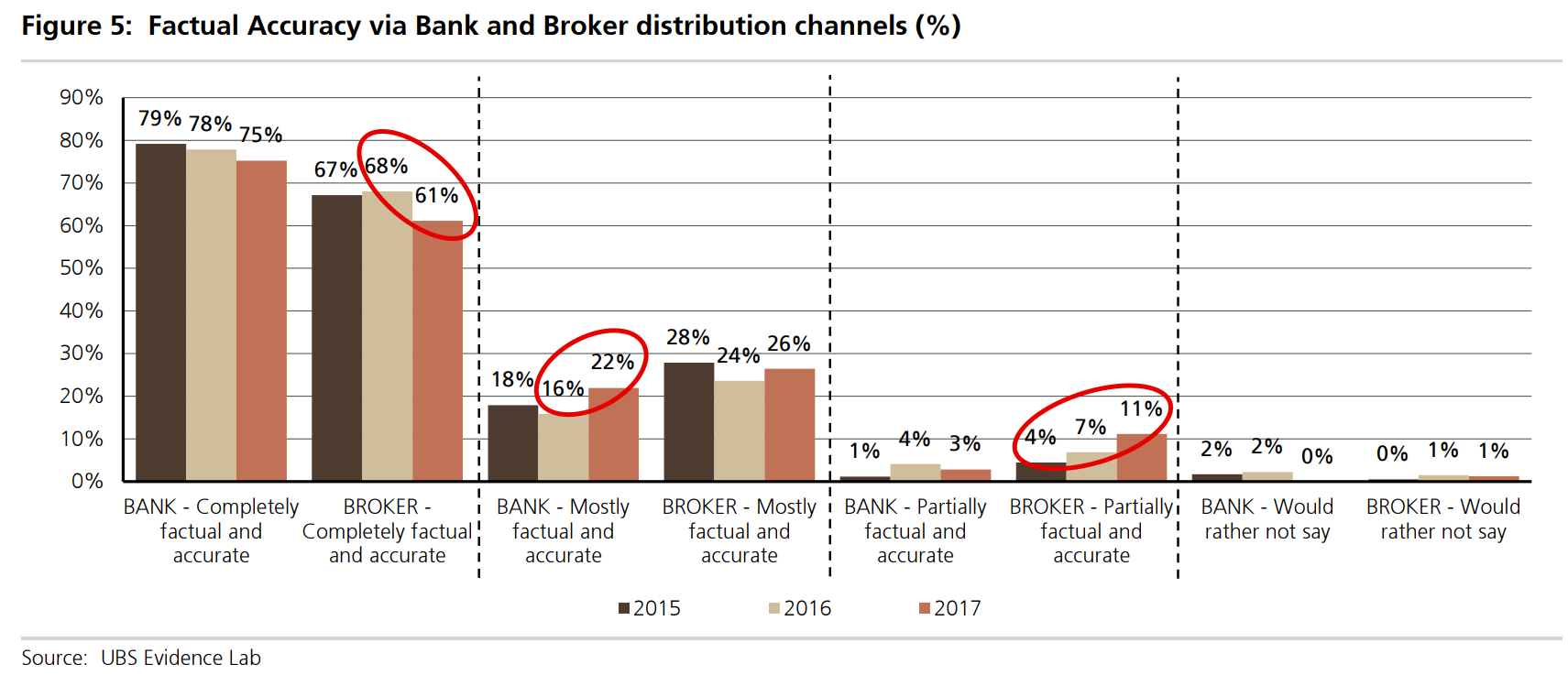

Misrepresentation more prevalent through the broker channel

During the 2017 Survey we found a statistically significantly higher level of factual inaccuracy via the broker channel than via the bank’s proprietary networks.

However, the level of factually inaccuracy has risen across both channels. In the 2017 Vintage only 61% of participants who undertook broker originated mortgages stated they were completely factual and accurate. This is down from 68% in 2016. This compares to 75% of customers stating they were factually accurate via the bank’s proprietary networks. Of concern 11% of participants who took out a mortgage via the broker channel in 2017 stated their application was only “partially factual and accurate”. This is a statistically significant increase from both the 2015 Vintage (4%) and 2016 Vintage (7%).

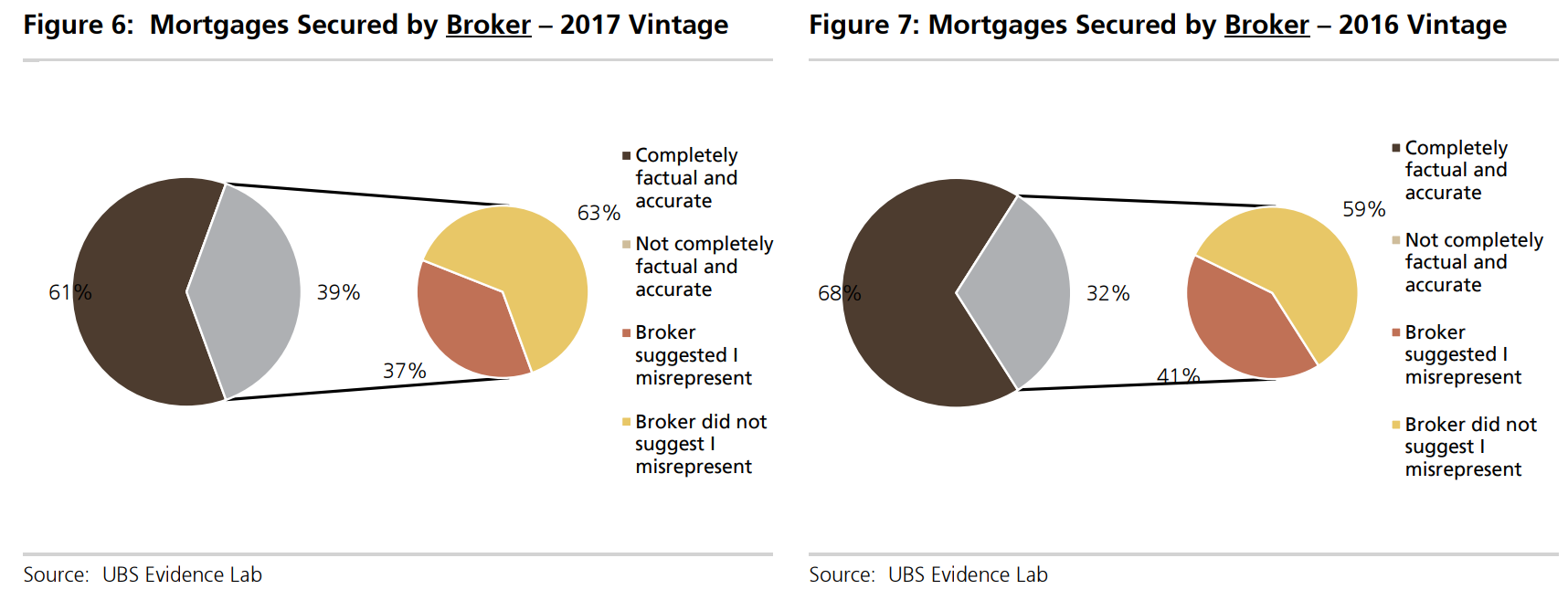

Was misrepresentation suggested by the broker or banker?

While the significant level of mortgage misrepresentation is a concern, we are more concerned that a substantial number of applicants continue to state that their mortgage consultant suggested they misrepresent their documentation.

During the 2017 Vintage 37% of respondents who used the broker channel and were not completely factual and accurate stated that their mortgage broker suggested they misrepresent the application. While this is down slightly from 41% in the 2016 Vintage it is still a concern.

This also implies that 14% of all mortgage applications via the broker channel were factually inaccurate following the suggestion of their broker, a similar level to 2016 (13%). It is possible that customers who have knowingly misrepresented their loans would prefer to point the blame at someone else, even in an anonymous survey.

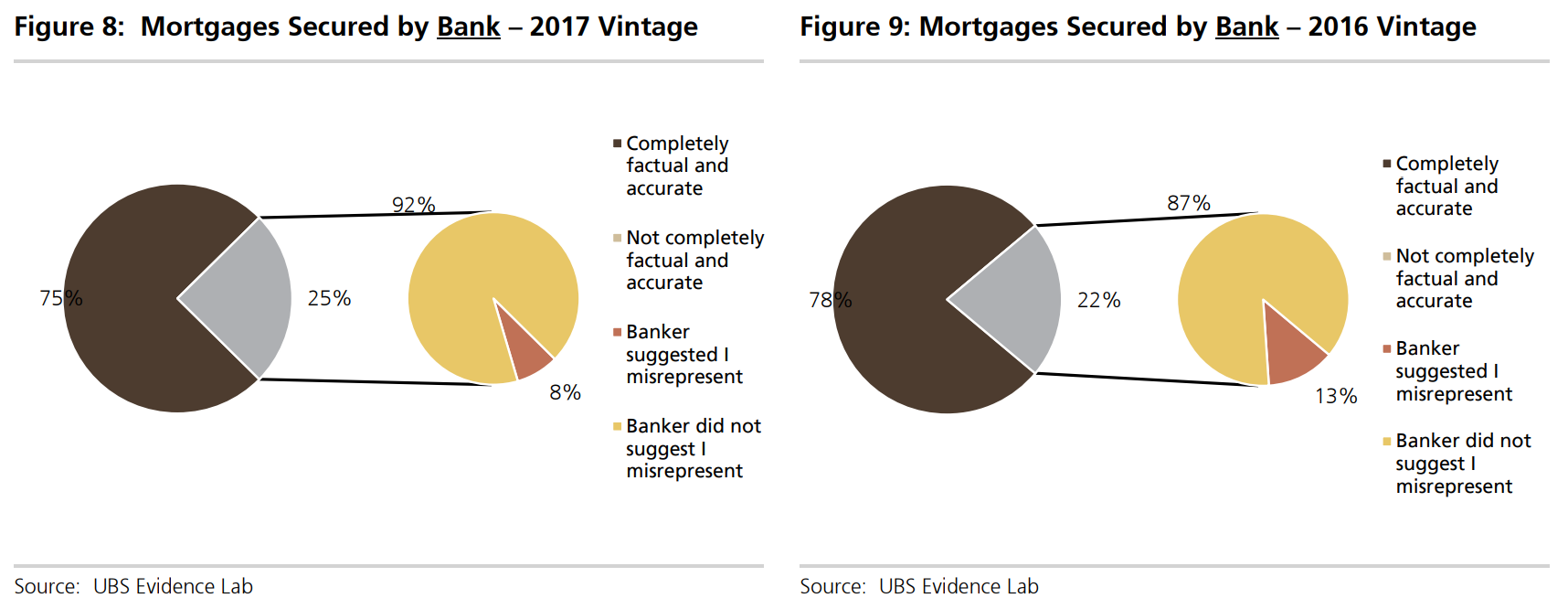

While there has also been a slight (not statistically significant) increase in the level of mortgage inaccuracy via the banks’ proprietary networks, the number of participants who stated that their banker suggest they misrepresent has fallen to 8% in 2017 from 13% in 2016. This implies only around 2% of bank originated mortgage applications are inaccurate as a result of the suggestion of the banker.

There is one difference to the 1890s but it is not a comforting one. The inexperienced non-banks of that period were funded from largely outside of the formal banking system. In this bubble the banks themselves created an “all care and no responsibility” broker channel for their own loans. If the time bomb does go off this time, it is sitting right at the centre of the banking system as the debauched Aussie/CBA relationship shows.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.