The rent-seekers at the HIA have released dodgy commissioned modelling from economic consultants – the Centre for International Economics (CIE) – warning of housing Armageddon if Labor’s policy to halve the capital gains tax (CGT) discount is implemented:

“According to research released today, an increase in Capital Gains Tax would result in a $1bn reduction in revenue to state Governments, increase the cost of renting and exacerbate the housing affordability challenge,” stated Tim Reardon, HIA’s Principal Economist.

HIA commissioned the Centre for International Economics (CIE) to investigate the economic implications of changes to the rate of Capital Gains Tax (CGT) on the economy. The Report models the impact on the economy of four different changes to CGT discount rate.

“The analysis shows that increasing CGT would generate a revenue gain for the Federal Government of $0.5bn a year which would be dwarfed by stamp duty tax losses to the states in excess of $1bn per year.

“The CIE also concludes that increasing the tax on investment homes may initially benefit ‘first home buyers’ but over time this gain will be lost as rental costs rise leading to higher home prices, that will once again force first home buyers out of the market,” added Mr Reardon.

“The RBA, Productivity Commission, Federal and State Treasurers have all identified the constraints on the supply of housing as an underlying cause of housing affordability challenge.

“Increasing the tax on housing will result in less investment in housing, fewer houses being built and inevitably a worsening of the affordability challenge.

“We cannot tax our way out of the housing affordability problem.

“Addressing affordability requires coordinated effort by all tiers of government to allow the industry to respond with the type and location of housing required to satisfy the pent-up demand.

“The report also finds that grandfathering existing investment properties out of the CGT changes will magnify these problems. Grandfathering reduces revenue from Stamp Duty to the States by reducing the number of homes built, and delays the inflow of additional CGT revenue to the Federal Government for decades,” Mr Reardon concluded.

Contrary to the HIA’s propaganda, unwinding the CGT discount makes sense for a variety of reasons.

First, there are actually significant Budget savings to be made. The Parliamentary Budget Office has estimated that cutting the CGT discount to 40% would provide a four-year Budget saving of $2.3 billion, whereas cutting the discount to 25% would save $5.7 billion over four years, and removing it altogether would save the Budget $10 billion. In a time of deep Budget deficits such savings are money for jam.

Sure, there would be some negative impact on state budgets, but given stamp duties are one of the most inefficient tax bases around, what better way to encourage reform and facilitate a shift towards land taxes than making stamp duties less attractive?

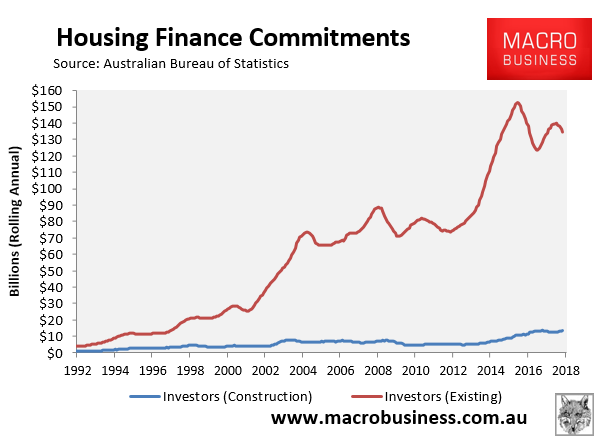

Second, Blind Freddy can see that investment in existing dwellings has literally exploded since negative gearing was reinstated in 1987, followed by the halving of CGT in 1999. By contrast, investment in new dwelling construction – which is the supply that the HIA bemoans is far too low – has been poor:

By all measures, negative gearing and the CGT discount have been epic failures in achieving the HIA’s goal of boosting new construction, despite their significant cost to the Budget.

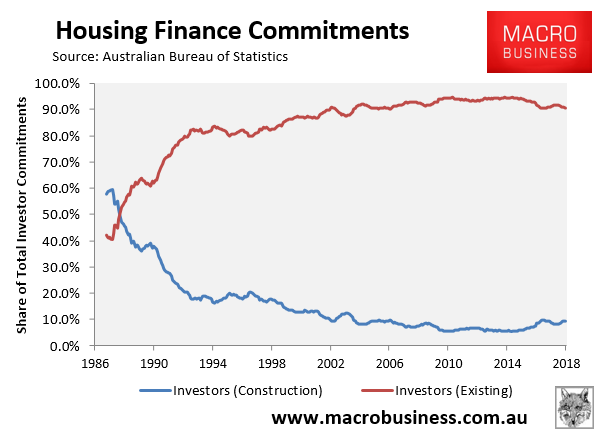

Third, there would be minimal (if any) impact on rents from lowering the CGT discount, since more than 90% of investors buy existing dwellings, and therefore do not add materially to supply:

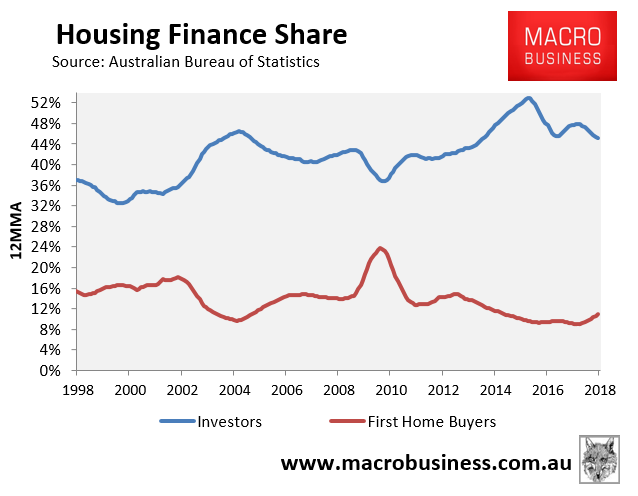

Finally, there is a clear inverse correlation between investor demand and first home buyer (FHB) demand:

Thus, any reduction in investor demand from cutting the CGT discount would unambiguously benefit FHBs, who would no longer be crowded-out.

In short, the HIA has resorted to propaganda rather than a considered analysis of the facts.

unconventionaleconomist@hotmail.com