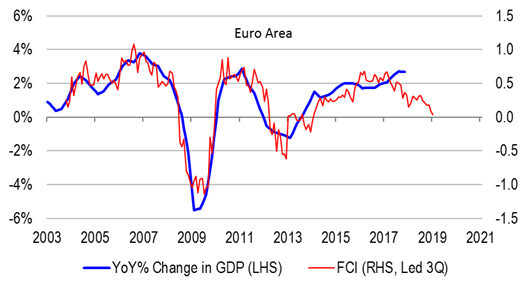

Recent European data have surprised materially to the downside. For example, German industrial production and retail sales likely shrunk by around 0.9-1% in 1Q, after growing very strongly in 2017. Also, sentiment indicators have fallen sharply off historically high levels.

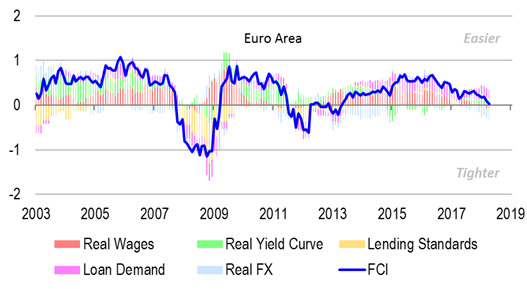

We are not surprised by these developments. Indeed, we expect to see more negative data surprises to come. Our proprietary European financial conditions index has historically been a reliable leading indicator of activity growth. It has been deteriorating steadily over the past few quarters to levels consistent with stagnation in the economy.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.