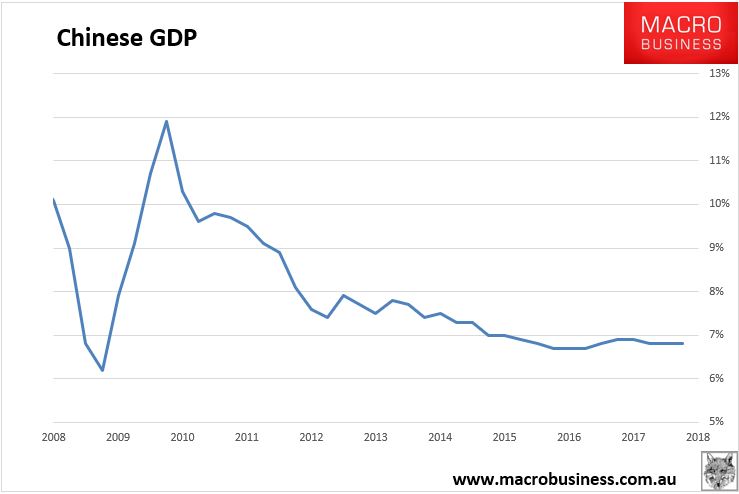

China has released March QTR GDP which came in as expected at 6.8%:

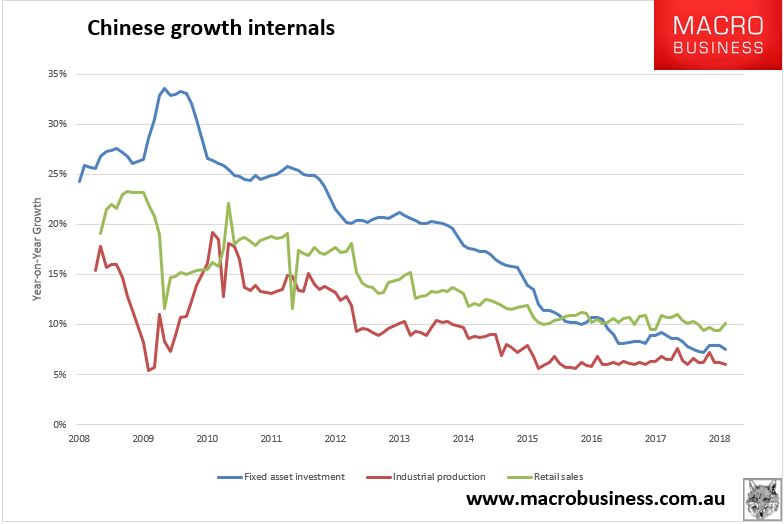

Underneath that was a real mixed bag. Industrial production missed at 6% and fixed asset investment missed at 7.5%. Retail sales beat at 10.1%:

Advertisement

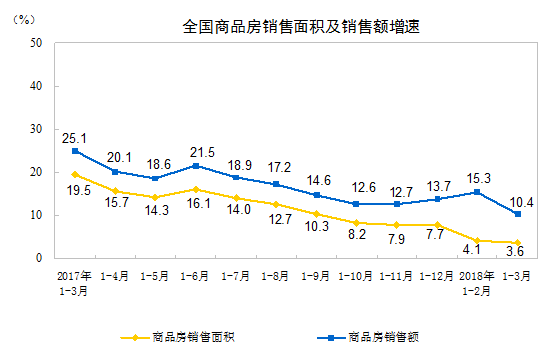

Turning to real estate, sales continue to slow with YTD down to just 3.6%

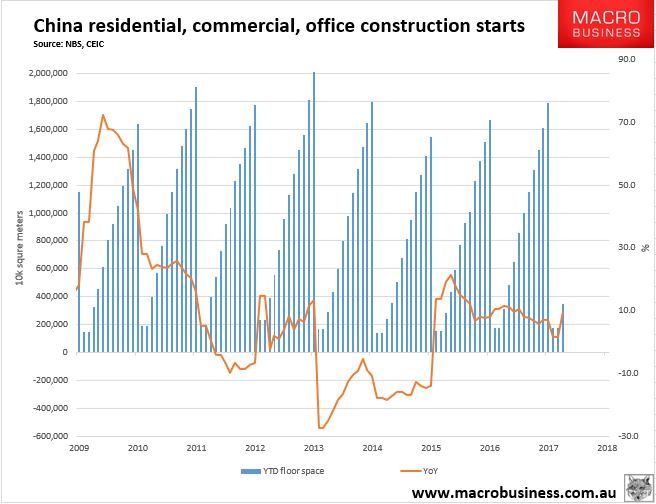

Starts rebounded strongly to 9.7% YTD but I suspect that is in part a post Winter shutdown rebound:

Advertisement

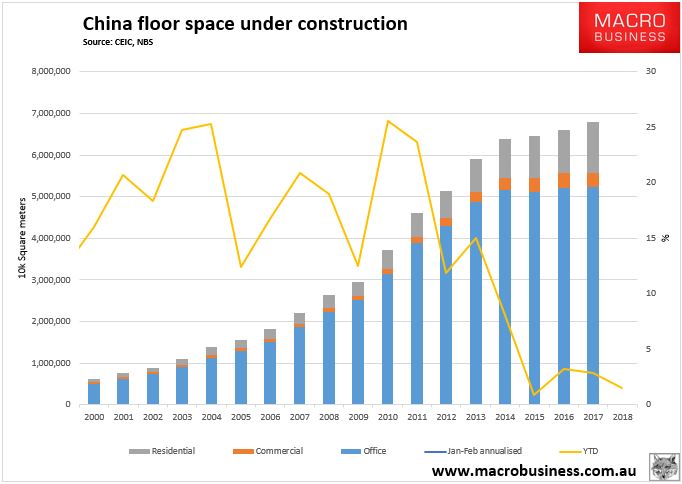

Floor area under construction fell to 1.5% YTD growth:

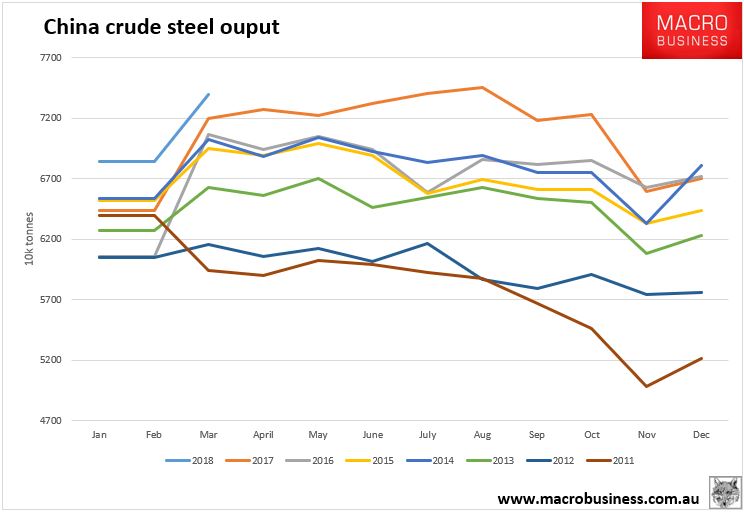

Crude steel boomed after Winter shutdowns but the YoY gap is narrowing fast. It should close by Q3:

Advertisement

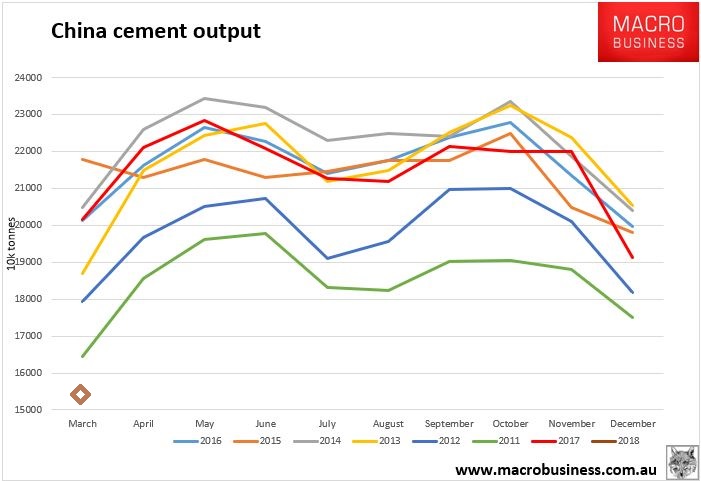

Cement output cratered for no obvious reason:

Quite the mixed bag which has led to a steep drop in the Credit Suisse Nowcast model:

Advertisement

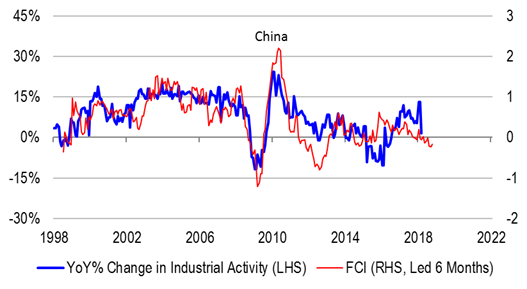

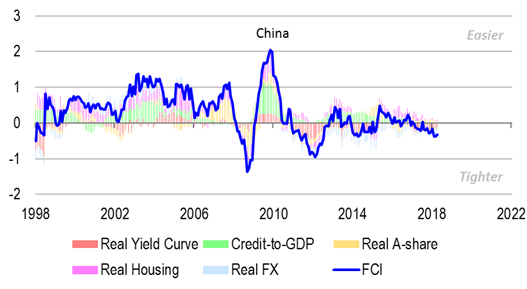

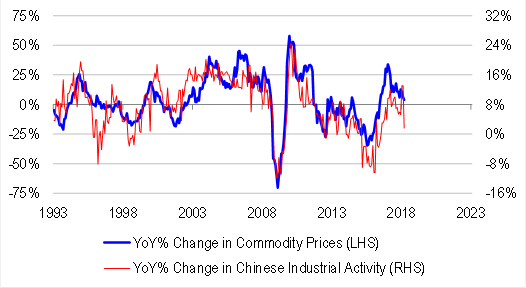

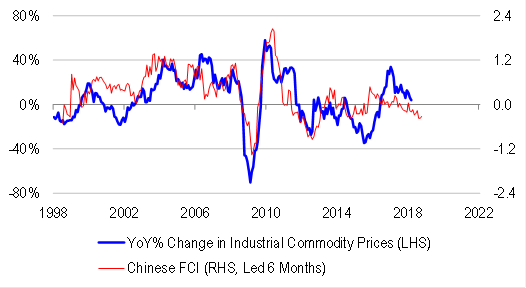

Our proprietary measure of industrial activity looks across hard data points. It has plummeted to 1.6% from 13.1% in January/February. The sharp slowing is broadly consistent with what our financial conditions index has been suggesting. Financial conditions in China remain very tight because of liquidity problems caused by hot money outflows in a pegged exchange rate regime.

It’s not obvious to the untrained eye so markets have rallied. But the leading edge of the slowdown has arrived.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.